A Reserves based Valuation for Gold Miners

Resources companies can often present a quandary for traditional valuation techniques. Is a hole in the ground a potential asset, or the guys digging it worth an opportunity premium in case they find more gold? They are of course a bit of both, but the long lead times from sinking the capital to delivering the return and demonstrating the excess CROIC and therefore potential valuation premium, can be obscure. As a consequence, an investor might wish to include something a little more tangible as a valuation second opinion, such as a reserves based valuation – ie valuing what’s in the ground.

That’s not to deny there are plenty of potential issues with attempting such a feat, but when a miner offers an analysis of its proven reverses, it doesn’t take a rocket scientist to apply the unit cash costs of extraction together with the extraction rate to arrive at a Net Present Value for these reserves and even flex this into some tables to see the stock price potential sensitivity to differing assumptions on the future gold price. Since I’m not a rocket scientist I have therefore done this and below I have included such analysis for a couple of the larger groups, Barrick Gold and AngloGold Ashanti. That the stock prices do seem to be sensitive to the results of such an analysis meanwhile suggests that there may be many other not-rocket-scientists out there using similar ‘quick and dirty’ reserves based valuations.

Some caveats, and there are many, include:

- The estimated reserves: These are estimated at a given price for the extracted mineral, usually at healthy discount to the prevailing market price. Barrick’s proven reserves at end 2020 for example where calculated assuming a market gold price of $1,200/Oz, which was a discount (cushion) of approx -25% to the then prevailing market price. At a higher price, additional reserves would no doubt become profitable to extract and therefore increase the overall level of published reserves, but this would also have the effect of raising the expected average unit extraction costs. We have not attempted to estimate the potential expansion in overall reserves on differing levels of future market gold prices, but our sensitivity tables do include differing assumptions on unit cash costs as well.

- Capital Structure: Our valuations are included on a current balance sheet structure and therefore associated tax liability for each company. A potential acquirer however, might well wish to substantially leverage up the balance sheet to also increase the offsetting tax shield benefits. To help understand the implications for this I have also included additional sensitivity tables assuming a zero corporate tax liability.

Barrick (not Barack) and AngloGold Ashanti

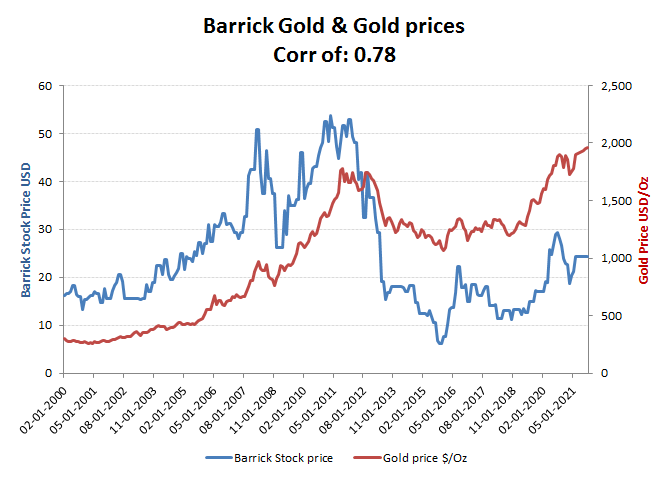

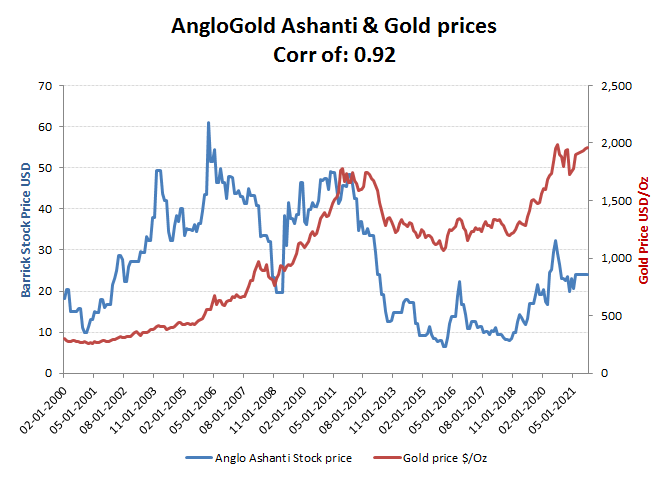

Before looking at the valuation tables, it might be also helpful to look at both Barrick and AngloGold stock price histories in context of the market price of their principal product, Gold.

The first observation one might have is that the stock prices for both Barrick and AngloGold have failed to recover to previous peaks, notwithstanding the Gold price recovering and to new record highs. Central bank money printing that is again responsible for the Gold price rally, has also increased equity market ratings and reduced market FCF and earnings yields, so clearly it is not a market rating issue.

