Is the ECB being hung out to dry?

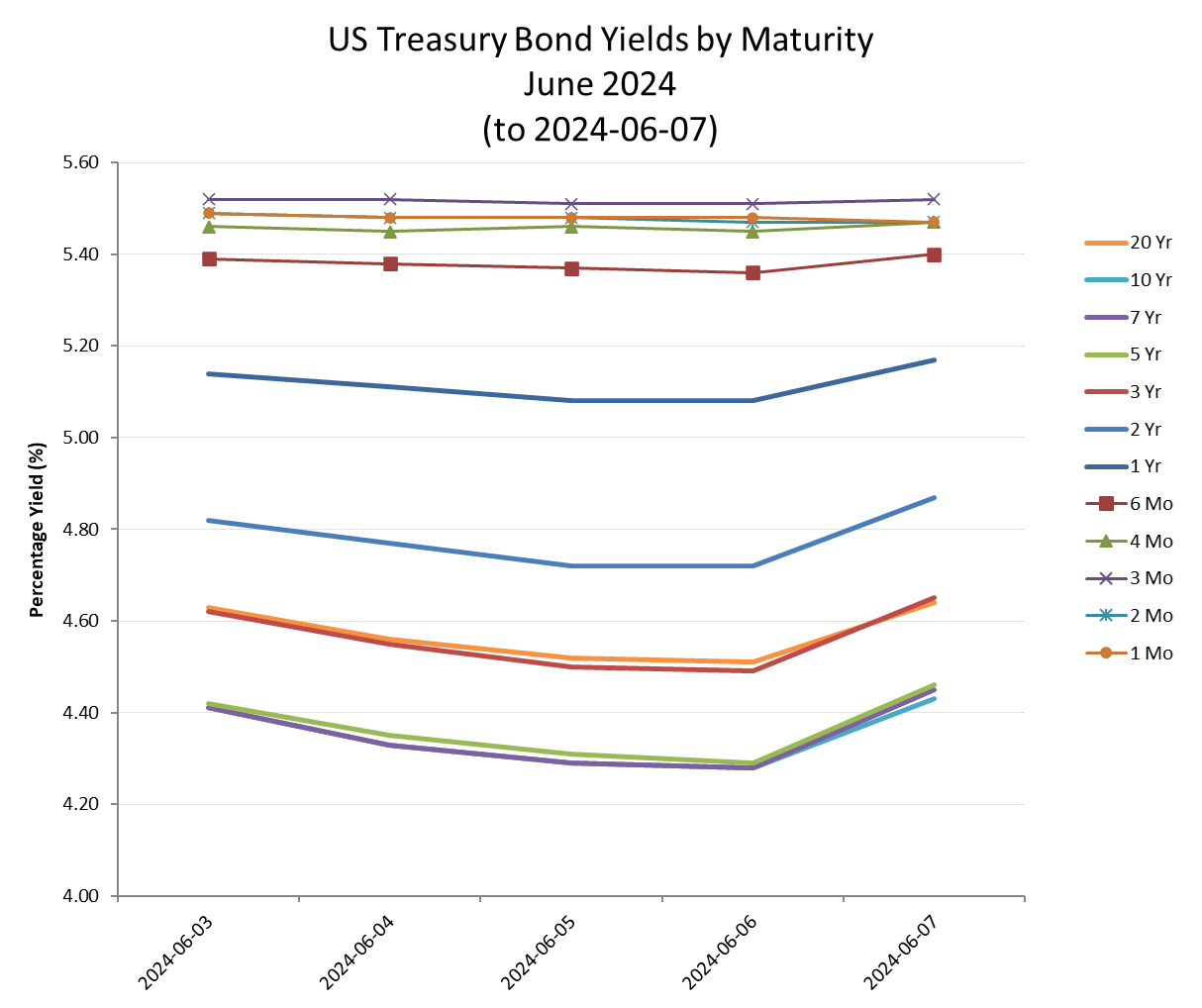

Has the US BIS not got the memo to support the easing narrative with softening economic data, or is the ECB and Euro being hung out to dry? For those hoodwinked by the manipulated GDP deflator assumptions (see below) between Q4 2023 and Q1 this year, into over-estimating the slowdown in economic activity must have been shocked by the hotter than expected May employment data released Friday by the BIS. But when your government has been running up a $1tn per quarter in deficit spending in an attempt to goose reported growth ahead of an election cycle, that growth is going to come with some adverse consequences for inflation and therefore interest rates. Much as Canada and the ECB both tried to pre-empt the start of an easing cycle with some largely symbolic rate cuts last week, as long as the underlying problems of spiraling deficits remain unresolved, funding costs will continue to rise. The subsequent rally in US treasury bond yields following these May employment numbers meanwhile remains the only verdict worth heeding and one which threatens to crush those hoping to ride on a wave of easing rates from the US.

The only trajectory that matters – are funding costs rising or falling?

Tax payers are maxed out, but governments persist in pursuing growth killing policies (climate, ESG, DEI, medical, CBDC, Ukraine .. you name it!) while addicted to spending programs, which means either monetising the deficits and risk spiraling into a currency and inflation crisis, or to borrow. The