Another ‘conspiracy theory’ bites the dust?

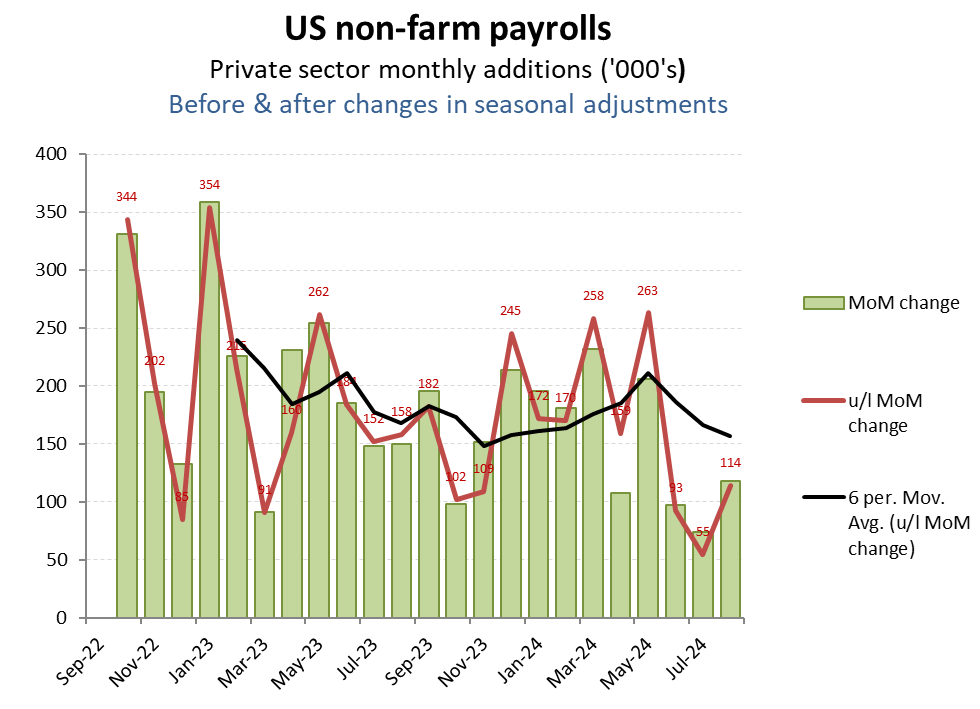

After lies, damn lies and statistics, government ‘estimates’ such as the BIS’s monthly guesstimates for non-farm payrolls must rank as one of the more unreliable economic datasets, particularly in the run up to a quadrennial election year in the US. While also undermined by the debt fueled life support currently being administered by the incumbent regime, these numbers do have a relevance in the type of message being communicated, and for now that is one of low but fairly steady growth, which in turn undermines some of the clarion calls for a return to monetary expansion (and debt monetisation) to support another artificial drop in interest rates.

While bouncing around the ~+100k per month level over the past quarter, private sector job formation remains above the approx -100/-200k pm levels that historically (and reliably so) have signaled an emerging economic recession. Unlike in Europe, limited employee rights protection in the US has enabled employers to react rapidly to signs of impending downturns in demand (such as order books) by cutting staff overhead well before the downturn hits their reported results or communications to investors.