Barrick Stock trailing Gold this rally

And so are AngloGold’s

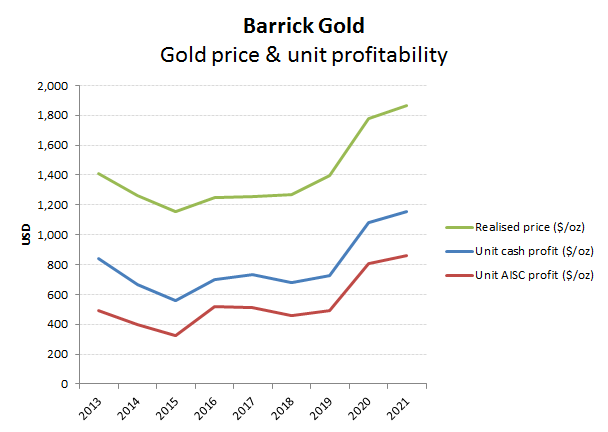

So perhaps it is a prospective earnings thing, that’s worrying investors?

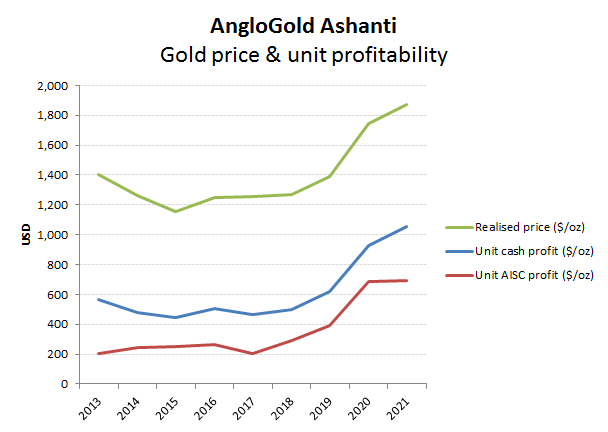

Well looking at the unit profitability on either a cash or an AISC basis, this isn’t the case as both metrics have also rallied with the Gold price, suggesting unit costs remain in check.

Barrick unit profitability rising with gold prices

As are AngloGold’s

So what’s up?

If it’s not the market, or the group’s ability to benefit from the rebound in gold prices this time, perhaps one should ruminate the other possibilities. While not a definitive list, here are some of my suggestions, in declining order.

- Something different this time such as special taxation or gold seizures such as Executive Order 6102 in 1933

- Comparative stock price rally last time (in 2011) over-egged either the profitability impact or expectations of further Fed QE and gold price rises.

- The Market’s behind the curve and just being slow to react

- The Market doesn’t believe the gold price will sustain current levels. Presumably this means it either buys into the Keynesian multiplier voodoo being chanted by the Democrats, or that they’re not going to be around long enough to print another $6 trillion of funny money.

Which of these is correct, hopefully will be resolved before the Autumn and possibly not entirely unconnected with the Maricopa audit. Whatever outcome you envisage for the gold price however, is your choice, but the below tables my help you quantify the potential impact on the stock prices of Barrick and AngloGold