latter requirement however, means competing for funds in international markets at a time when most other leading economies are trying to do likewise. Much as these characters would like to talk down funding rates, squaring this circle isn’t a viable proposition until the spending side of the equation is resolved, which for now seems no closer. Bond markets seem to have the measure of this as can be seen from the firming trajectory in yields and which ultimately force reality on feckless governments and voters.

Lies & Govt statistics

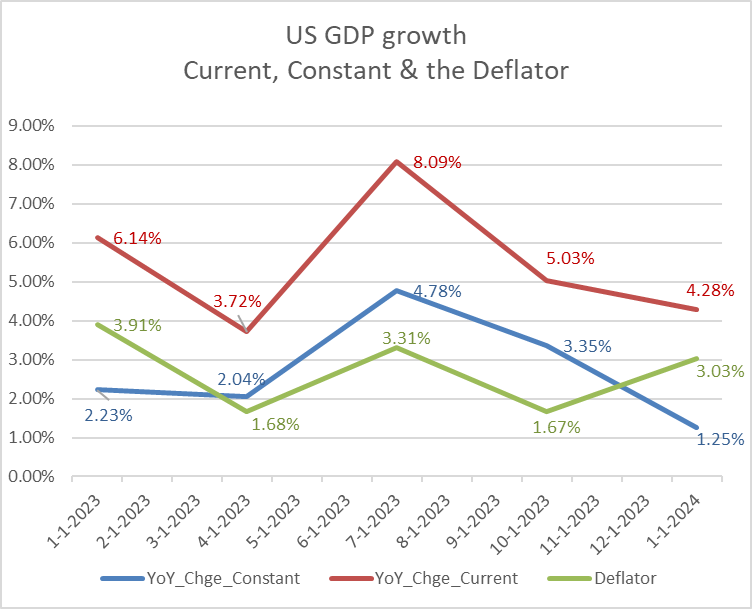

If markets thought the Q1 US GDP estimates were signalling an imminent collapse in economic growth that might justify taking the foot off the monetary brakes, then it was mistaken on two fronts. Firstly, the estimated decline in constant GDP growth from Q4’s +3.35% to only +1.25% for Q1 (-2.1ppts QoQ), reflected more the gyrations in the deflator estimate as what was actually transpiring in the economy. For instance, does anyone really believe the Q4 deflator (inflation) dropped to only +1.67%? In terms of actual (current price) GDP, the estimated Q1 slowed by only -70bps QoQ, while the reported real decline was exacerbated by the return of the deflator to a more reasonable level. The second reason meanwhile is the one already stated, that funding costs reflect the the relative demand for the asset required, in this case investors cash. More demand (from reckless deficits) on constricted supply, will determine the market cost of cash, rather than the wishes of the indebted.