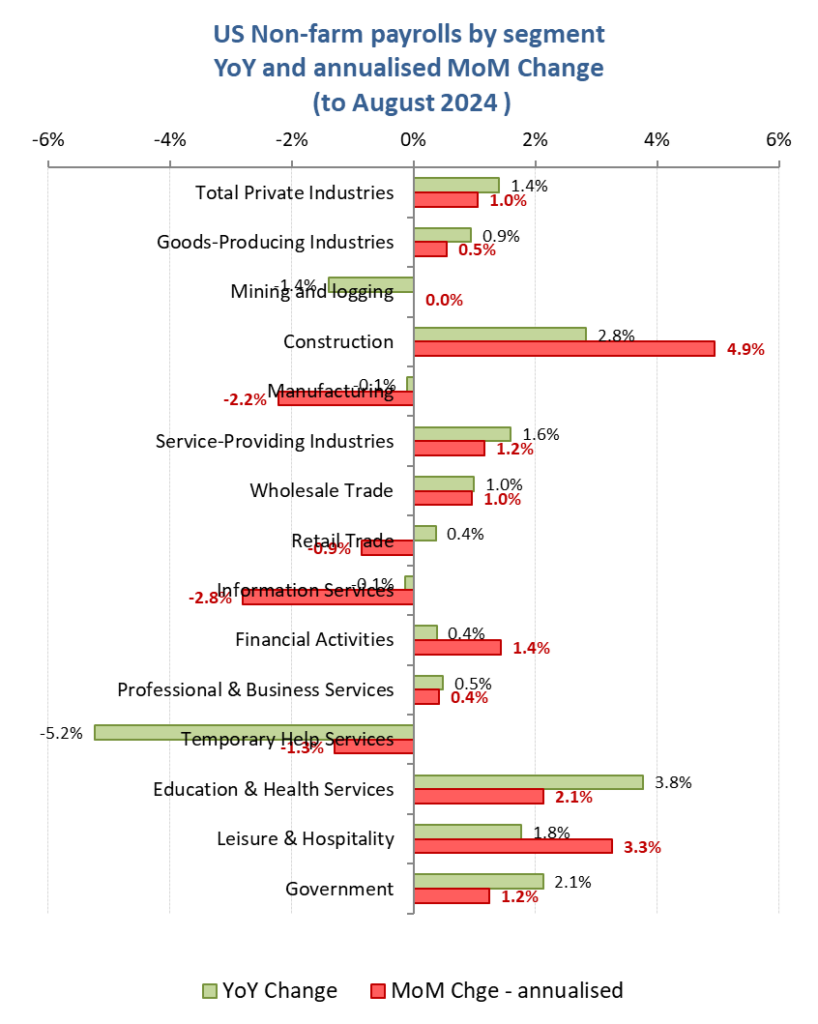

By industry sector and category, the August employment data remains mixed. The pick up in construction presumably is a reaction to easing mortgage rates and hopes for further easing to come after last year’s rate increases, albeit this could also mean some potential vulnerability to come should these rate cut expectations get disappointed. The softness in manufacturing however, remains a concern and possibly reflects the ongoing squeeze on auto sales and profitability following tightening ‘climate’ regulations, but resistant consumer uptake of EV’s together with a need for cost savings after last year’s inflation busting wage settlements. As such, there may be no early improvement from this category, which might remain depressed into the run up to the November elections. Elsewhere, ongoing softness in PC markets and a noticeable hangover in AI interest continue to depress Information Services while further easing in temporary help positions will need watching as this category can often act as an early indicator for swing demand for labour -ie areas that respond early until employers are confident enough of the trends to hire or fire permanent staff.

