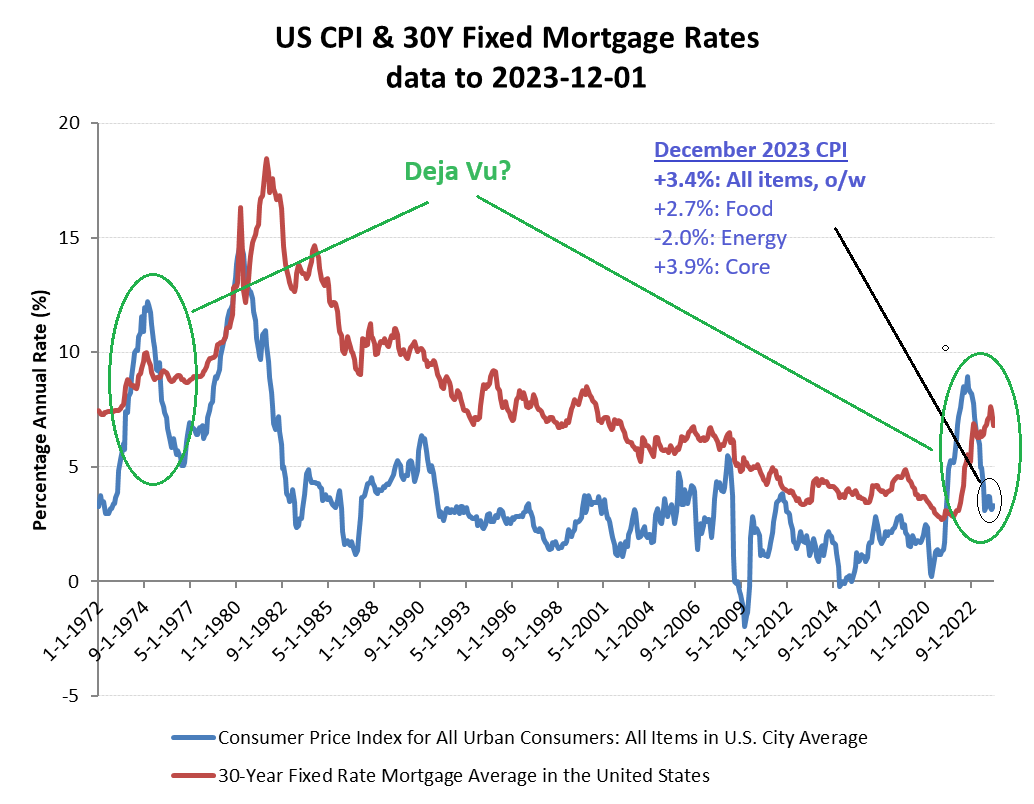

Deja Vu – but have the lessons been learned?

“Follow the Fed” has been a winning investment strategy, but that ought to be confined to what the central bank is actually doing rather than the narrative that it is trying to communicate. Since early December, that narrative has been plainly on offer, with Fed Chair Jerome Powell signalling a series of interest rate reductions for 2024 and with markets obediently taking the cue by bidding up both bonds and equities. With December core inflation remaining stubbornly high at +3.9% YoY however, the Fed’s room for manoeuvre is probably a lot more constrained than the bulls would hope. Memories of Arthur Burn’s premature easing and subsequent inflation and interest rate spiral and currency declines will limit the scope for debt monetisation, at least until a more credible fiscal policy can be introduced (ie after the November 2024 elections). With a tsunami of Treasury bond maturities in 2024 and the government running a deficit of around $1tn per quarter, that suggests rates will again rise as the US et al all compete for lenders, along with a possibly bleak initial outlook for consumption.

