Wazzup today in the markets – 16th May 2017

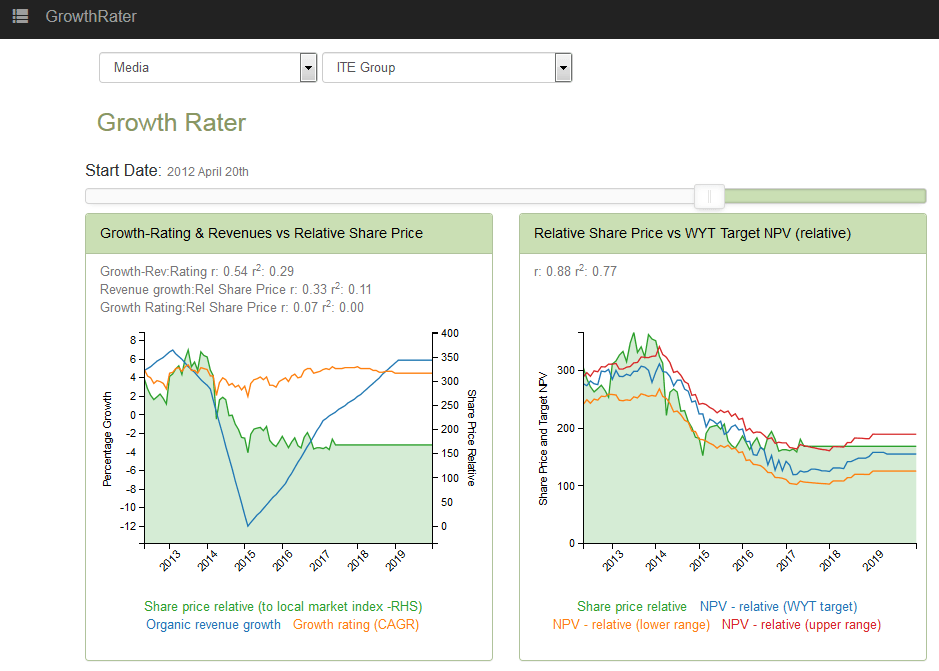

- ITE (ite_l) – H1 FY17 results & strategy review: Underwhelming on both .

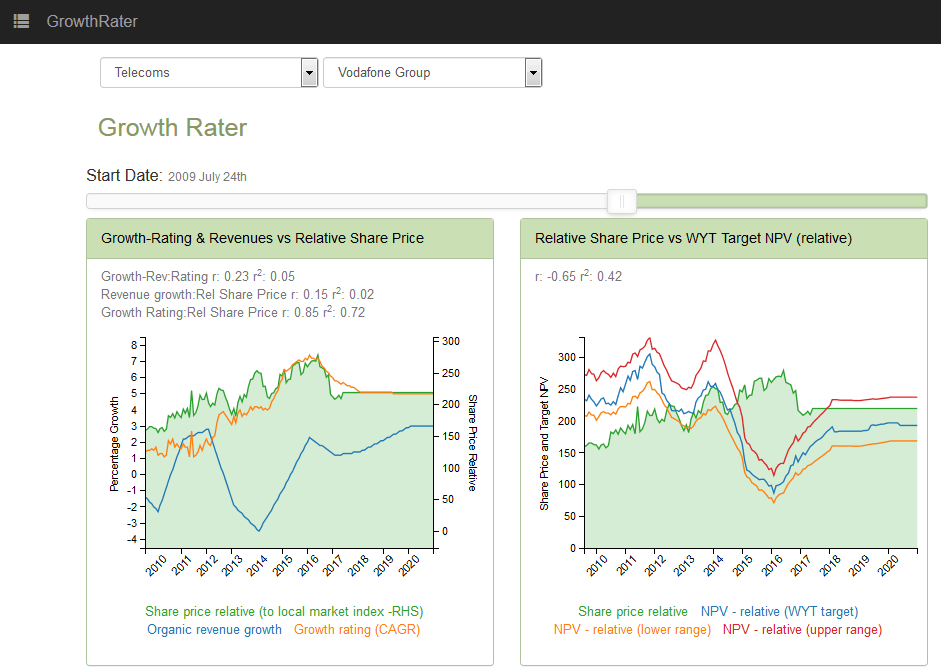

- Vodafone (vod_l) – FY17 results: Value trap as investors chase yield

.

ITE (ite_l) – H1 FY17 results & strategy review: Underwhelming on both

No real surprises on this morning’s H1 results and strategy update.

- Current trading is still struggling outside of Moscow, with underlying profits expected to be broadly flat for another 18 months, before the big bounce in FY19 with the projected ‘Double digit’ growth.

