Wazzup today in the markets – 18th May 2017

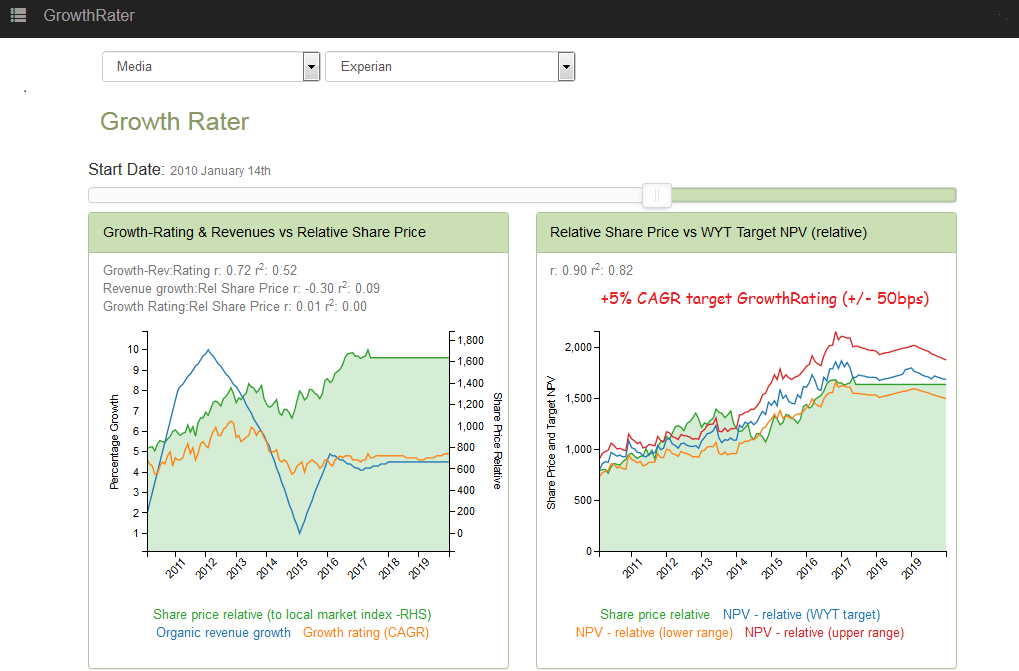

- Experian (expn_l) – FY17 results: Sacrificing marketing expenditure to make the margin target .

