Sitzkreig

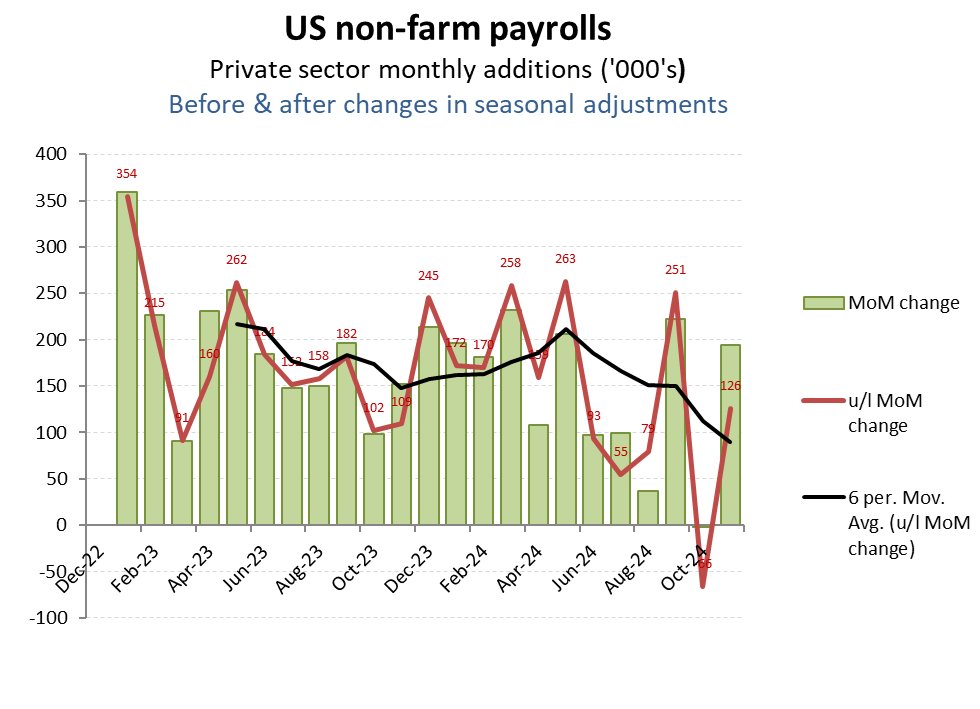

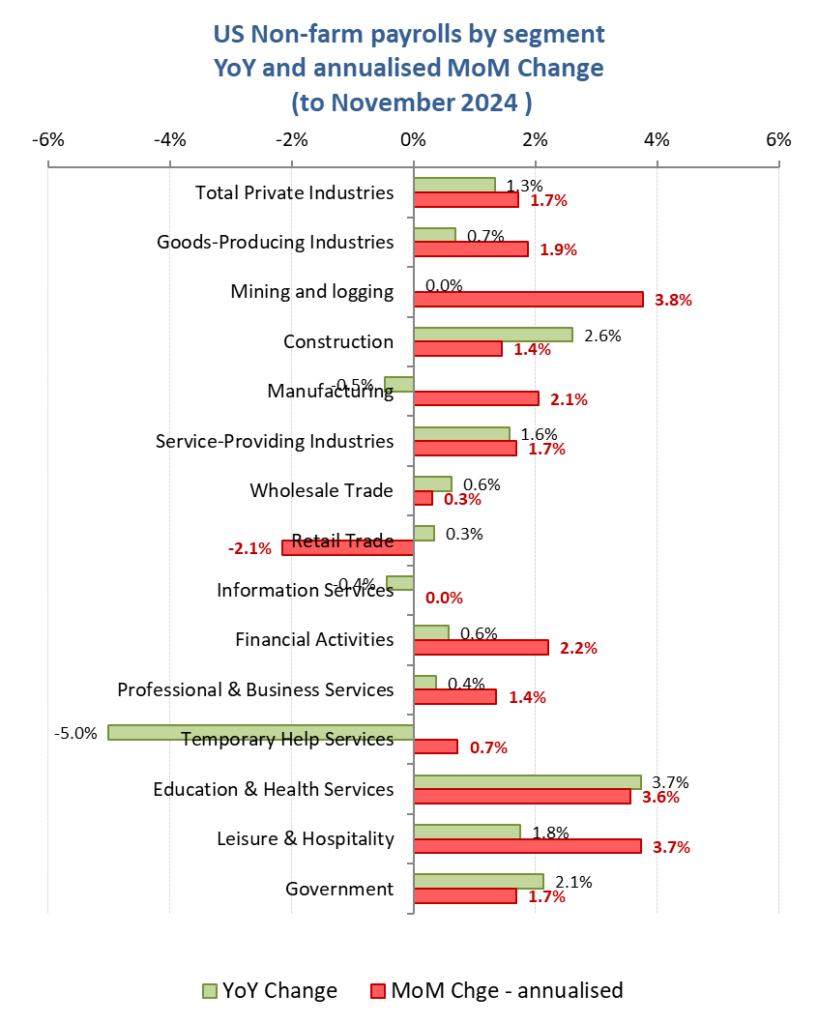

Today’s headlines may be celebrating the recovery in US jobs numbers in November (or at least the BIS’s ‘non-farm payroll’ guesstimate), but the reality may that we are just seeing the month-on-month distortions and knock-on effects of goosing the pre-election report for September which seem to have come out of the October figures. In that context, November therefore probably represents little more than a return to trend, with the current employment and economy still drawing on a crazy pre-election deficit stimulus equivalent of over 10% of GDP, but now ahead of the fiscal hangover once this is slashed under DOGE. While the continued strength in hospitality seems somewhat