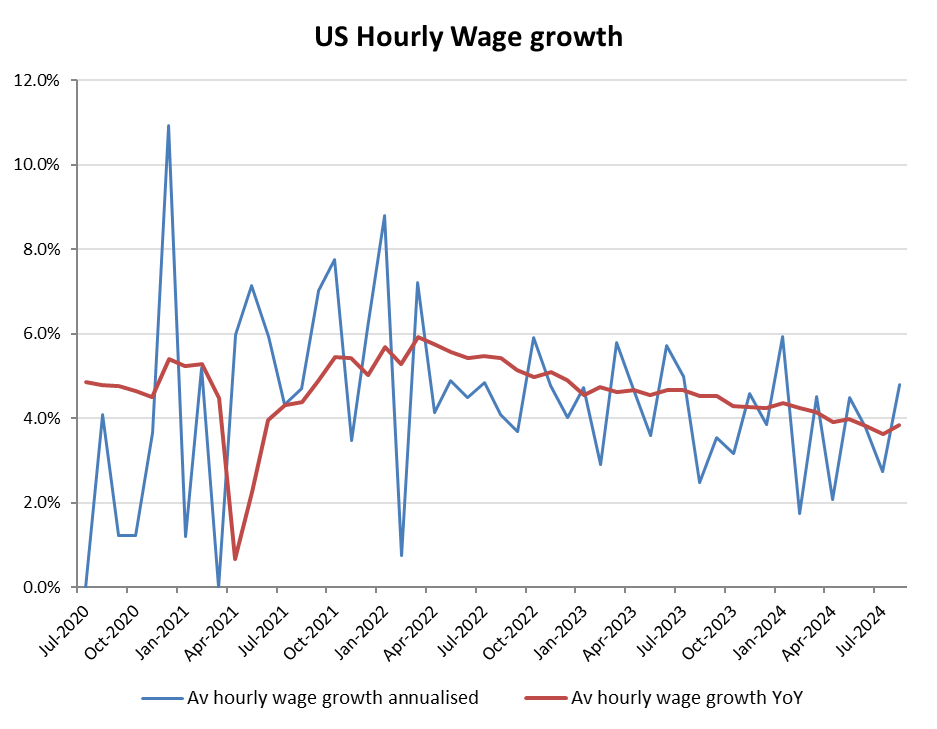

As with the overall net job formation, the data on average hourly wages is fairly inconsequential to the monetary tightening/easing debate. If net job adds is not flagging an imminent recession, the continued advance in average estimated hourly wage growth at a rate slightly ahead of inflation doesn’t suggest either an overheating labour market nor a need for an easing stimulus.

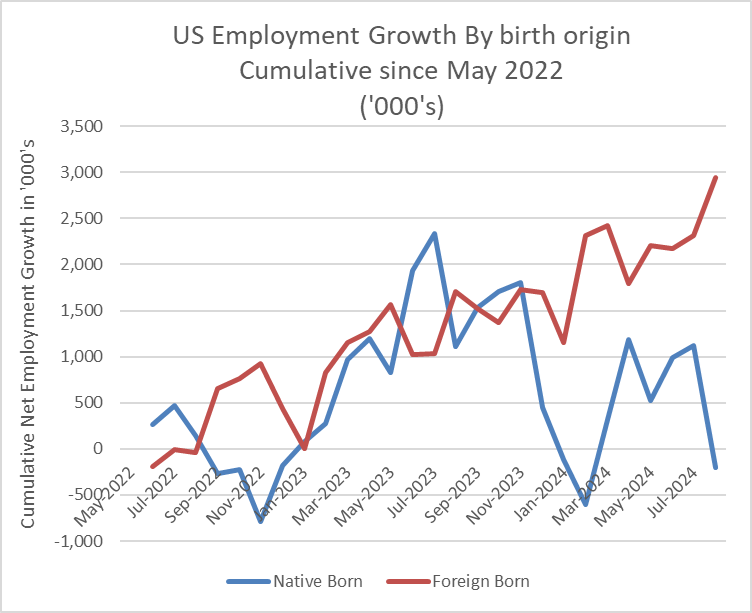

As mentioned already, markets and official data series are being manipulated by political interference, both in record deficit spending, where the full funding costs of the addition debt (approx $1tn per 100 days) has yet to be priced into either inflation (and USD debasement) and or/ bond yields as the US Treasury is forced to compete for borrowings. An additional distortion meanwhile includes the open borders policy, albeit any stimulus for ‘cheap’ illegal labour will have been more than negated by the additional social costs (financial and cultural) that will have to be paid on these. One such cost can be seen from the disparity of benefits from this strategy as domestic born workers are replaced by foreign born ones. As can be seen from the above BIS data, over the past two years, while there has been approx 3m net new jobs for foreign born employees, there has been no overall job growth for native born ones. Looks like another conspiracy theory (the ‘great replacement’) supported by the data!