So much for fiscal probity!

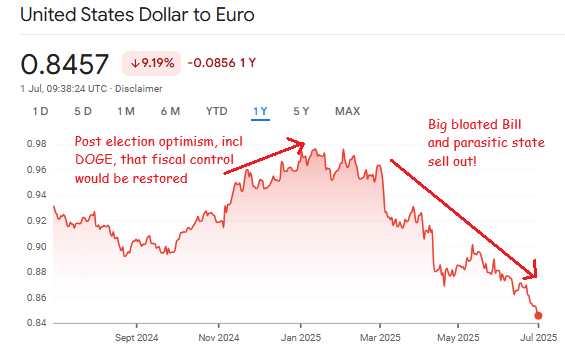

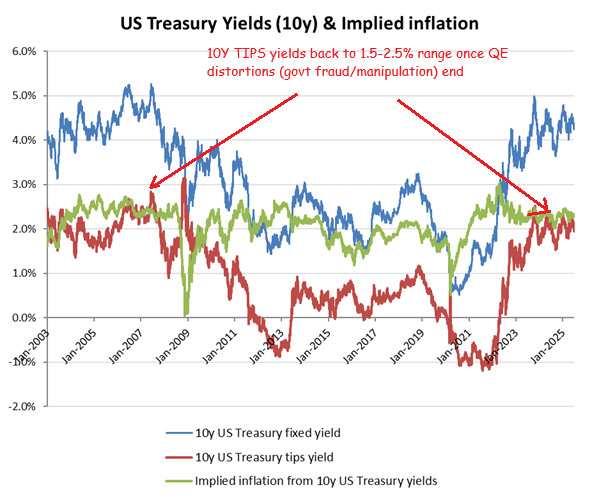

For currency markets and bond vigilantes, Trump is proving to be a great disappointment, particularly against the initial high hopes of a return to honest financing following the election rhetoric and the early progress on DOGE by Elon Musk. The initial rally in the USD has now reversed as Trump’s bloated “One Big Beautiful Bill Act” threatens to exacerbate an already unsustainable level of deficits. Notwithstanding his attempts to deflect blame on Fed Chair Powell, running a deficit of over 6% of GDP for the foreseeable future, when public debt is already over 120% of GDP (>$36tn) is the real reason TIPS yields are back over 2%. Yes, a new Fed Chair could return to QE to monetise the deficit and create to illusion of solvency, albeit this would merely aggravate the negative pressure on the USD, where the real funding costs would threaten a much more expensive interest rate penalty. Short term and stupid, as we’ve all been able to see with Turkish bond yields and TRY depreciation.

Trump and his loyalists are currently busy gaslighting us that Fed Chair Powell is the villain in this story by not cutting interest rates. This is a rather sad red herring however, as short term Fed rates are irrelevant to longer term Treasury yields that investors may be prepared to lend cash to the US Treasury. They are also only one component on the real return to be had on these instruments, with confidence in the currency being considerably more important. When markets still believed in the election hype that fiscal restraint would be exercisied to balance the budget and restore honest financing, the USD appreciated. The subsequent volte face on this, including an outraged Elon Musk withdrawing support however, suggests otherwise and is clearly reflected by currency markets and the USD. If Trump wants to cap his funding rates, his first task will be to restore confidence to pursuade investors that the US government (and USD) is a safe haven for investment. Sure, they can sieze control of the Fed and drop rates, but unless they resort to QE again, that could be counterproductive on raising the necessary liquidity while the deficit and public debt levels remain out of control.

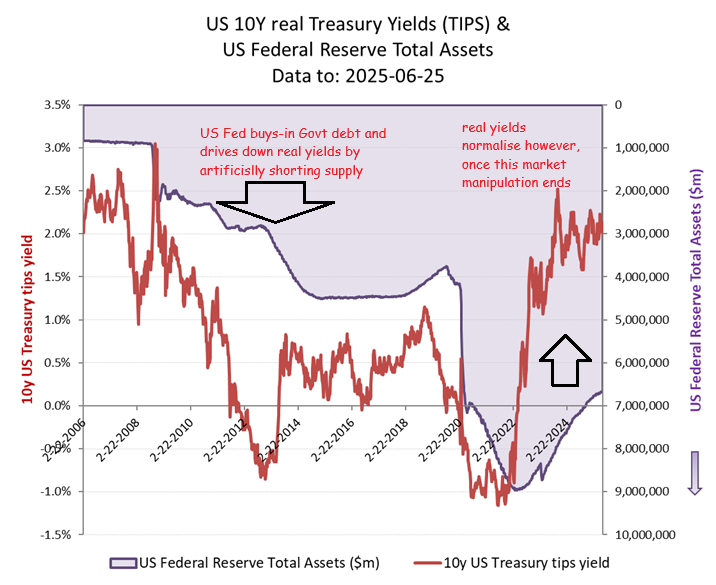

Without the debt monetisiation fraud of QE, real Treasury rates have normalised back to their longer term range of 1.5-2.5%. With debt maturities, an additional >$2tn of new debt to sell and a fiscal policy with limited credibility, there seems little reason why competition for funds won’t see these real yields err twoards the upper end of this range. Sure, the Fed could resort to market manipulation with QE to windrow dress this, but the impact on USD currency devaluation could prove considerably more costly.

It’s not rocket science. The government can manipulate initial rates in its bonds, but this is merely debt monetisation, which soon turns into debasement when markets realise that these will never get sold back into the market. Short term this might creat the illusion of lower funding costs, but once investors start factoring in the consequential currency debasement, this camouflage gets stripped away pretty quickly. An easing trade deficit on tariff uncertainties may ease that part of the FX equation, but the scale of the federal debt overhang and persistent budget deficit remains a serious risk of precipitating a negative spiral of deflating currency and compensatory inflating interest rates.

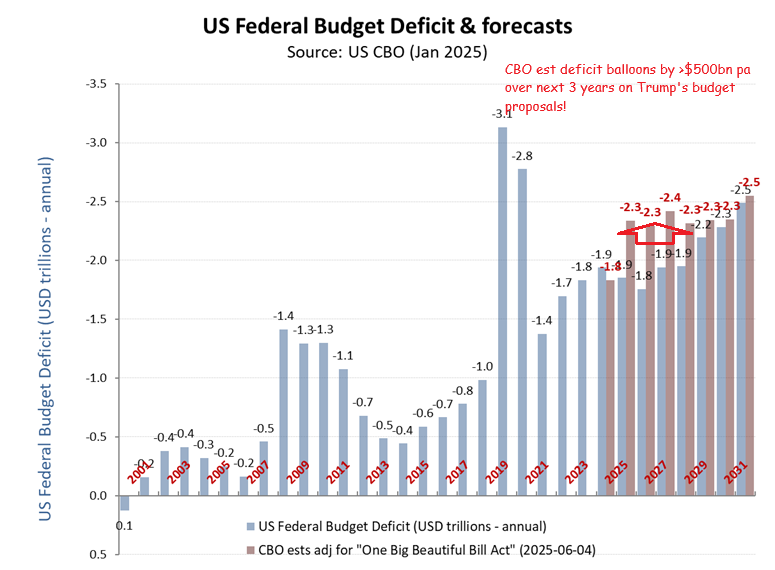

Running deficits of approx 6-7% of GDP as far as the eye can see while trying to support an existing debt overhang of approaching $37tn (or >120% of GDP) while debt markets normalise funding rates and realise governments are politically incapable of living withing their means. If there is one possible redeeming factor is that there is no obvious alternative reserve currency out there to hasten the collapse in the USD.