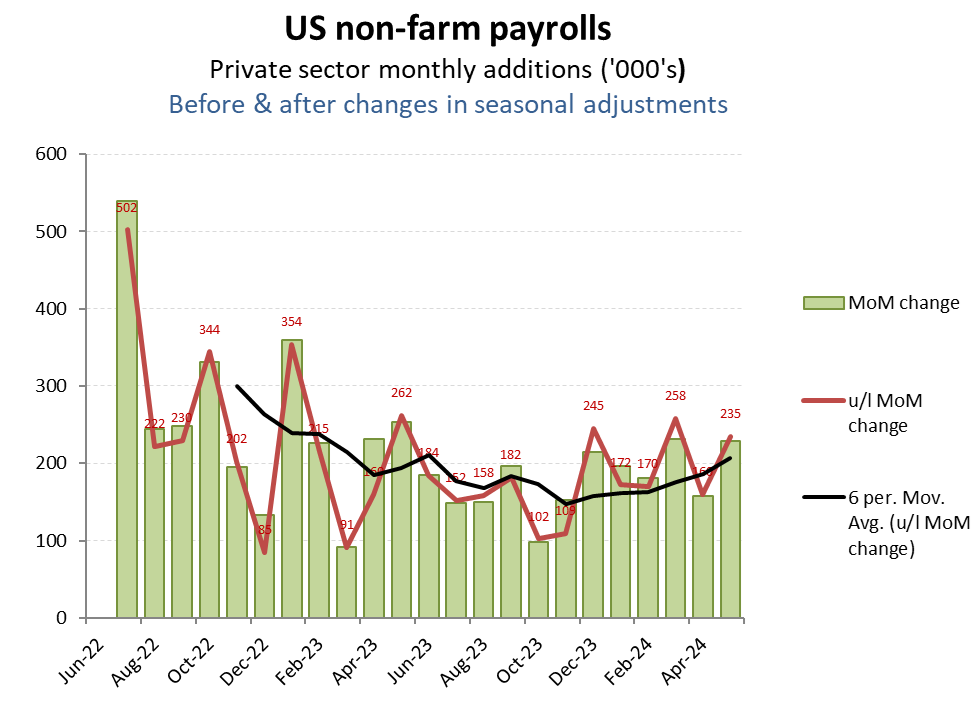

May employment data hotter than expected, or at least needed to support the easing narrative

Employment in May running hotter than expected, or at least than the easing narrative needed!

Whether it was the overall level of private sector job formation, or the underlying level (excluding changes in seasonal adjustments) or even the trailing 6 month average trajectory in these, it was difficult to extract a particularly negative spin on these figures.

