Wazzup – 26th May 2017

Informa (inf_l) – Plan B still looks the more attractive option .

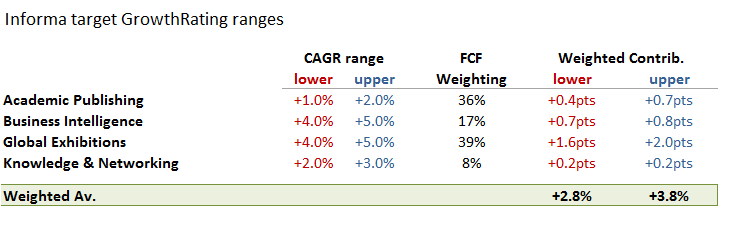

This morning’s AGM trading statement for the first four months of 2017 did little more than “re-confirm” FY17 expectations for another year of “growth in revenues, earnings and cash flow”. While welcome, after the more mixed and poorly received updates recently from UBM and DMGT, it is what comes after Plan A (or GAP as Stephen Carter calls it), that is of greater interest. Having fattened up the business by restoring organic revenue growth by culling the laggards and buying more exhibitions, you’re probably looking at a group with an average growth capacity capped at around +3-4% CAGR (see below table of growth weightings by divisional FCF), but what then? Parking unrelated Academic Journals, Exhibitions and professional information services under one roof is inherently inefficient when compared to a more vertical focus where scale can provide, so the obvious next step is to start crystallising some of the potential merger synergies of these from divestment.

The first of these could be the Academic operations, which are readily saleable in a consolidating industry and would also raise the average growth for the remaining operations at Informa. For journals, scale offers both cost (including IT) and revenue efficiencies, while the high cash conversion and stability make them well suited for private equity, as we’ve already seen such as with BC Partners purchase of Springer and more recently of Macmillan Science. After this, Informa would still be left with two largely separate activities, one offering B2B marketing solutions (Events etc) and the other providing professional information, mainly on a subscription basis. As with UBM, it may just be a matter of time before Informa accepts that the professional information operations would be worth more to a group such as Gartner or IHS Market, which would then leave the rump exhibition operations ripe for a consolidation, perhaps resurrecting the old UBM merger proposal.

For shareholders, what this offers, is a valuation that is currently capped around a +3-4% GrowthRating range as management go through the motions of plan A, but with a longer term back-stop of a more interesting corporate restructuring once fattened up and ready for market – Plan B?

Growth capped at +3-4% including Academic

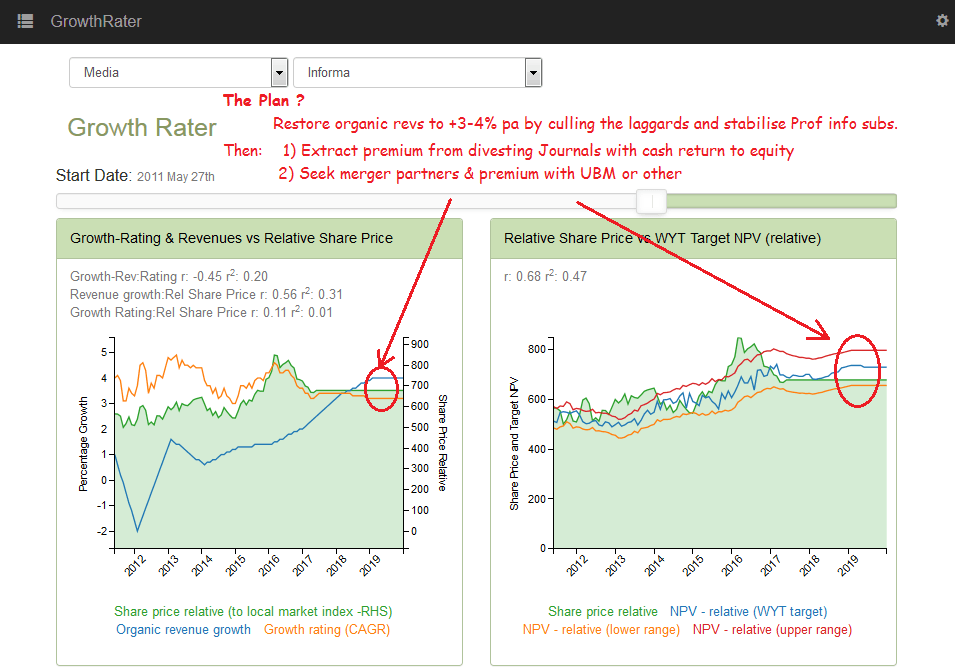

Breakout from a +3-4% CAGR range requires further portfolio change

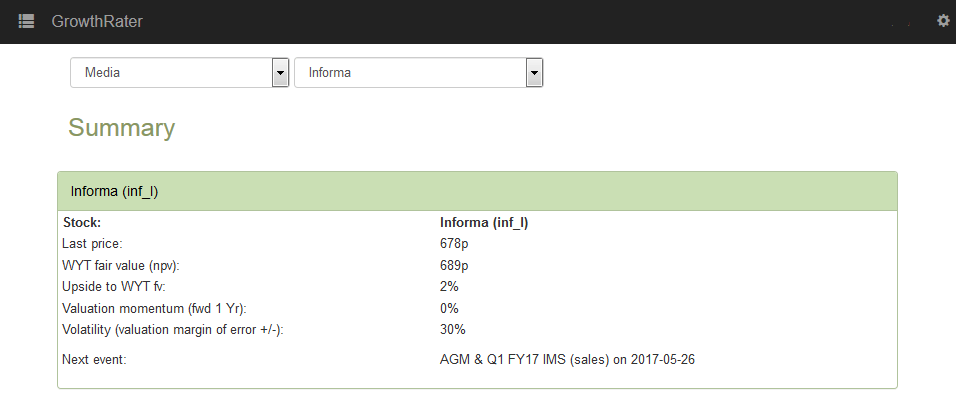

For more detail on the valuation and forecasts, please go to Analytics