Played again?

Are we being played, yet again? Markets have been suggesting as much since the start of the year, with gold soaring, the USD wilting and US treasury yields edging higher. The penny seems to have dropped even for Elon Musk as Congress tries to push its pork filled funding bill while failing to incorporate any of the DOGE savings into legislation. The FBI and DoJ meanwhile seem to have ‘lost’ all those Epstien videos and the tsunami of fraud implicating a substantial potion of the DC ‘swamp’ has yet to elicit any worthwhile indictments. With the FDA also approving a new mRNA covid shot before any proper placebo-controlled trial, the US electorate who thought they were voting for a change last November may be starting to appreciate how UK electorates have been feeling since 2016.

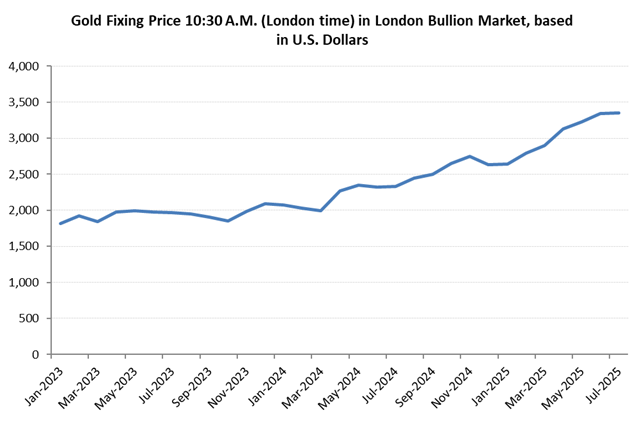

Gold soars

First it was the Biden/Yellen rush to insolvency driving cash into inflation/USD debasement hedges such as gold, but then only to see this accelerate with the new Trump administration. Wasn’t this supposed to be the fiscally responsible Rebublican party, which also controlled both houses of Congress. Surely, with Milei held up as the example and Elon exposing trillions in wasted expenditure with DOGE, while deregulation and reversal of net zero stimulates the economy the risk premium on the USD ought to have been contained, particularly as core inflation retuned to below +3%. Factors, positive to the USD one light have hoped.

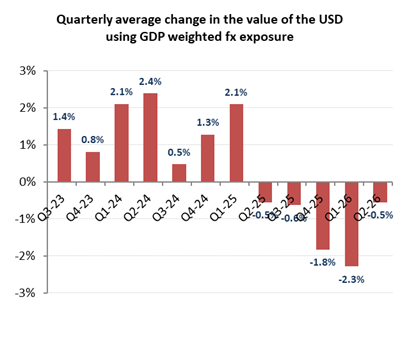

While USD wilts

Not to be however. Perhaps it was the tariff club being used in the trade negotiations, or the punishment meted out by those challenged by the prospective ending of the ‘forever wars’, the climate alarmism and also the plandemics, all highly profitable earners for this group! Or perhaps it is more simple and part of a planned devaluation to assist the reduction in the trade deficits.

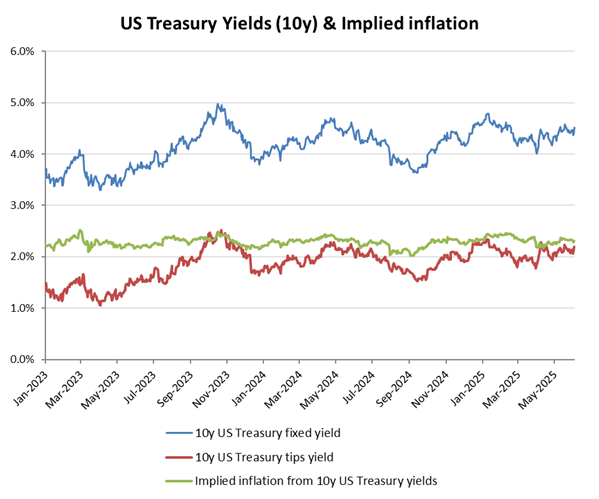

US treasury yields edging higher

As can be seen below, the Fed tightening is being tapered in face of the further maturity cliffs and refinancings, albeit not enough in itself to deflect the broader normalisation in funding rates, which are returning to the upper end of their long term range of approx 1.5-2.5% real (TIPS). Fold in an inflation element of around 2.5% pa and it ought to have been no surprise for fixed bond yields to head back up towards 5%.