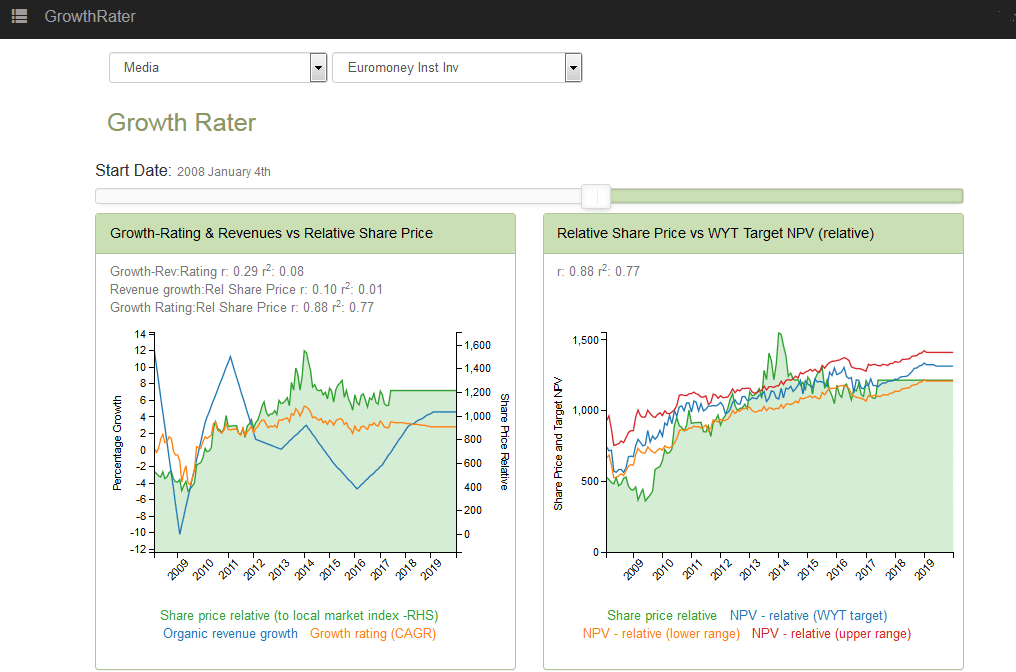

- Euromoney (erm_l) – H1 FY17: Signs of stabilisation, but perhaps a little early to celebrate the recovery

- UBM (ubm_l) – added to GrowthRater portfolio: As price closes below 700p . .

.

Experian (expn_l) – FY17 results: Sacrificing marketing expenditure to make the margin target

For the year just reported, the group delivered on it guidance for a second half recovery in margins, although it seems only at the expense of a sharp drop in marketing investment which raises the question as to the potential impact this may have on growth and margins into the current year not withstanding a similar guidance for both by the company as for last year. The stock however is not aggressively priced, trading on a prospective OpFCF yield of 4.7% discount a GrowthRating of approx +4.6% CAGR which is broadly in line with the current organic revenue growth trend as well as the group’s trailing average GrowthRating over the past 10 years.

Last trading update – FY17: Results were in line with expectations, with a +5-4% increase in organic sales (excl-incl CCM) driving a +7-6% rise in EBIT, margins up +60bps to 27.7% (+30bps at =fx) a +6-5% advance in adjusted PBT and +5% improvement in adj EPS (to $0.884-$0.924), supporting a +3.7% rise in DPS. Included within the continuing EBITA advance of +$54m however, was a -7%/-$23m reduction in marketing and customer acquisition expenses (to $322m). For FY18, guidance is similar to that given for FY17, that being for MSD organic sales growth, with stable margins and “further progress in adjusted EPS”.

FY17 – the numbers:

Revenues: +2.0%/+$93m to $4.643bn ($4.335bn excl CCM), incl approx +4.1% organic (+40bps to approx +4.6% excl CCM), -2% fx and -0.5% acquisitions. Organic includes:

- N.America: +5% to $2.5bn (+8% credit, +8% Mktg and -2% consumer)

- LatAm: +9% to $730m (+6% Credit,+34% Decision, +39% Mktg)

- UK & RoI: +1% to $807m (+3% credit, +5% Decision, +5% Mktg, -9% consumer)

RoW: +5% to $341m (-3% credit, +21% decision, +16% Mktg)

• EBITA: +4.6%/+$55m to $1.261bn ($1.213bn excl CCM), incl approx +6% organic (+7% excl CCM) including at =fx:

- N.America: +11% to $781m (margins: +110bps from 30.7% to 31.8%)

- LatAm: +3% to $251m (margins: -140bps from 35.8% to 34.4%)

- UK & RoI: -4% to $246m (margins: -160bps from 32.1% to 30.5%)

- RoW: +47% to -$3m (margins: +570bps from -4.8% to -0.9%)

Outlook: The group is not giving much away with a repetition of its prior year guidance of MSD organic sales growth and “stable” margins (+5% and +30bps underlying respectively in FY17), although as can be seen from last year’s splits, this included significant volatility by region and product line. It also included a substantial margin tailwind from lower ‘Marketing & Customer Acquisition’ costs which fell by -7%/-$23m and as a proportion of sales by 86bps from 8.3% to 7.4%.

Priced at what it’s delivering – MSD growth

Euromoney (erm_l) – H1 FY17: Signs of stabilisation, but perhaps a little early to celebrate the recovery

We may be nearing the cyclical trough perhaps, but it still looks a little early to chase a recovery this side of what may prove to be some tough Brexit negotiations and with the shares trading at around the middle of its historic GrowthRating range of +3-4% CAGR.

