Wazzup today in the markets – 17th May 2017

- UBM (ubm_l) – AGM trading update: Spartan disclosure, but solid value proposition

- .Tarsus (trs_l) – IMS: Forward bookings for FY17 +9% (lfl) – too good to be true? .

.

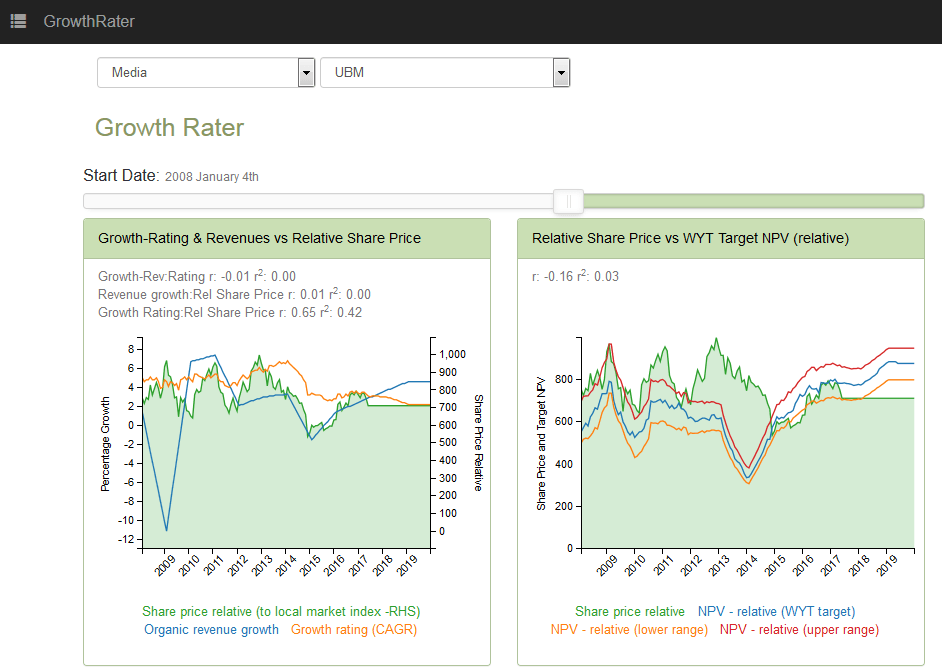

UBM (ubm_l) – AGM trading update: Spartan disclosure, but solid value proposition

Having gone ex the big final dividend and presenting another lean IMS statement, the shares are becalmed, although should they drift back to under 700p, they may be worth a look at (see below).

AGM IMS

I hope you weren’t holding your breath for this as, on the important issue of outlook, UBM’s trading update is no more than a ‘cut and paste’ job of last year’s.

- Today’s AGM trading update: “UBM has performed in line with management expectations and the outlook for the full year is unchanged.”

- Last year’s AGM trading update: “UBM has performed in line with management expectations and the outlook for the full year is unchanged.”

While a dull, but consistent message akin to what RELX has been churning out each year has it’s merits, a little more detail on trading would have been welcome (eg forward bookings, performance by category and region), particularly given the substantial corporate rotation in trading assets which over the past three years has included over £1.1bn of acquisitions and almost £600m of divestments.

AGM IMS statement below + my annotations

“As expected, the performance at the spring fashion events was mixed, with good growth in Sourcing and a successful launch of IFF Magic in Japan offsetting some of the challenges in the other US fashion segments. [remember the $972m acquisition of Advanstar in Oct 2014? – we do!]

Elsewhere in the portfolio, MD&M West, Enterprise Connect and Seatrade Cruise delivered good growth, the Game Developers Conference was solid and both phases of Hotelex & FineFood in Shanghai grew strongly. The Allworld integration is progressing well and performance is in line with the business case. FHI in Jakarta showed strong growth. The sales excellence roll-out in EMEA is nearing conclusion and the roll-out in Asia has begun.

