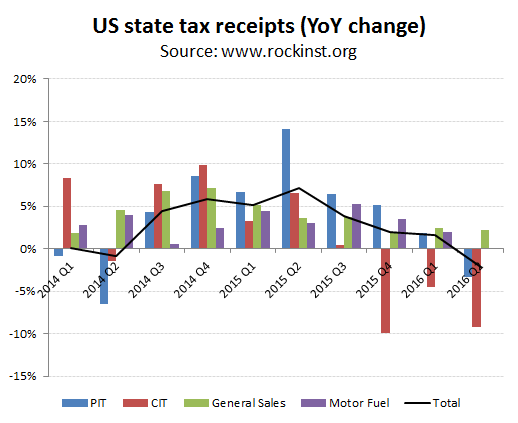

US state tax receipts fall by -2.2%; hardly a prelude for a Fed rate increase!

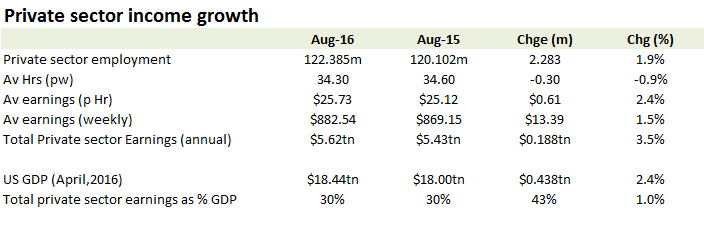

Sometimes the ‘facts’ are difficult to reconcile, particularly when these are government statistics. For Yellen this has included maintaining the fiction that all is well with the US economic recovery, but not so good that the Fed should take its foot off the monetary accelerator. Along with other market commentators we monitor the monthly data on job formation and wages from the bureau of Labor. From these non-farm payrolls one can extrapolate the rate of private sector income growth, which for the last reported month of August suggest total private sector income growth of approx +3.5% pa. While at the cooler end of the Goldilocks growth range, it was not so low as to leave the prospect for a rate rise so remote that no one would want to hold US dollars any more.

Recent analysis by the Rockefeller Institute on US state tax receipts however suggest a weaker economic and income environment with Q2 data showing state tax receipts declining by -2.2% YoY, including a -3.1% drop in personal income tax. While the latter is being excused as a lagged reaction to weaker stock markets and therefore lower taxable disposal gains, this would suggest a shocking propensity for US private investors to sell out in the brief market lows between Sep-Oct 2015.

http://www.rockinst.org/pdf/government_finance/state_revenue_report/2016-09-21-SRR_104_final.pdf

Q2 2016 state tax receipts down -2.2%

This reversal in state tax receipts also extends to Corporate tax receipts, which were down by -9.9% in Q2, but not to sales taxes. Notwithstanding this evidence of contracting personal and corporate income, sales tax receipts were still up, albeit at a hardly blistering rate of +2.2% YoY.

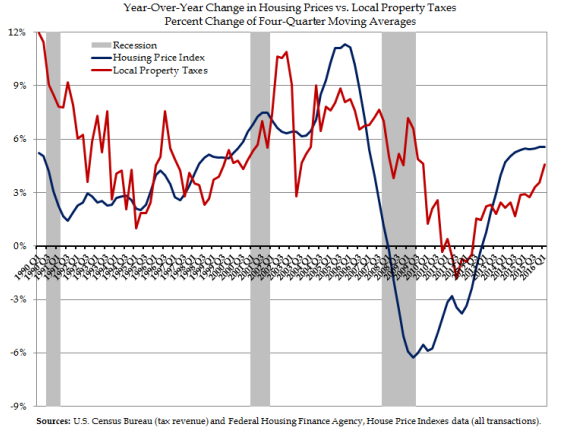

Squaring the circle of expenditure exceeding income is clearly indicating a continued reliance on debt financing which in turn needs the Fed keep rates low and available credit high. Further evidence of this unbalanced and dis-functional recovery can also be seen from the continued growth in local property taxes which are driven by rising property prices. Without income growth support, rising prices are also a function of lower mortgage rates and increased credit availability, with these rising valuations also providing support for additional loan driven consumption growth elsewhere. Welcome back to pre-2008. It doesn’t look like much has changed except that with rates near zero this time, what next – helicopter money, with homeowners paid interest to borrow?

Local property tax receipts still rising

Show me the money moment.

Income based taxes are lower and are currently only being partially offset by higher consumption based taxes which are credit based. Not exactly an environment likely to encourage the Fed to choke this off with a rate increase is it, regardless what the non-farm payroll data might suggest. For those you following US state expenditure sensitive industries, such as K12 educational publishers, falling state tax receipts suggests a perhaps tougher round of state expenditure budgets for the FY16/17 than might have been previously anticipated.