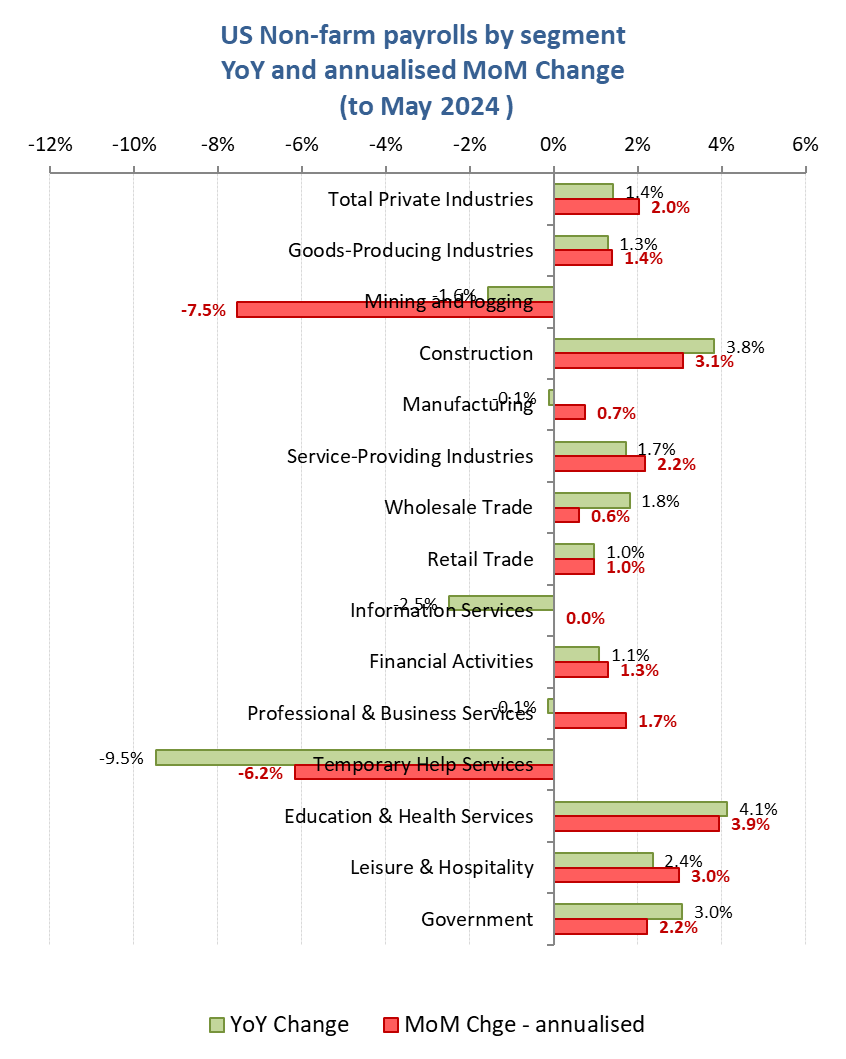

Apart from Temporary and Mining, a broad spread of employment growth

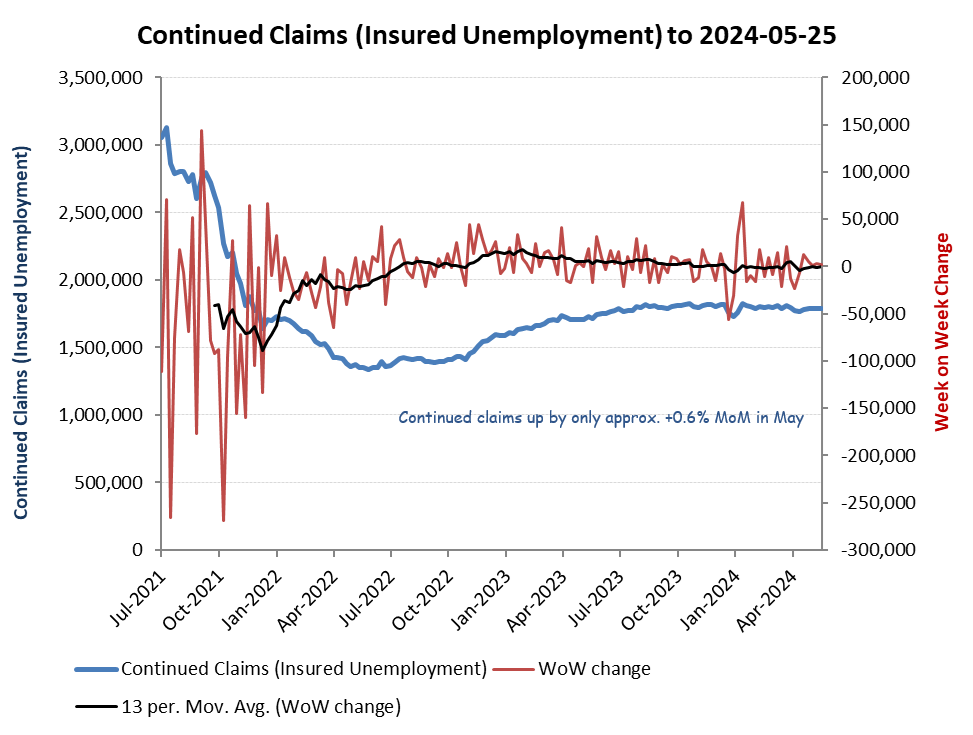

Sometimes, the insured unemployment claims data can provide some harder data series on the health of job markets, but for May, these were broadly flat, increasing by only around +0.6% MoM, which doesn’t offer much validation or otherwise to the BIS employment estimates.

