US jobs data for May – real trends now being allowed to show through

Is the BLS letting markets down gently that the US economy sucks and to kiss goodbye to a rate hike in June? Beyond the boost in February from renewed shale fracking and an exceptionally mild winter (on mining and construction job formation), US job growth into 2017 has been dire. I’m not referring to the sanitised figures pushed out by the media and financial services industry to keep rate expectations and the US dollar high, but the real numbers before they’ve been skewed by the increasingly aggressive seasonal adjustments.

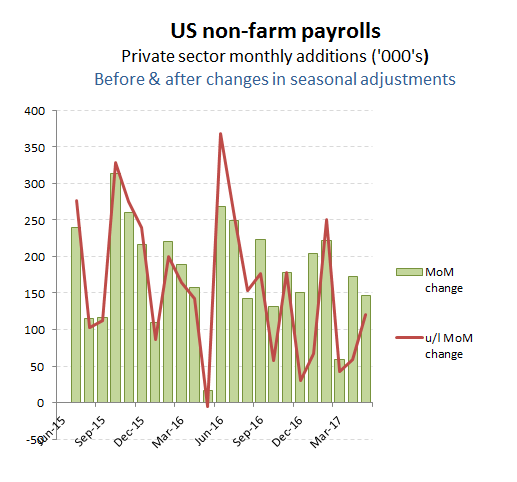

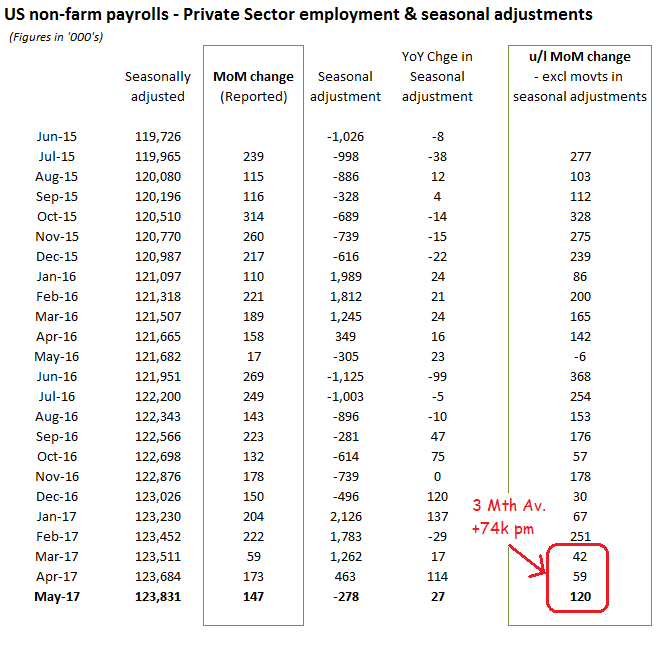

You might have been told that April job growth surged by +211k, but the real growth in Private sector jobs that month before the changes in seasonal adjustment were made was nearer +76k on the original release. Today, that latter figure has been restated down to +59k, while the comparable figure for March has been pared back from an original estimate of +54k, to only +42k. Today’s release for May of a +138k rise in seasonally adjusted net job adds (+147k for Private sector and +120k before changes in seasonal adjustments), therefore can be expected to generate squeals from the press and markets, but the reality is that it is just a slightly more honest reflection of what is really going on. Reports, such as the one below from Reuters, this morning, have continued to pump the narrative of a strong economy enabling the Fed to normalise rates on the basis to the reported BLS job data and the selective use of upbeat GDP forecasts from the Atlanta Fed, while choosing to ignore the underlying data, including the third consecutive decline in US Auto sales for May. Perhaps the Fed is beginning the realise that the old narrative is no longer washing with markets in face of the real situation and is now going to once again pull-back from a rate normalisation. My key question for markets though is what damage this does to the US dollar and whether Trump will have enough of a slowdown in expectations to still be able to drive through is tax and stimulus plans through Congress.

Below, is the sort of stuff being pushed out to markets up until this afternoon – you might notice that the current article on their site has been substantially amended versus the original version this morning, parts of which I have included below with my comments.

https://uk.finance.yahoo.com/news/strong-u-job-growth-expected-may-wage-rise-040248687–finance.html

- Original Report – “Nonfarm payrolls probably increased by 185,000 jobs last month, according to a Reuters survey of economists, after surging 211,000 in April. May’s projected increase would be in line with this year’s 185,000 average monthly job growth.”