The pipeline of bolt-on acquisitions continues to be good. During the period we acquired a small Turkish event in the lighting segment at an attractive multiple. [- on historic perhaps, more than prospective!]

UBM’s focus remains on accelerating organic growth and driving further margin improvement in line with the Events First strategy.” [consistent with its FY17 guidance for “higher underlying revenue growth” (vs +1.5% in FY16) and an “improvement in margins”]

Investment summary

Each new management has a big play. For Tim Cobbold, this has included the further consolidation of activities around Events, but with a focus on mature markets. While, this can provide a kicker in terms of earning accretion and ROIC as a lower growth business will have this reflected in a higher initial yield priced into the acquisition, the longer term consequence is the inevitable drag this creates on average organic growth prospects and therefore the OpFCF yield and GrowthRating that should be priced in to stock. Markets it seems are sensitive to this, which is why the stock is trading on a 6.0-6.5% prospective OpFCF yield to discount growth at only just over +3% CAGR. Strip out the dilution from discontinuing some rump marketing service activities however, and organic revenue growth for the core event operations may not be too far adrift from this growth rate this year, which is why I’m happy to price in a GrowtRating range of +3-4% CAGR. The stock may be becalmed having gone xd the big final dividend (16.9p), but the underlying valuation looks well supported by the growth delivery, while the limited exposure to UK domestic markets offers a defensive support ahead of what may prove to a traumatic period of Brexit negotiations. Lurking ever present in the background meanwhile, remains the prospects for further industry consolidations such as with Informa or ITE.

Having gone ex the big final dividend and presenting another lean IMS statement, the shares are becalmed, although should they drift back to under 700p, I’ll add some to the GrowthRater portfolio

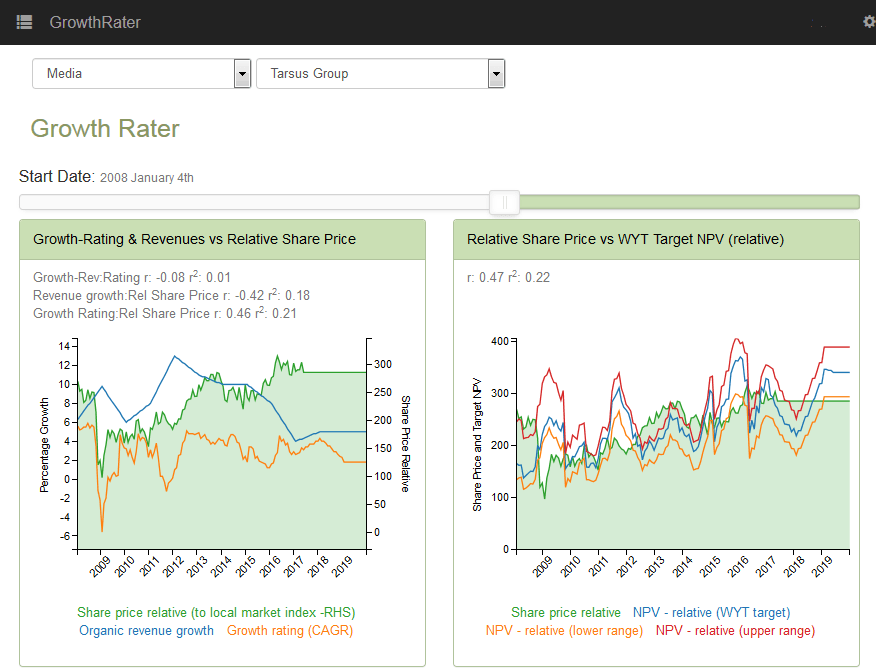

Tarsus (trs_l) – IMS: Forward bookings for FY17 +9% (lfl) – too good to be true?

While other Event operators are reporting slowing organic sales growth including heavy falls in markets such as Turkey, Tarsus continues to sale ahead, reporting like for like forward bookings for FY17 ahead by +9% and predicting another upbeat annual performance.

“We are excited about the organic growth prospects of the business and we remain confident about the outlook for 2017.”

Full trading update can be found here