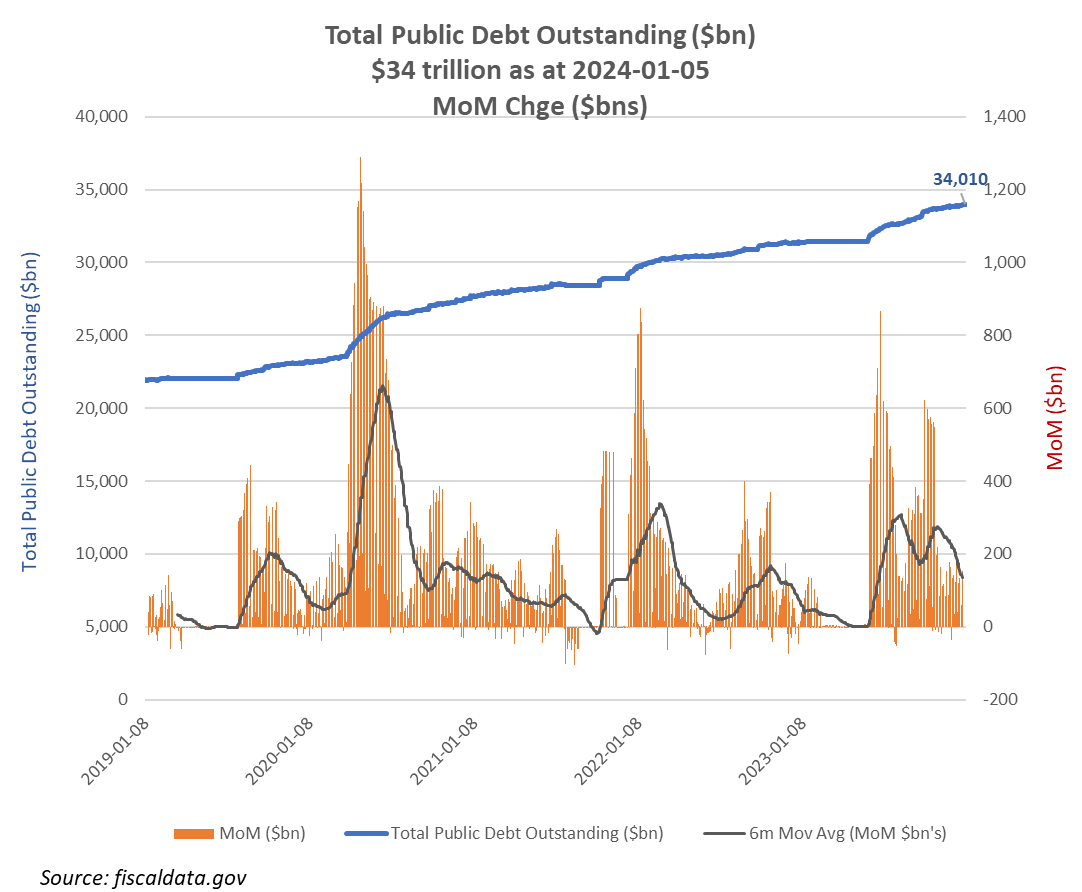

The US Fed can determine interest rates, but for only as long as it can sustain credibility and confidence in its fiat currency as a reliable store of value and as an efficient and stable medium of exchange. With public debt already topping $34 tn and rising by ~$1tn per quarter and around $8tn of bonds also maturing this year, investors will need convincing that currency won’t be sacrificed with more money printing, particularly when core CPI is is still running at almost double the +2% pa inflation target

Fed pivot, or just talking their book ahead of the Treasury maturity tsunami?

