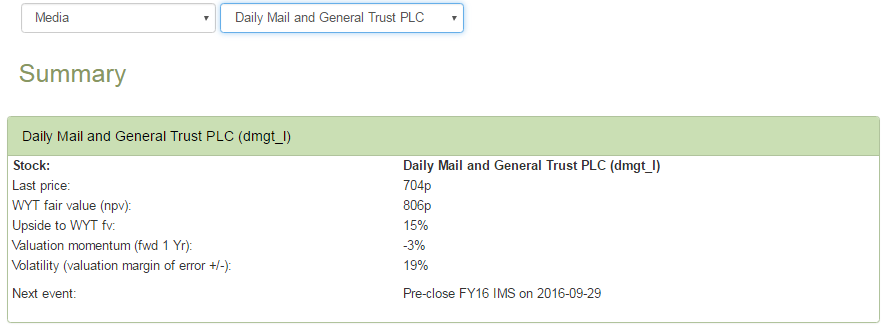

DMGT – added to GrowthRater model portfolio at 704p

DMGT – added to GrowthRater model portfolio at 704p

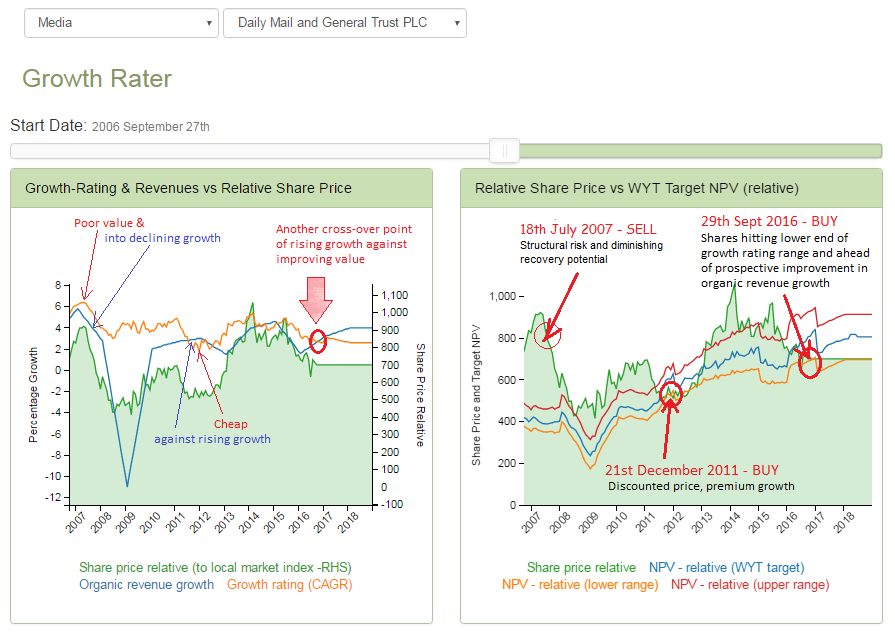

The shares have been off my radar over the last couple of years after having broken above the top of my GrowthRating range (of +2.6-4.1% CAGR) and as organic revenue momentum dropped below this as the structural decay in print advertising continued, falling oil prices impacted the the group’s sizeable interests in Events and B2B and after a series of delays to the RMS (One) launch.

- Revenue momentum however may be turning. Print advertising prospects remain bleak, but everyone and their dog already know this and while endless articles on the gluteus maximus of some reality star is not going to win a pulitzer, it seems to pack the viewers into MailOnline, with the accompanying improvements in advertising income. The key sentiment driver however will be the pick-up in RMS organic revenue growth now that the first product releases from RMS(One) have finally been released. This together with the stabilization in oil prices around $45-50/bbl and we are now perhaps passing the inflection point in the groups revenue trough (see the below charts)

- What this means is that organic revenue growth for the forthcoming year (Sept 2017) could well top +3%, which could put it ahead of the implied growth being priced into the shares at current levels (with an OpFCF yield approaching 7%) while also at the lower end of my GrowthRating range.

- For those that want to find out more for themselves, please click here – https://app.growthrater.com/

- Otherwise I have folded some relevant charts and the last investment summary below.