- My comment – The actual increase for May is reported at +138k, with Private sector net additions of +147k. Excluding another favourable change in seasonal adjustments (of +20k), the underlying increase in private sector net job growth was +120k. Underlying net private job growth meanwhile was restated down by -17k for April (from +76k to +59k), with March restated down by -12k from the original +54k, to only +42k. On a rolling quarterly basis, that equates to an underlying rate of increase in MoM private sector job growth of only +74k per month.

- Original Report – “Another strong jobs report would help the Fed proceed with another rate hike at its June meeting, by supporting its contention that recent weakness in retail sales and inflation data will prove transitory,” said Josh Wright, chief economist with recruitment software provider iCIMS in Matawan, New Jersey.

- My comment – “Another strong jobs report”? As the saying goes, “rubbish in, rubbish out”. The last decent month for underlying jobs growth was February’s +251k MoM net job increase, albeit benefitting from un-seasonally warm weather (more building activity) and the rebound in fracking activity on the recovery in oil prices. The press will probably lead with the story that May was a “Huuge miss”, but the reality is that is was actually a lot better than the previous couple of months and it was just that expectations were way too high because that were being worked off the dodgy stats.

- Original Report – “Minutes of the Fed’s May 2-3 policy meeting, which were published last week, showed that while policymakers agreed they should hold off hiking rates until there was evidence the growth slowdown was transitory, “most participants” believed “it would soon be appropriate” to raise borrowing costs.

- My comment – Blah, blah “keep buying the US dollar because we’re going to tighten” – well perhaps not any more

- Original Report – “The Atlanta Fed is forecasting GDP increasing at a 4.0 percent pace in the second quarter.”

- My comment – Well, not exactly as they cut it from +4.1% to +3.7% on 26 May. Also interesting that the Atlanta Fed forecasts was singled out when it had been the upper outlier in a Q2 GDP growth range of +2.1-4.1%. Selective reporting again to support the narrative of rising interest rates?.

- Original Report – “The economy needs to create 75,000 to 100,000 jobs per month to keep up with growth in the working-age population”.

- My comment – Two points

- 1) What jobs? More low paid temporary jobs or those that people can raise a family on?

- 2) Excluding changes in seasonal adjustments, the average MoM job growth in the private sector has been only +74k per month over the last quarter – Ooops!!

May US non-farm payrolls – the reported numbers

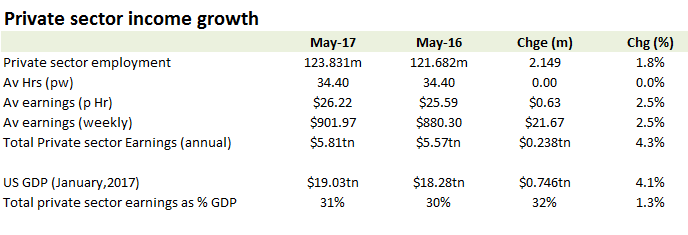

For those that like to extrapolate the fictional data into annual statistics for average earnings growth will see the +1.8% annualised wage increase (from $26.18 per hour in April to 26.22 in May) on flat average hours is hardly the heady stuff to excite fears of wage inflation. On a year on year basis, that represents an actual increase in Av earnings of approx +2.5%.

Av earnings up only +1.8% annualised

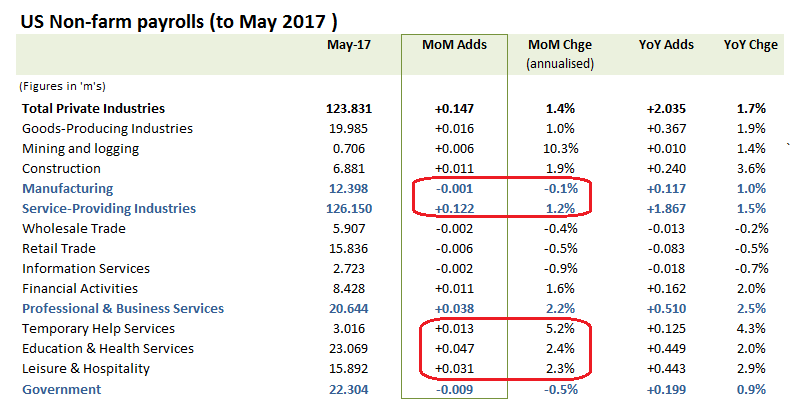

If Trump wanted to rebuild manufacturing jobs and raise middle class earnings, there’s little evidence in the May statistics to suggest this is working, with manufacturing employment actually contracting slightly in the month. Higher rig count and fracking activity on the oil price bounce continues to support ‘mining’, but the main areas of job formation in the month again came from ‘Hospitality & Leisure’, Education and Health’ and ‘Temporary’ categories.

No evidence of a manufacturing revival here