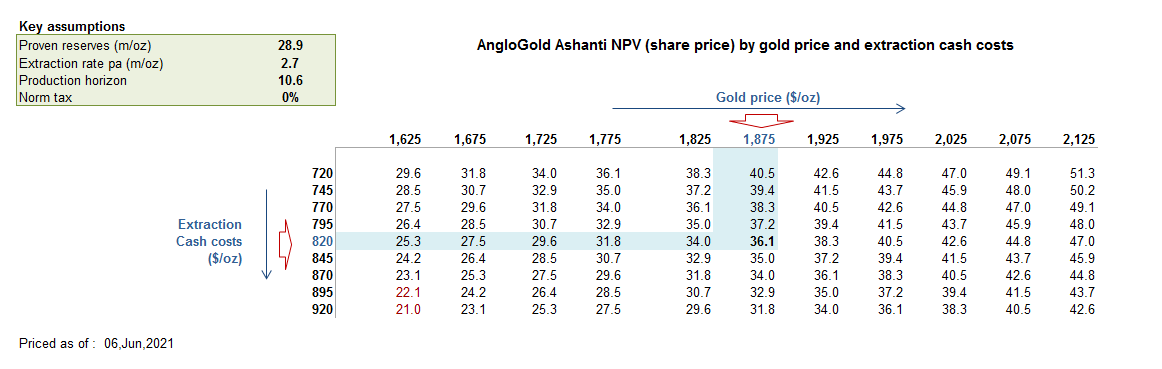

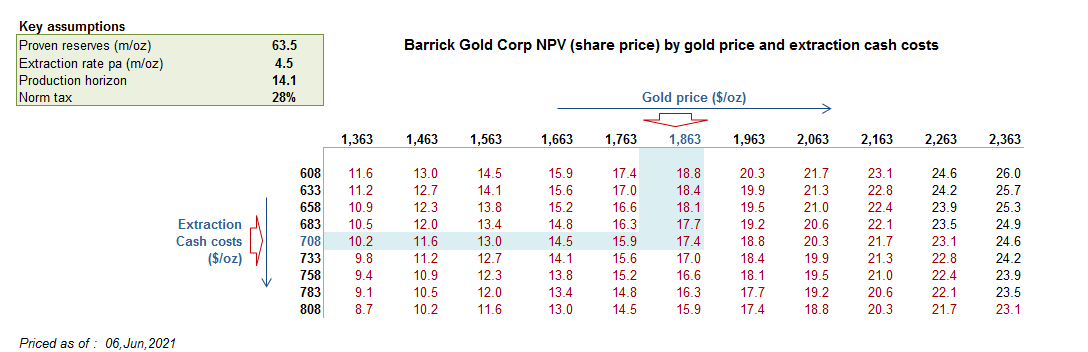

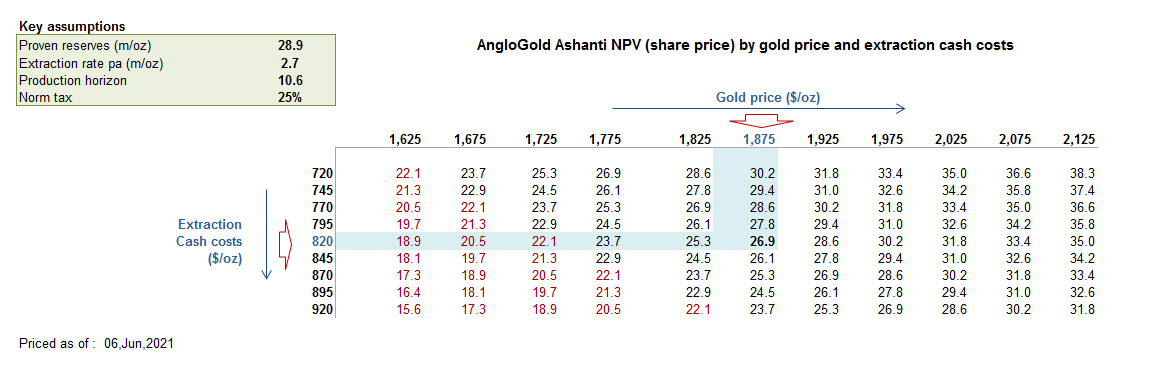

Full tax and existing capital structure basis

A point to note in reading these tables is that the prices displayed in a Red font denotes the valuation is standing at a discount to the current stock price (as of close Friday 4th June)

- Barrick: On a full tax basis, the stock would seem to need a Gold price about +20% higher than today (ie at approx $2,300/Oz) or that managements track record in finding gold justifies a comparable opportunity premium. A sub 10% CROIC however, suggest the later may prove difficult to support.

- AngloGold Ashanti: Perhaps investors would rather pay a premium for Barrick’s American weighted estate rather than be exposed to the political risk in South Africa, but on a pure reserves based valuation Anglo is by far the cheaper. Alternatively, it might just reflect a less reliable and ‘proven’ reserves estimate than for Barrick!

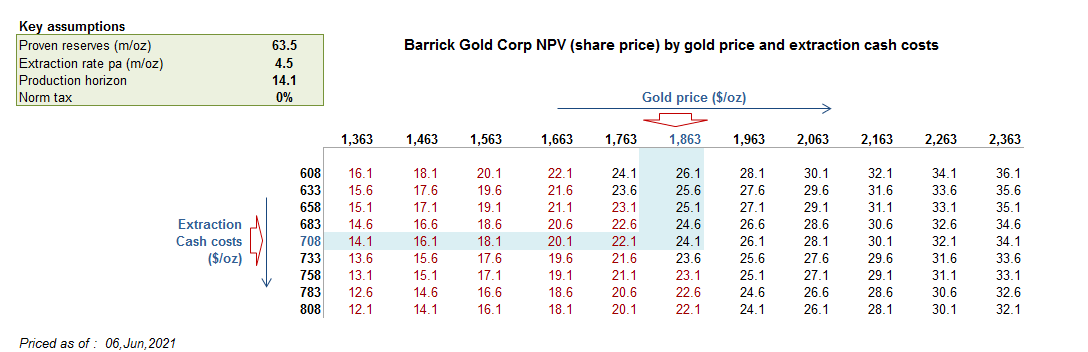

Zero tax (sheltered) basis

- Barrick: It may struggle to justify the current stock price from its reserves alone on the current capital and tax structure, but to the right corporate raider that could soon be resolved, particularly if a friendly central bank keen to enlarge its gold deposits was to hand to help with the financing.

- AngloGold Ashanti: The chances of AngloGold being able to run fast and loose with its corporate structure to avoid paying tax in South Africa is perhaps wishful thinking.