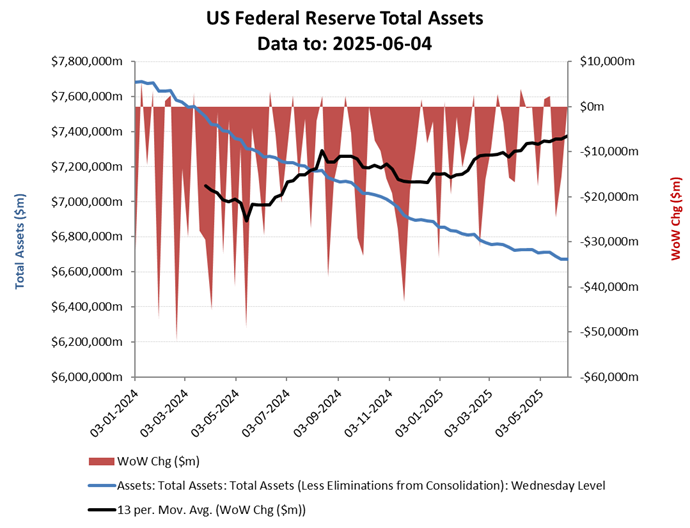

US Fed tapering the balance sheet tightening

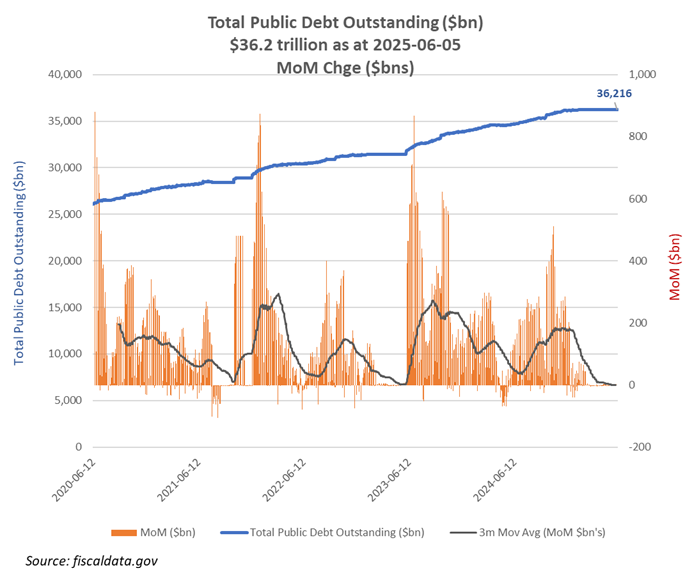

US public debt stable, albeit due to seasonal tax receipts

The recent stabilisation in US public debt may seem to take some of the recent pressure off the administration, but this is merely a temporay feature reflecting the normal tax inflows

at this time of the year. Trump’s ‘Big Beautiful Bill’ will see this back up towards $38tn by the year end and while attempts to remove the debt ceiling may ease the immediate funding issues, it will do little to inspire confidence with either the currency and/or bond markets. Elon’s reaction to what is a betrayal of the promise to restore fiscal responsibility therefore is more than just a clash of ego’s but something much more existential to the US.