Few signals coming from unemployment claim data

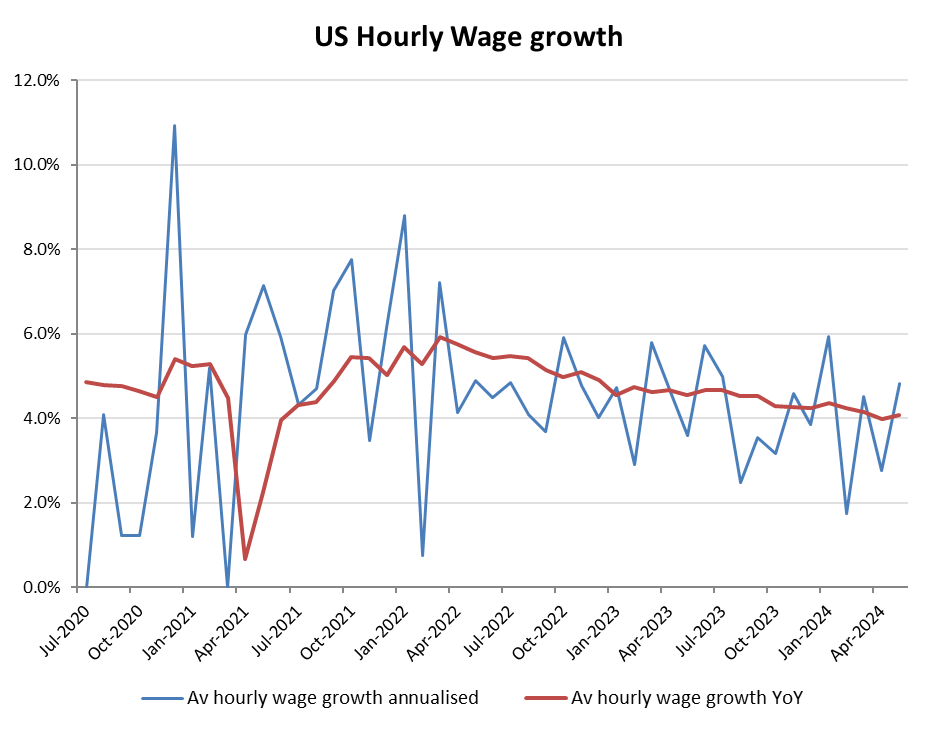

As for wages, the BIS May data suggests a broadly stable picture, with a slight rebound towards +5% after April’s nearer +3%, but with the YoY average holding at just above +4%.

Goldilocks?

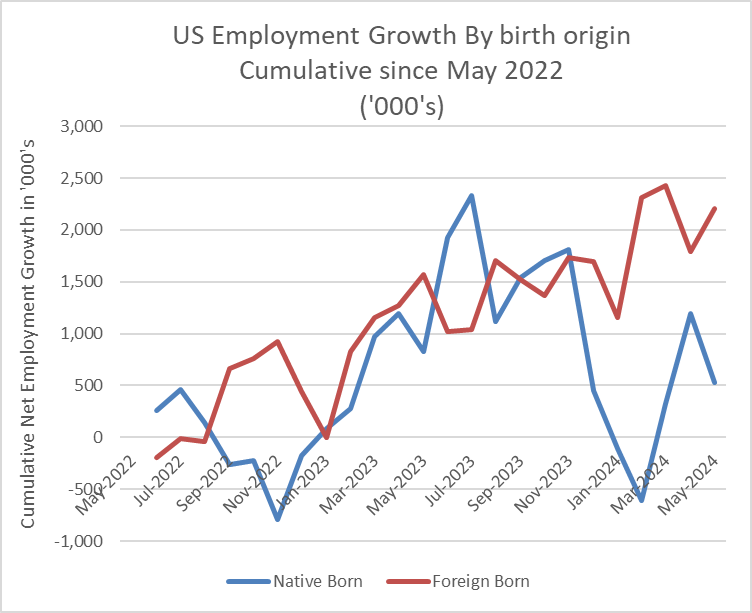

Perhaps more insidious, given the open door migrant policy however have been the construct in these overall employment numbers, with no growth in overall employment numbers for indigenous workers born in the US over the last year. While the social, cultural and impending political cost of this is not something that will be of immediate concern to bond markets, the longer term effects and on Novembers elections could prove more seismic.

Hmm!