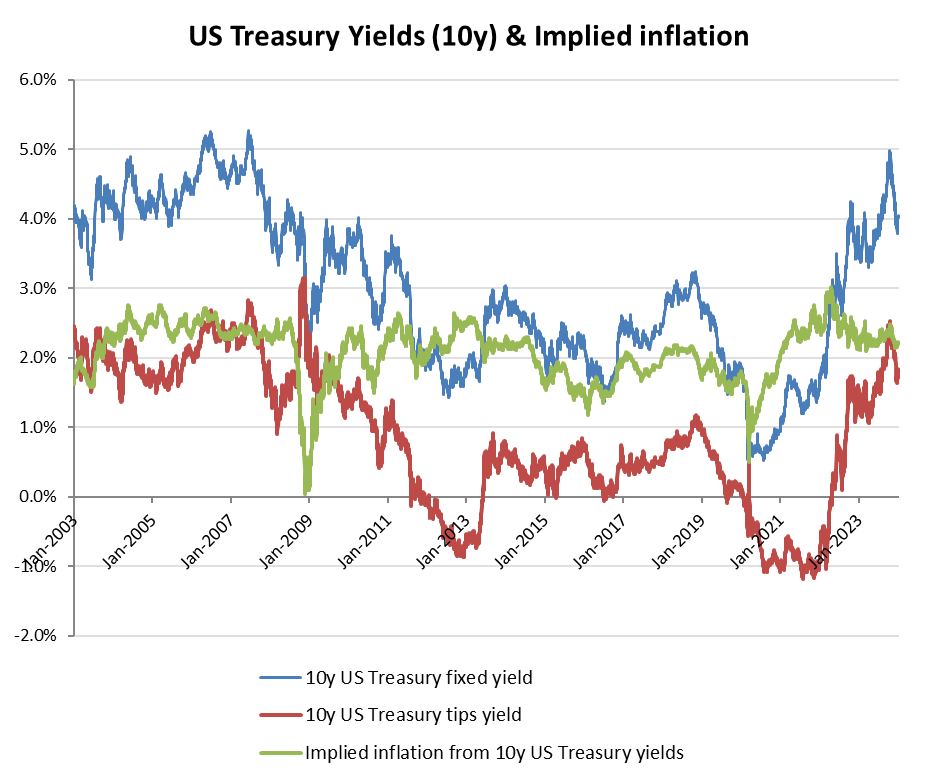

If the US Fed is unable to monetise its debt in order to avoid a currency crisis, then yields in bond markets will inevitably ‘normalise’. For US 10 year Treasuries, what that means is a return to a real yield of around 2% pa (see below), plus whatever the prevailing inflation expectation is. From the below chart, one can already see the effects of QT in normalising real yields back to around 2%, while the inflation being discounted has been ranging between 2-3%. Assuming an average inflation rate of around 2.5% pa over the 10 year Treasury yield cycle, then its wouldn’t be unreasonable for investors to demand a yield of at least 4.5% pa, and initially possibly higher until a new administration can introduce less reckless fiscal policies. A return to 10 year Treasury yields to well over 5% therefore quite possible!

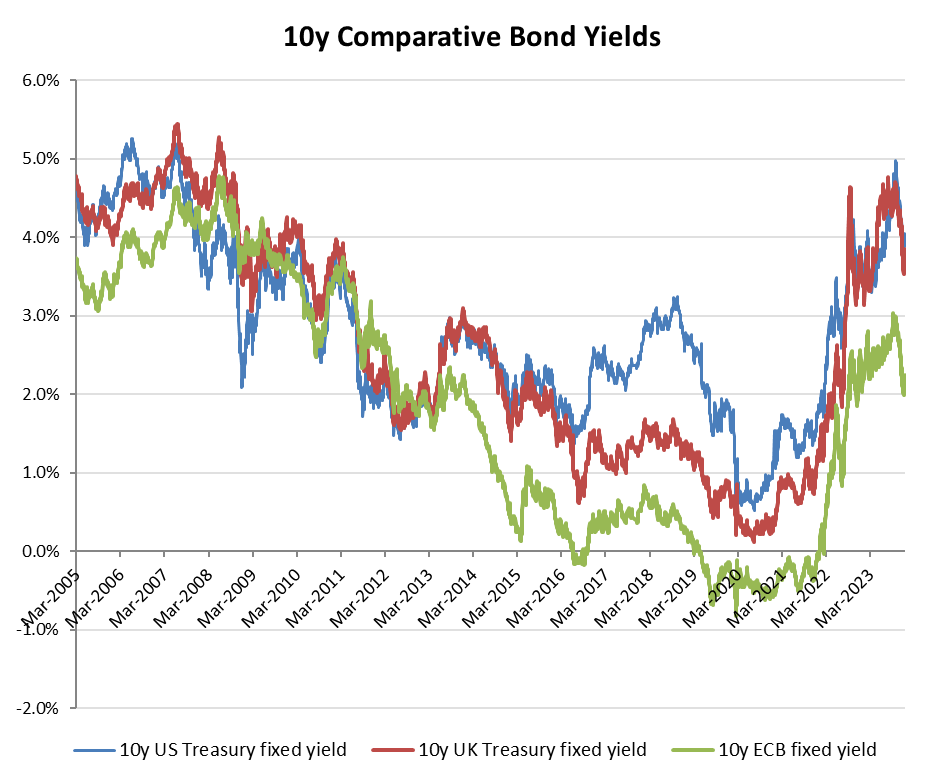

It’s not just the implied inflation being priced into Treasury yields, but also the normalisation of real yields back to around +2%