For more see Analytics

Last trading update- H1 FY17: A combination of easier comparatives on subscriptions and stabilising events managed to post the first positive organic revenue growth in two years, albeit after the -5% for Q1, the +1% rise in Q2 still left the H1 average down by approx -1.3%. Including a +10ppts fx tailwind however, and H1 reported revenues increased by +5%/+£9m to £203m, with adj EBITA rising by +5%/+£2.2m to £49.0m (-5%/-£2.4m excl +£6.4m from fx). With adj PBT rising by +5% to £49.1m, adj EPS increased by +9% from 29.2p to 32.7p (vs our 32.2p estimate), while group delivered on its promise to improve the dividend payout with a +26% uplift in interim dividend from 7.0p to 8.8p (albeit below our more generous 9.48p expectation). Net debt at end March of -£84m was broadly in line with our forecasts, albeit with a better than expected W/Cap release of £17m offset by a higher tax payment of £13m and after the -£194m of share buybacks.

This included:

- Subscriptions: +1.5% organic to £126m (vs +1%) reflecting some downward pressure on asset managers fee income, but stabilising commodity markets.

- Advertising: -13% organic to £16m reflecting the continued impact on UK banks of Brexit

- Sponsorship: -2% organic to £27m – as above, but with Q2 stabilising to +5% after Q1’s -14%

- Delegates: -5% organic to £27m including a Q2 pick-up to +1% after -14% in Q1

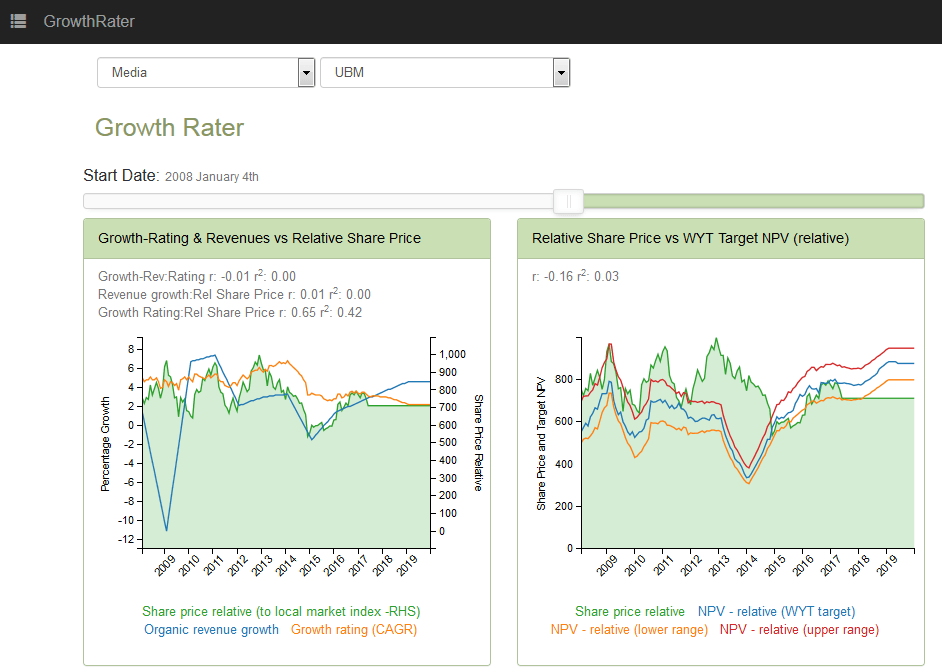

UBM (ubm_l) – added to GrowthRater portfolio: As price closes below 700p

Markets weren’t overly enthused by yesterday’s AGM statement, with the shares closing at 699p. As I said I would in yesterday’s post if the shares dropped below 700p, I added the stock to the GrowthRater portfolio. At this level they offer a +10% upside to the NPV, which also includes an improving valuation momentum. While the recent acquisition strategy of acquiring low growth Event assets is not something I support as it smacks of an attempt to bump up short term EPS rather than drive growth, markets seem to have also seen through this by de-rating the stock to a current GrowthRating of only around +3% CAGR, which on my forecasts could fall to nearer +2% by FY2. As a UK listed stock, but with a substantially offshore income stream, it also offers an element of hedge to the forthcoming Brexit negotiations, or perhaps the lack of them. .

.