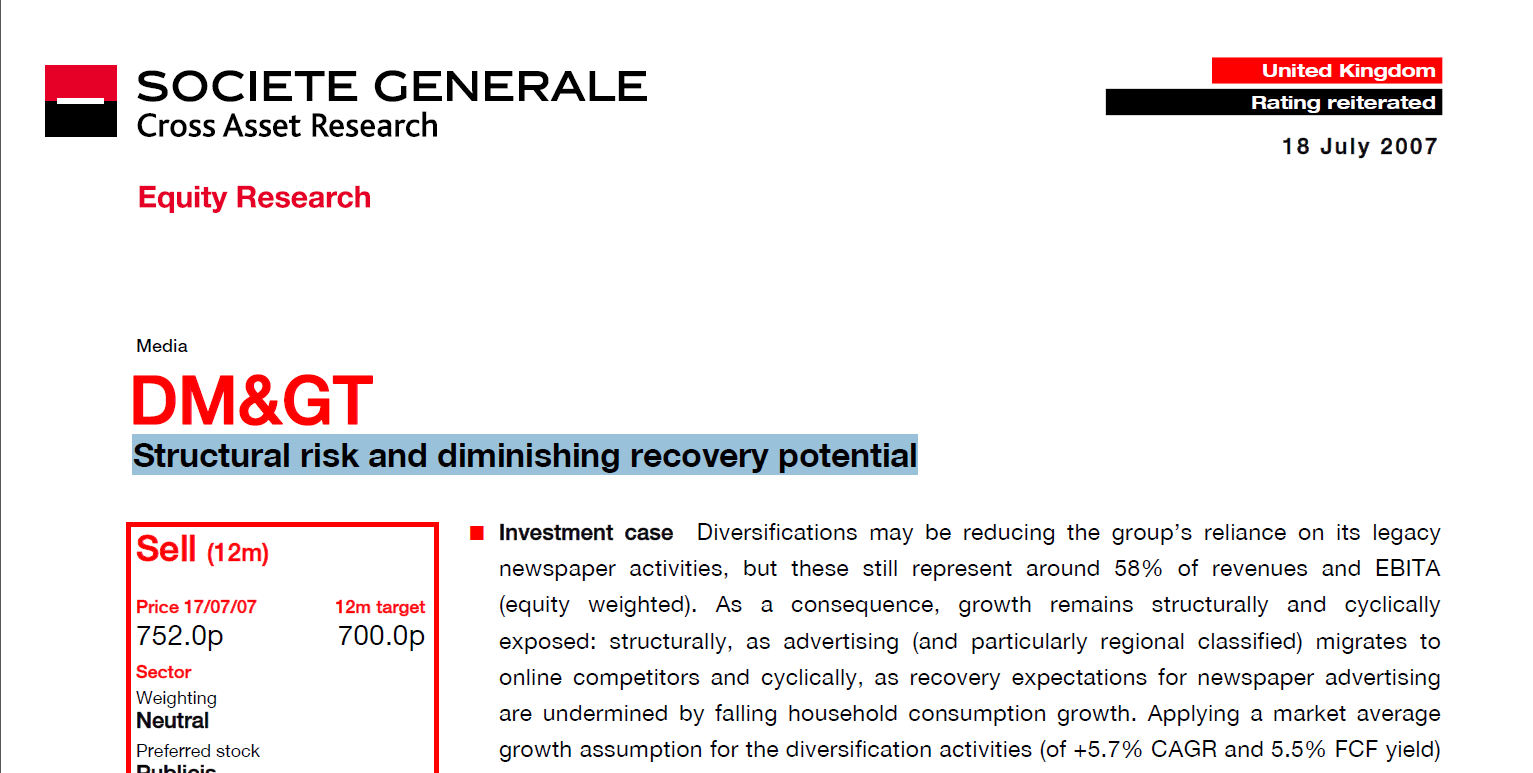

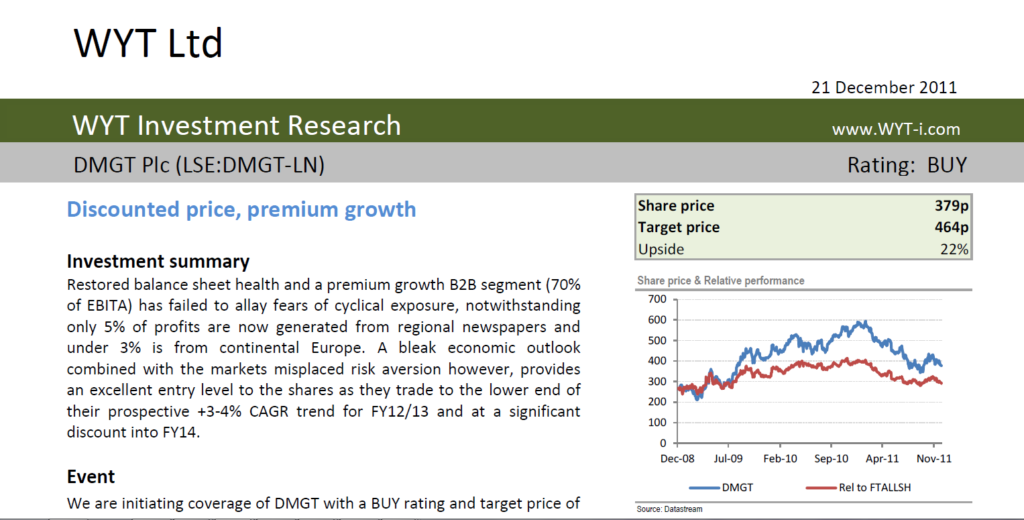

- For those wanting an audit and evidence that this works, I’ve also attached a couple screen shots of old notes of mine which may well be lurking somewhere on the web,

- A SELL note at 752p back in July 2007 when I was at SocGen

- and a

- BUY note I wrote in December 2011 when the shares were at 379p.

Don’t overpay for growth or buy on a declining revenue momentum