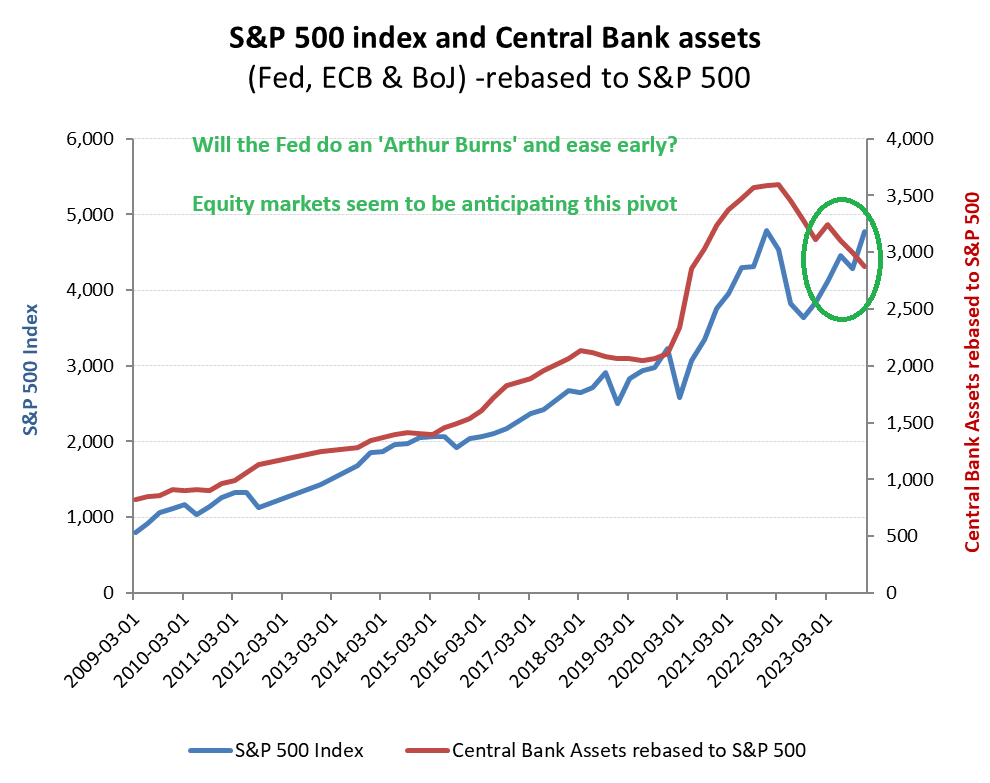

If inflation and the risk of currency collapse in face of uncontrolled deficits is going to limit a flip back to QE, then the current rebound in equity values may start to look somewhat exposed

Equities are anticipating a Fed pivot back to the money printer

This of course is not our first inflationary rodeo, even if few currently in financial markets have any direct experience of these events. As the December CPI result suggests, a generation of deficit spending funded by debt monetisation is not just headwind to ROIC, but also inflationary and will take time to purge and not without pain in terms of impact to future consumption. Where we are today, after the initial decline in energy related inflation, seems ominously similar to 1975 when the then Fed Chairman Arthur Burns prematurely took his foot off the brake with an early easing. The consequence, as can be seen in the below chart was the disastrous rebound in inflation, which necessitated the Volker rate increases and the return to the tighter fiscal policies of Reagan and Thatcher.

Remember the past, or risk repeating its mistakes

Unlike the 1970’s however, the stakes for the US are much higher. Much of its manufacturing industry has been hollowed out by offshoring, while the levels of public and private debt relative to incomes is considerably higher. What that means is that for as long as the spendthrift fiscal policies remain, rising funding costs on these higher financing liabilities could still pose a significant stagflation risk.

