Follow the money

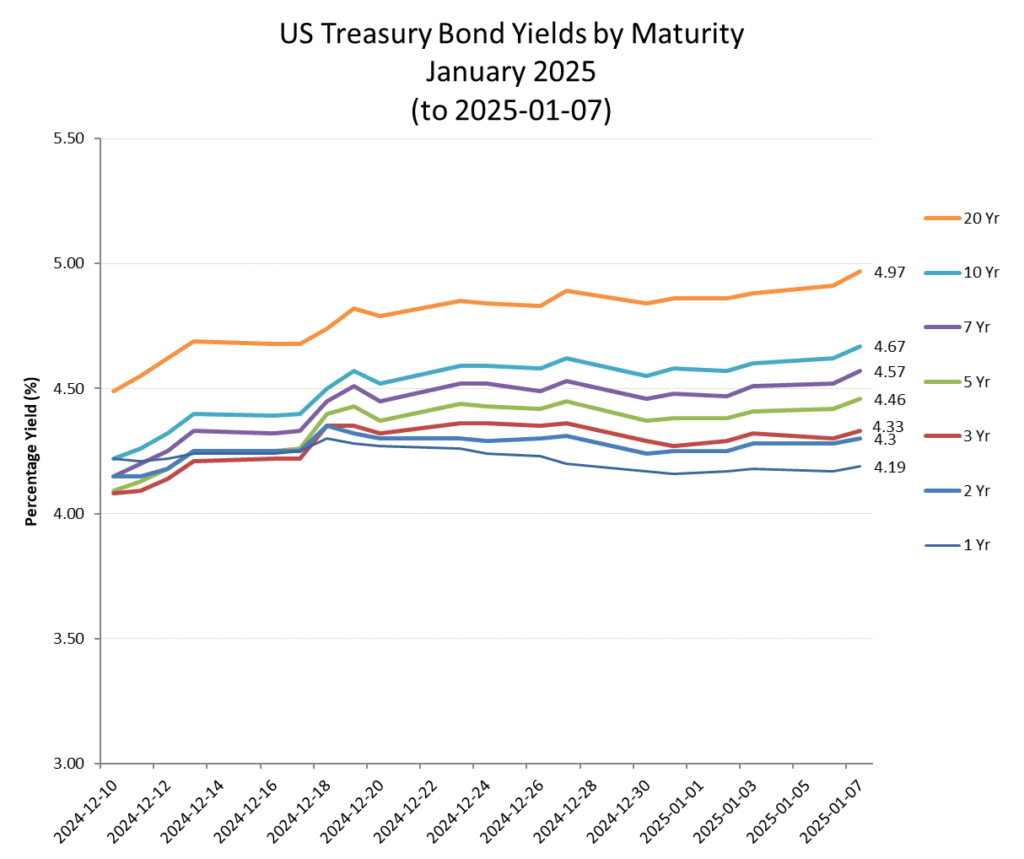

Back in August of last year I highlighted the seemingly incongruous activity of corporate treasurers who had been raising record levels of new debt from bond issuances, notwithstanding the prevailing market ‘wisdom’ and recomendations that interest rates could only fall from those prevailing levels. Well, with long end bond maturies rising, including an approx +50bps increase to almost 5.0% for 20 year Treasuries in just one month, it seems those corporate treasurers were no mugs.

Those proponents of a return to money printing to depress interest rates had failed to understand that this game had been played out as the soaring deficit and inflationary repercussions started to undermine that most sacrosanct policy of protecting the USD reserve status. Facing similar problems as in the late 1970’s and early 1980’s (under the Fed’s Arthur Burns) it seems the electorate have once again been forced to reach for a similar cure, as delivered by Reagan/Thatcher and Friedman/Josephs, albeit this time its the example of Milei in Argentina and Musk’s DOGE proposals to try and avert a full blown currency crisis. Without the MMT money printing, that means a return to market pricing of capital and the normalisation of interest rates, which initially will rise until the deficit spending can be curtailed.