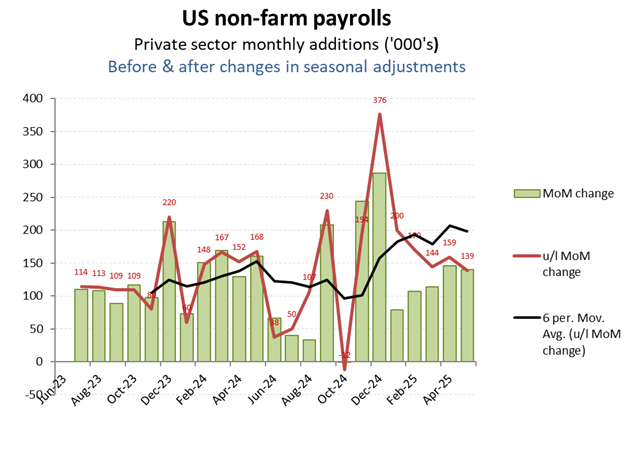

US private sector employment however, remaining resilient

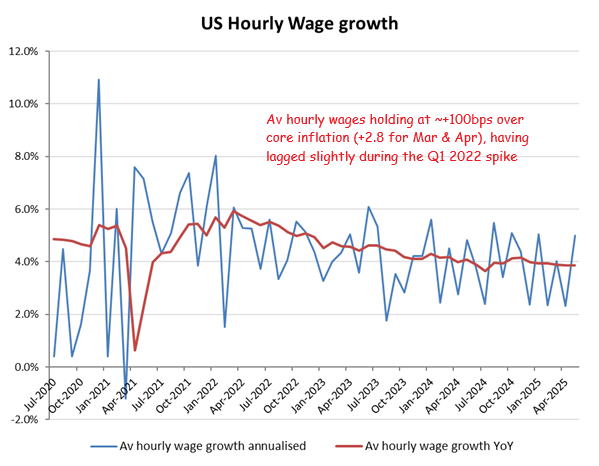

Short term, the employment guessimates out of the BIS are not flagging an imminent recession, with QoQ net job additions holding at almost +140k in May, while average hourly wages are now above a shrinking inflation outrun

Av hourly wage growth again above CPI

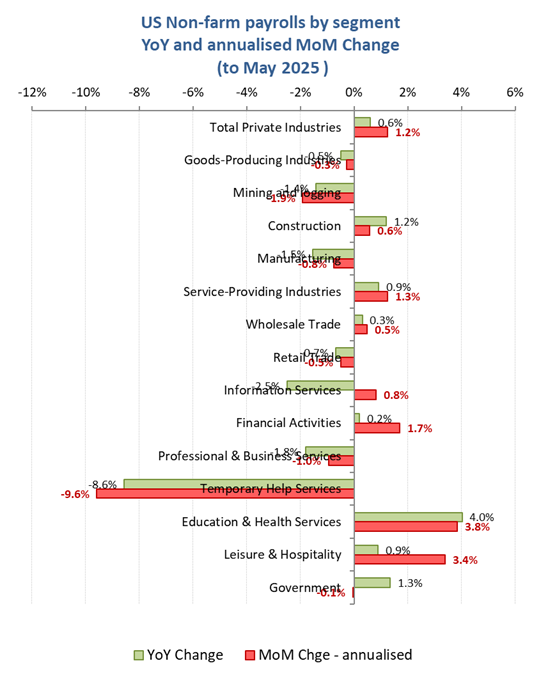

By category – sharp declines in temporary staff

By category however, things get a little more confusing. Notwithstanding the tariff strategy aimed at re-onshoring manufacturing, US manufacturing job numbers actually declined in May. Mining & Logging categories, which includes oil/gas production surprising was also weaker, notwithstanding the focus on domestic production in all of these. The sharp contraction in temporary employment can sometime reflect a tightening labour market which encourages a shift to contractual employment, although it can also signify the reverse, with this group easiest and cheapest to divest as a swing cost item should a softening economy be seen to be coming down the commercial pipe.

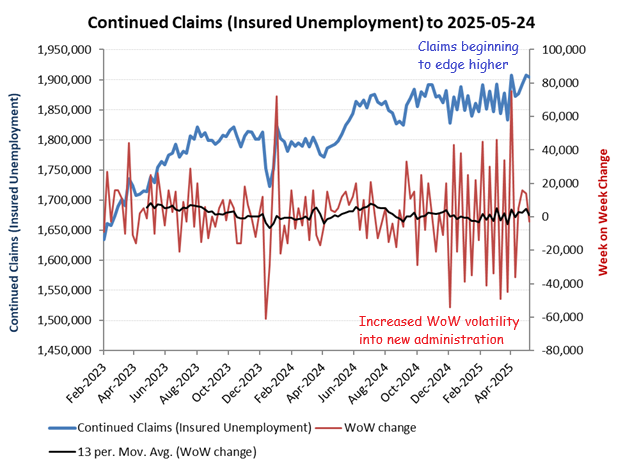

Insured unemployment claims edging higher

Initial concerns on future demand, particularly as recent tariff increases start to filter thru the system might also be refkected in the recent step up in unemployment insurance claims.

On balance, while the current state of the economy may seem relatively stable, there are clear emerging headwinds which may need a series of positive outcomes from trade to conflict negotiations to emerge otherwise we might be facing further bond yield hiatus along with stalling earnings expectations