GrowthRater portfolio – closing longs on FedEx (+34% with +20% rel) and DMGT (+8% & +5% rel)

To pay for the Christmas presents, I’ll be closing a couple of long positions in the GrowthRater portfolio when markets open. One because it has done what I had hoped for and more (FedEx) and the other because it is increasing looking like dead money, or worse, in the face of deterioration in its markets (DMGT).

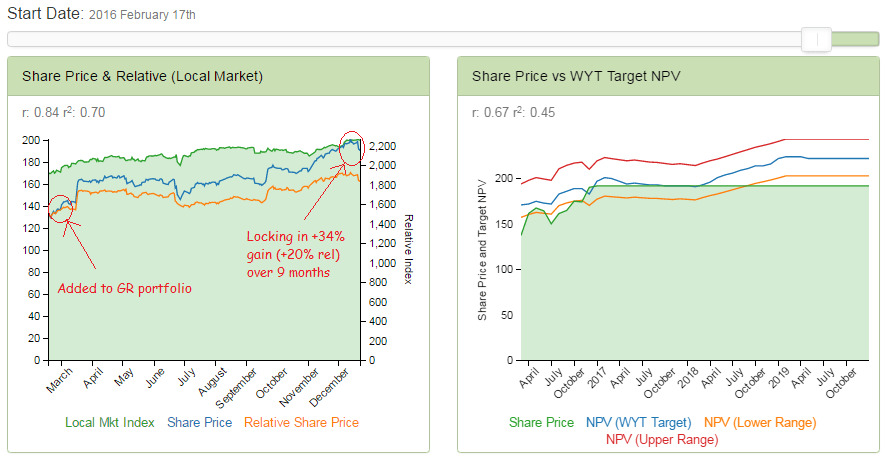

- For FedEx at around $192ps, that means locking in a gain of approx +34% (+20% vs the S&P500) since being bought back in March at $143ps.

- For DMGT however, it is closing what is increasingly looking like dead money as evidence from the commercial TV sector suggests a more aggressive and perhaps extended cutback in UK advertising expenditure ahead of a probably traumatic series of Brexit negotiations. Fortunately, the stock at approx 763p (close on the 23rd Dec) is still up on the 704p entry price back in September (+8% actual and +5% rel to FTAS) and has gone ex a 15.3p final dividend as well, but from here it feels like I would be surfing against the tide and will revisit at a later stage.

Fedex: Having added FedEx to the GrowthRater model portfolio back in March at $143 ps and with the shares currently trading at around $192 ps, I am happy to lock in the +34% gain (and +20% relative to the S&P500).

This is not so much due to the current weak margin performance as it integrates its TNT acquisition and lays down additional capacity at its US Ground operations, as markets should be able to look beyond the initial dilution to the improved operational leverage and margin outlook into FY18-19. My concern relates more to what may be an overly upbeat consensus view on global trade volumes and GDP growth for 2017 which has also been used by the Fed to justify its recent interest rate increase. Rising rate expectations together with threatened trade and tariff barriers by the new President on top of a fracturing EU and an increasingly belligerent tone our of Beijing are all factors which might de-rail these expectations. As we move into 2017, political rhetoric promises to exacerbate these fears as the new US administration starts its trade and stimulus negotiations which I see as providing the catalyst to what now seems to be a seasonal culling of initially complacent GDP recovery forecasts. With the shares on a sub 5% OpFCF yield and without an immediate momentum catalyst for re-rating I would therefore prefer to sit back on the side-lines to await a better entry point further downstream.

Locking in a +34% gain in 9 months

Last trading – H1 FY17: Revenues advanced +20%/+$4.9bn to $29.6bn (Q2: +20% to $14.9bn) with adj EBITA increasing +13.8%/+$314m to $2.6bn (Q2: +2.5%/+$30m to $1.23bn), adj EBITA margins declining by -50bps from 9.2% to 8.8% (Q2: -130bps from 9.6% to 8.3%) and adj EPS up +17.6% from $4.85 to $5.71 (Q2: +8.5% from $2.58 to $2.80) on a -5% reduction in average shares. These results included first time contributions from TNT of $3.7bn to revenues and $124m to adj EBITA (Q2: $1.9bn and $90m respectively) suggesting underlying advances on a pre-acquisition basis of +$3.9%/+$959m (Q2: +4.6%/+$579m) for revenues and +8.4%/+$191m for adj EBITA (Q2: -4.3%/-$52m). GAAP EPS meanwhile increased +7.8% from $4.86 to $5.24 (Q2: +6.1% from $2.44 to $2.29) after expensing -$38m of acquired intangible amortisation and -$126m of integration and other non-recurring items.

Q2 KPI by division includes:

- FedEx Express: Revenues +2.2% to $6.74bn on average daily packages +1% to 4.3m (o/w US domestic -1% to 2.7m and international up +2% to 0.98m) and with average yields up +1% from $19.52 to $19.80 (+3% to $17.39 for US domestic and -4% for international). Adj EBITA meanwhile increased by +5% from $622m to $654m and margins +30bps to 9.7%.

- TNT Express: Revenues of $1.9bn with adj EBITA of $90m ($70m GAAP) and margins of 4.7%.

- FedEx Freight: Revenues +3% to $1.60bn (average daily freight pounds up +0.2% on a +5% increase in yields) with adj EBITA -13% from $101m to $88m and margins -100bps from 6.5% to 5.5% with results impacted by lower weight per shipment.

- FedEx Ground: Revenues +9% to $4.42bn on average daily volumes up +5% and yields up +4% with adj EBITA declining by -12% from $526m to $465m and margins -2.5ppts to 10.5% reflecting network hub expansion (+4new hubs and a +15% increase in space) and higher purchased transportation rates.

OUTLOOK: The initial dilution following the TNT purchase together with the step-up in FedEx Ground capacity has depressed underlying earnings progress although as cost synergies drop-thru and costs stabilise once the new facilities bed down, then this should accelerate margin growth into FY18 & FY19.

For FY17, the group’s financial guidance includes:

- Adj EPS to range $11.85-$12.35 (vs $10.81 in FY16). This excludes

o -$250m TNT Express integration charges and Outlook restructuring

o -$75m of TNT Express intangible asset amortisations

- GAAP EPS to range $10.95-$11.45 (vs $6.52 in FY16). This is before any potential mark-to-market pension adjustments