Add on the ~$1 trillion per quarter of deficits to the debt pile

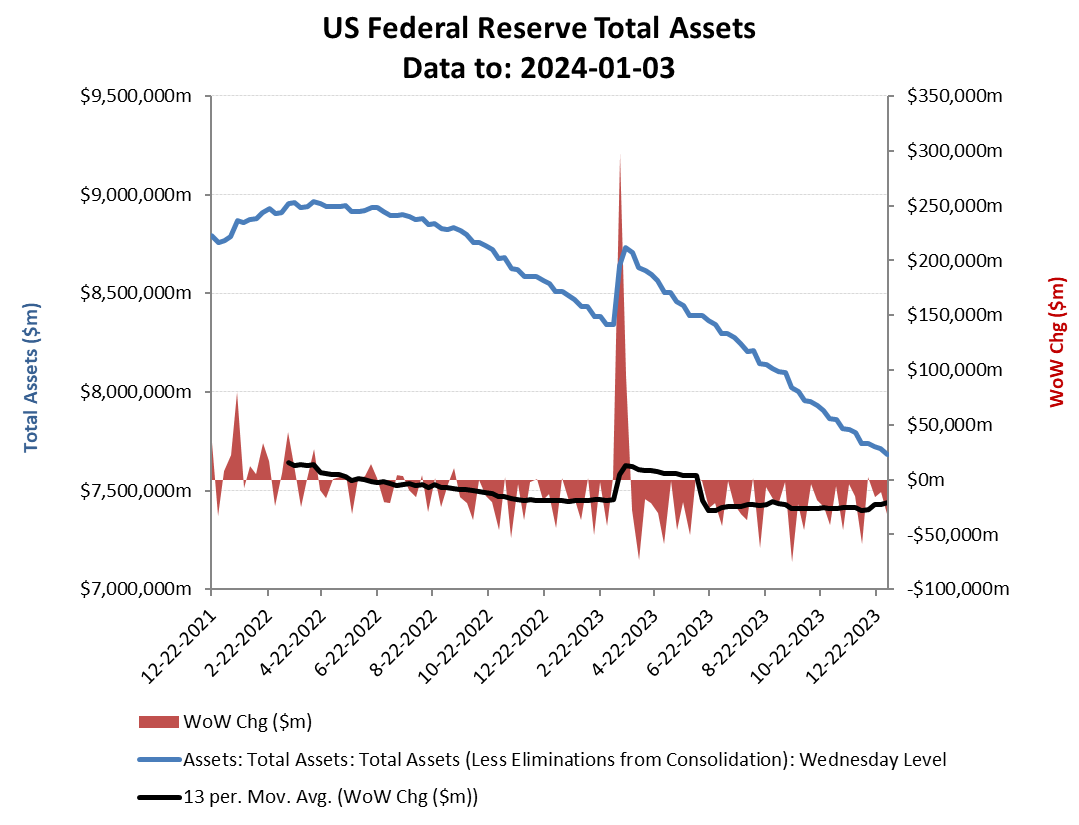

So what is the Fed doing? Notwithstanding the easing rhetoric, it is still adhering to its $95bn pm balance sheet reduction. While some banks are currently advising clients to expect the Fed to flip back to QE as soon as March this year, this is unlikely to offer much in the way of a panacea as debt monetisation into stubborn inflationary pressures on uncontrolled deficit spending is a well established recipe for a currency devaluation, which in turn just aggravates inflation and the interest rates one has to offer investors to continue lending you their cash. Sometime better known as Weimar, Zimbabwe or Venezuela!

The Fed may be talking soft to depress rates, but its actions on reducing its balance sheet remains in tightening mode

