Do central banks see a problem with Barrick?

There is something rather ironic about Central Banks using deflation as an excuse to print cash which is then used to buy gold shares, which are of course a leveraged play on rising gold prices which in turn are a reflection of the lack of confidence in central bank monetary policies. For the Swiss CB it also makes for an intriguing double bluff in that it is trying to deflate the value of the Swiss franc by creating and selling CHF, but executing this by investing in a hedge against this happening!

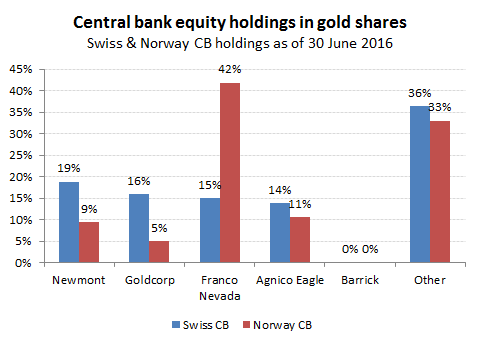

Recent data from the Norwegian and Swiss central banks reveal gold share portfolios worth just under $1bn each.(https://smaulgld.com/swiss-national-bank-built-1-billion-mining-share-portfolio/) In itself, this is unremarkable in a world where the ECB will potentially subsidise a German chemicals company (Bayer) to acquire a GM seeds and pesticides group (Monsanto), where many of its products are banned in the EU. What is of interest however, is the distribution of these gold share holdings and its possible implications. Neither the Swiss or Norwegian central banks are invested in the World’s largest and most liquid gold miner, Barrick Gold.

Swiss and Norwegian central banks have each built up gold share portfolios worth approx $1bn

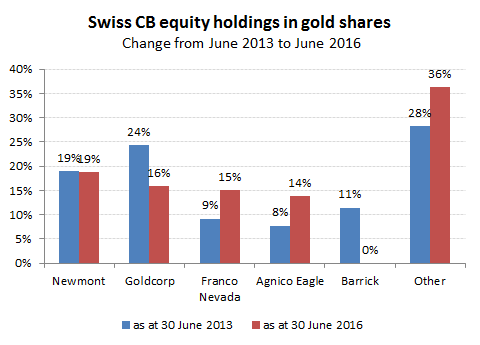

This position on Barrick however is relatively new, as back in mid 2013, the Swiss CB had approx 11% of its gold share portfolio in this bellwether stock. Elsewhere, the stake in Goldcorp has been reduced, the positions in Franco Nevada and Agnico have been substantially raised while the exposure to Newmont has remains broadly unchanged at 19% of the gold portfolio.

Swiss CB has cut its Barrick holding

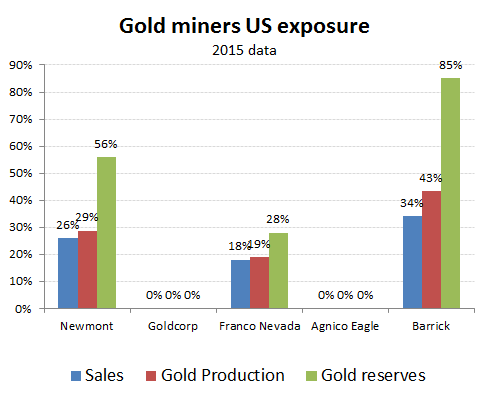

So why are these central banks shunning Barrick? Barrick Gold is covered in our GrowthRater web App (https://app.growthrater.com/) and there is nothing specific on the stock with regards its financing, cost of production or leverage to the gold price (est at 1.20:1) that would ring the alarm bells. Its exploration performance has produced the occasional cock-up, but the current share price is within spitting distance of the proven reserves value if discounted at current production and cash extraction costs. There is one area in which Barrick stands out, but this would normally be regarded as a positive feature; its heavy US exposure (see chart below). Might this now be a cause for concern and if so what has spooked these two central banks to dump the stock?

85% of Barrick’s proven reserves are in the US

COMEX – do we have a problem?

If a 44:1 leverage ratio at lehman’s proved to be excessive, how does the idea of COMEX’s gold cover ratio exceeding 500:1 then? True, physical delivery is discouraged, and for obvious reason, but with western vaults all but cleaned out by Eastern demand and the opening of a competing exchange in Shanghai dealing in only physical delivery one has to ask, ‘What if?’. With Deutsche Bank’s now legendary derivative exposure (>$70tn) and reports of a physical gold delivery failure at its Xetra-Gold, perhaps this denouement is getting a little closer. If so, then a run on COMEX could be rapid and with little chance of honouring the demands for delivery the Fed could either stand back and see where the chips fall or step in again. Given the interlinked derivatives markets, the former could make Lehman’s look like a tea party, which therefore suggests some form of bailout would be needed. The problem though, is that while Lehman/AIG etc just needed dollars, which the Fed can magic up with a few keystrokes, gold is physical and somewhat more difficult to produce. There would however, be another option, and one which also has a precedence; the Government could steal compulsorily purchase the stuff. The prospects of such an outcome is not the sort of thing that would encourage holding gold in the US, either above or below the ground. With 85% of Barrick’s proven gold reserves located in the US, do some of the central banks dumping the stock suspect something?

Executive Order 6102

In 1933 the US government forced its citizens to sell their gold to the Federal Reserve at a fixed exchange rate of $20.67/oz (approx $378/oz in today’s money) which it then proceeded to price at $34/oz for international transactions. The justification was to stimulate the economy with the pretext that it would enable the Fed to issue more credit as the US dollar was on the gold standard. Could this happen again and what might the pretext be this time now that the dollar is merely a fiat currency and not bound by a gold backing?