- The ‘new’ strategy (called TAG) is a fairly standard one of increased focus around the major brands, or those with scope to scale, with an additional £20m of investment being put behind it to be spread over three years, but with the P&L costs excluded from the ‘Headline’ numbers.

- Net financial derivatives at end March increased to -£24.3m, which if added to net debt of £55.2m would take the effective liabilities up to -£80m

- Valuation: No particular change from my view a couple of weeks ago. Beyond the medium term operating margin target to return to “high 20’s” again, the stock looks as though is had run high enough ahead of this announcement. If the new team screw up, there may be a speculative play, albeit lower down. In the meantime UBM and Informa look more appealing on a valuation/momentum/speculation perspective.

H1 FY17 summary

- Revenues: +9.4%/+£6.0m to £69.6m

- o/w organic of +2% (Q1: +4%, Q2: 0%)

- o/w fx of +9.2%

- o/w Acqs of +5.2%

- o/w Biennials/timings of -7.1%

- EBITA (adj): -21%/-£3.0m to £11.3m (margins -630bps from 22.4% to 16.2%)

- Net interest: +23%/-£0.3m from -£1.3m to -£1.6m

- Associates: -14.7%/-£0.7m fro £4.5m to £3.9m

- Adj PBT: -23%/-£4.0m from £17.5m to £13.5m

- Adj tax rate: +390bps from 13.4% to 17.2%

- Mins: -30% from £2.5m to £1.8m

- Net income (adj): -26/-£3.2m from £12.6m to £9.4m

- EPS (adj): -25% from 5.2p to 3.9p

- DPS: unchanged at 1.5p

- Amort (acq intangibles): -£7.8m vs -£7.6m

- Impairments: £0m vs -1.2m

- Exceptionals: -£2.5m vs £0.7m

- Tax rate (IFRS): -3.7% vs 9.1%

- EPS (IFRS): -79% from 2.80p to 0.60p

- Net cash: -£55.2m (+£3.9m vs year end of -£59.9m)

- Financial derivatives: -£25m vs year end of -£24.2m

Full company results & strategy presentation here

All covered at: https://app.growthrater.com/

Vodafone (vod_l) – FY17 results: Value trap as investors chase yield

A +4-8% EBITDA growth guidance on a >5.5% prospective dividend yield that is forecast to be covered by FCF may sound like a compelling combination for income starved investors. These growth metrics however, are only achievable by stripping out the bad stuff and against a lowered and restated base, (by deconsolidating Vodafone India ahead of its agreed merger with Idea Cellular), rather than being reflective of a real underlying improvement in trading, which continues to struggle to breach inflation, notwithstanding only recently coming off a heavy investment cycle.

Trading update – Q4 & FY17: Year-end declines across UK and India left Q4 organic sales growth at only +0.2% and the FY17 at +1.2%, while the deconsolidation of Vodafone India from the FY and restated prior year obscured the fact that adjusted EBITDA on the previous scope would have come in at €15.751bn and therefore at the bottom end of the €15.7-16.1bn (+3-6% org) guidance range made in Nov 2016.

Q4 & FY17 – the numbers: Revenues -4.4%/-€2.2bn to €47.6bn (incl organic of +1.2%), with adj EBITDA flat (-€6m YoY) at €14.1bn (+5.8% organic claimed) after a -6.1% contraction in OpEx. After lower D&A (-2%/-€207m to €10.2bn vs CapExp of -€8.1bn), financing charges (-8%/+€71m to -€862m) and higher associates (+173%/+€104m to £164m), adjusted PBT on continuing operations advanced +13%/+€376m to €3.272bn, which leveraged up to a +17% increase in adj EPS on continuing activities from € cents 6.87c to 8.04c on reductions in minorities (-24% to €234m) and adj tax rate (-120bps from 26.6% to 25.4%). Increasing the final dividend by +7.4% to €10.03c, the group raised the FY17 DPS by +5.6% from 13.98c to 14.77c, equating to approx €4.14bn pa.

Q4 organic revenue growth included:

- Service: +1.5%

- Europe: +0.1%

- o/w Germany: +1.2%

- o/w Italy: +2.8%

- o/w UK: -4.8%

- o/w Spain: +1.3%

- AMEA: +6.8%

- Vodacom: +3.8%

- Turkey: +13.9%

- India: -11.5%

OUTLOOK: Excluding Vodafone India, the group is guiding for a +4-8% organic growth in adj EBITDA (at =fx) to €14.0-14.5bn for FY18 (vs €14.2bn in FY17), with FCF of “around” €5.0bn.