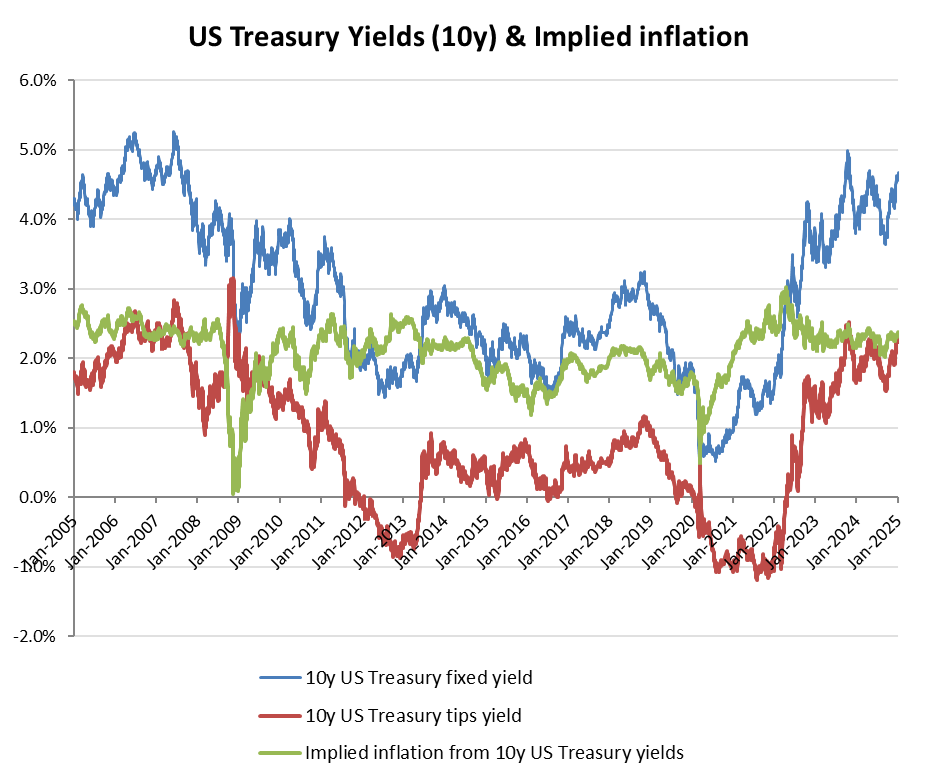

What that means for bond yields is that without QE distortions, these would return to around 2%, with the initial demand for funds by deficit riven governments pushing these towards the upper end of their 1.5-2.5% range. Assuming success on stimulating demand from easing taxes and regulatory impediments as well as unleashing energy production and lower energy costs, then the long run inflation expectation of around 2.5% still being built into treasury bond markets seems sustainable, albeit suggesting medium term bond yields may rise further and perhaps to over 5%.

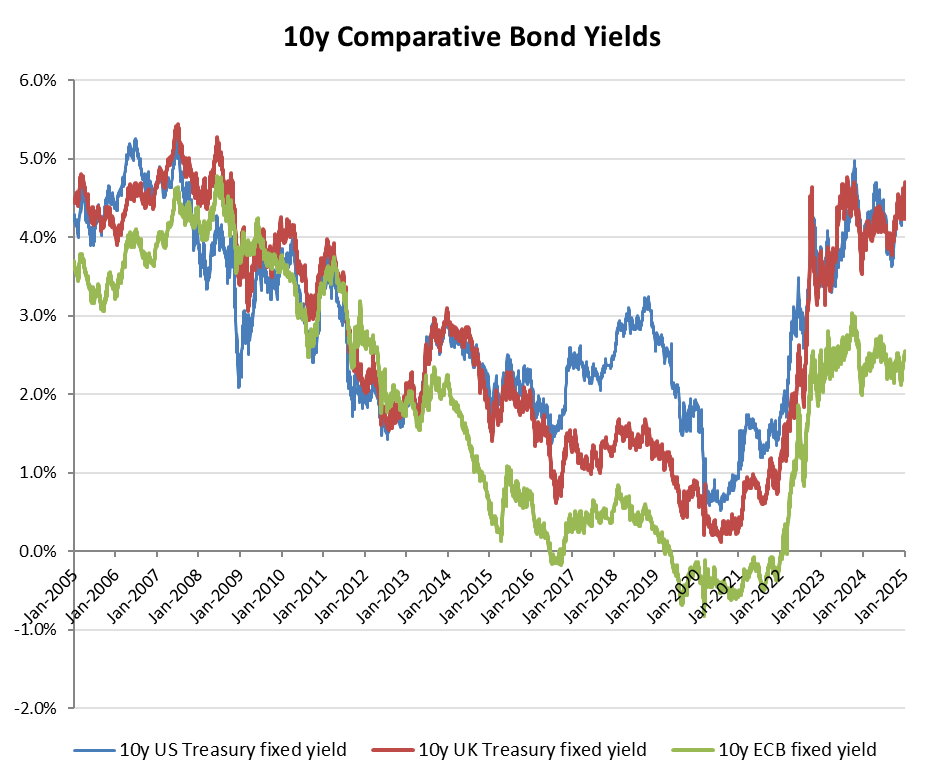

The big question now is who can survive this process of rate normalisation? Clearly and as with the early 1980’s, some tough decisions on government outgoings will be needed, albeit with a policies able to nurture private enterprise and growth to help create that virtuous circle of inward investment into the US and USD which in turn would assist in capping rates after the initial spike. But what about the rest, with Europe seemingly locked into a defict spiral and were attempts to keep supressing interest rates will hasten the forthcoming currency crisis and subsequent exchange controls to stem the inevitable flood of cash into the more attractive US and USD. As this liquidity tide ebbs, expect some shocking exposurers