Pearson – resorting to one-off non-cash tax items to try and spice up a tired recovery story

Pearson was for a while the darling of the sector, with a recovering top line supported by substantial cost reductions and an fx tailwind from the appreciation in its principal trading currency, the US dollar. Beyond this however, there was only limited evidence that the ship is being turned about, in terms of what really counts, it’s organic growth outlook. Flat organic sales reported for the 9 months confirms that the +2% reported in the first six months was indeed more a function of phasing benefits rather than a validation that years of restructuring and digital investment were now going establish an upward path towards market average growth.

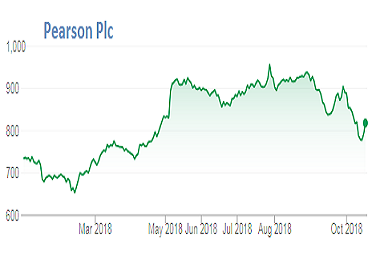

While today’s upward revision in ‘adjusted’ EPS guidance looks impressive, this is entirely a function of one-off and largely non-cash tax and related interest benefits. Beyond this cosmetic flummery, little has actually changed and with some of their ‘great’ growth markets (China, Brazil and South Africa!) looking decidedly wobbly, one might ponder whether the stock has got a little ahead of itself. Indeed, the share price chart seems to be crying out for a ‘technical’ analyst (someone with a ruler) to start drawing some straight lines between some of the recent declining peaks and troughs; not that I would condone such blasphemy!

On a more fundamental perspective however, one might come to a similar conclusion