Inflation hedges

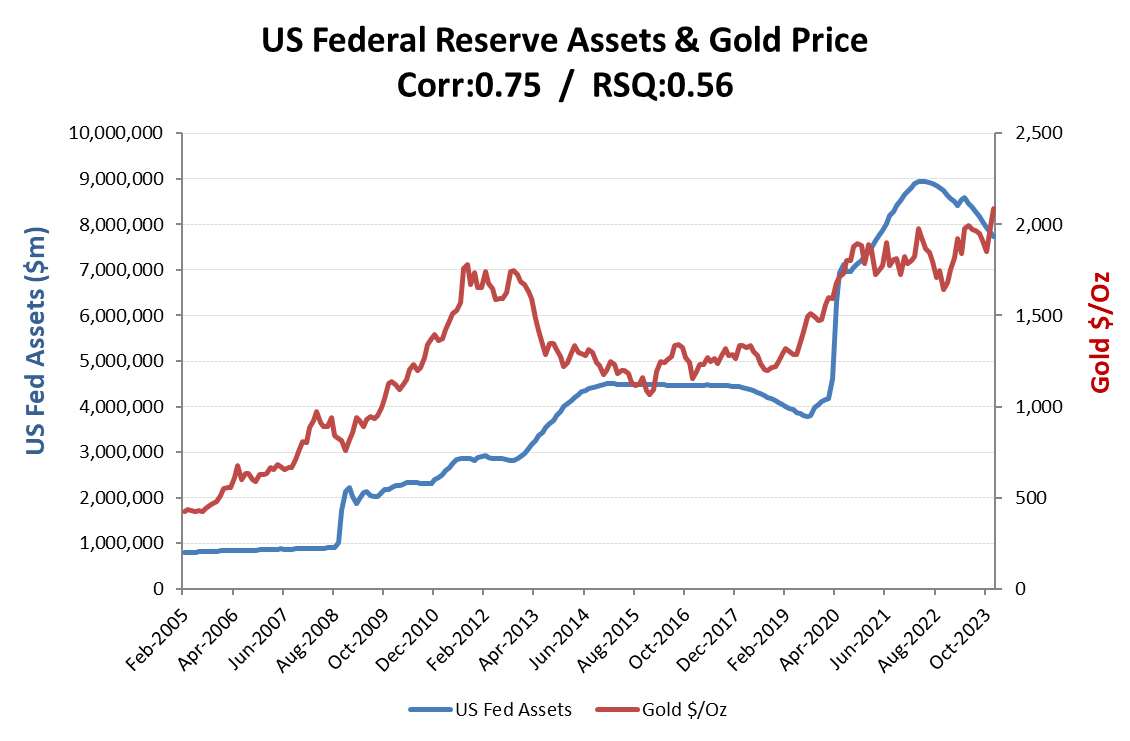

Ideally, an early return to fiscal sanity in 2025 together with reversals in onerous regulations to unlock the US’s traditional entrepreneurial strengths is the way forwards, although these would still remain on the other side of a still uncertain election season in November 2024. Apart from inflation adjusted bonds (TIPS), there are few safe havens in a ‘worst case scenario’, as the recessionary headwinds on consumption will impact corporate earnings and dividends. Precious metals offer an element of initial hedge, albeit without a yield in a market of rising yields, while the executive order 6102 in 1933 seizing private gold holdings offers an worrying precedent!

Gold rally reflects the inflationary hedge to the ‘pivot’ narrative, although somewhat lacking in conviction as the price retreats from its >$2,000/Oz highs

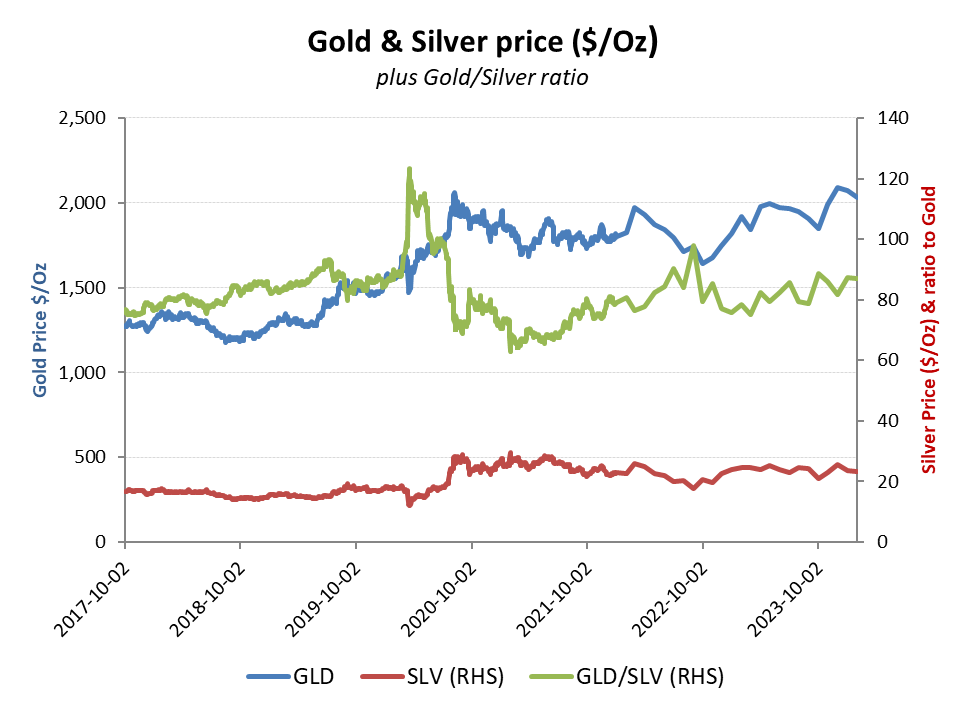

Gold running slightly ahead of Silver, albeit still broadly within its longer term pricing relationship