surprising, this may have more to do with the post hurricane recovery rather than any particular confidence in the structural prospects here (as flagging theme park attendances would seem to confirm). The softness in retail however, may offer an initial adjustment for what is expected to come down the line in terms of consumer discretionary expenditures.

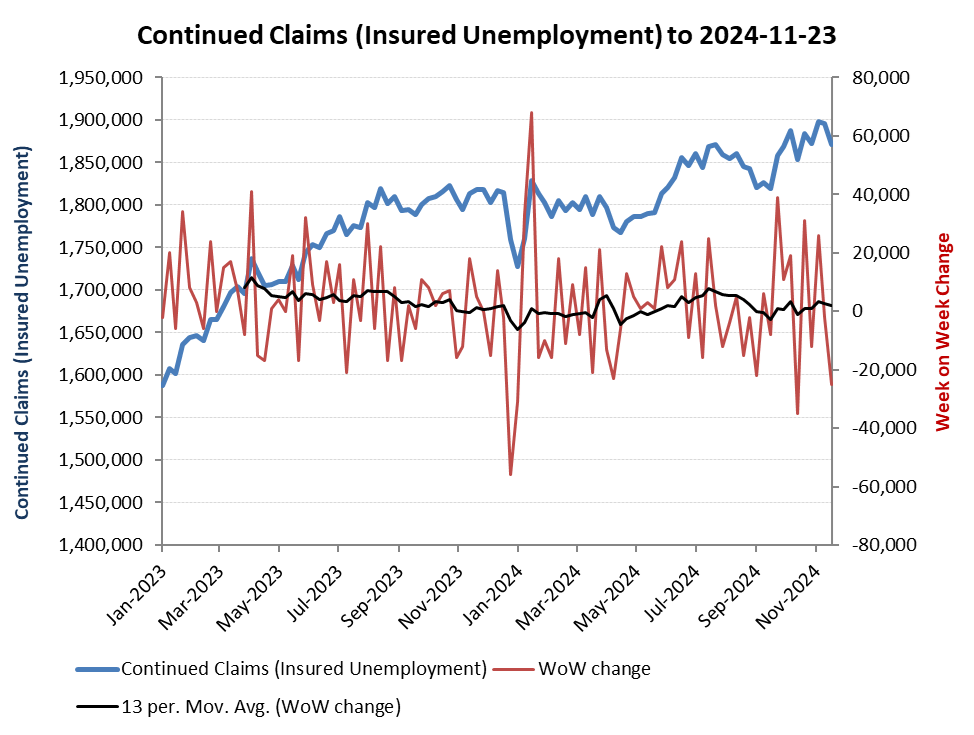

Given the pre-election environment, the individual monthly guesstimates need to be treated cautiously, with perhaps to look at the broader trends, while including alternative indices, such as the unemployment insurance weekly claims data. As with the BIS non-farm series, weekly unemployment claims are suggesting a softening employment market, but not precipitously, at least yet.

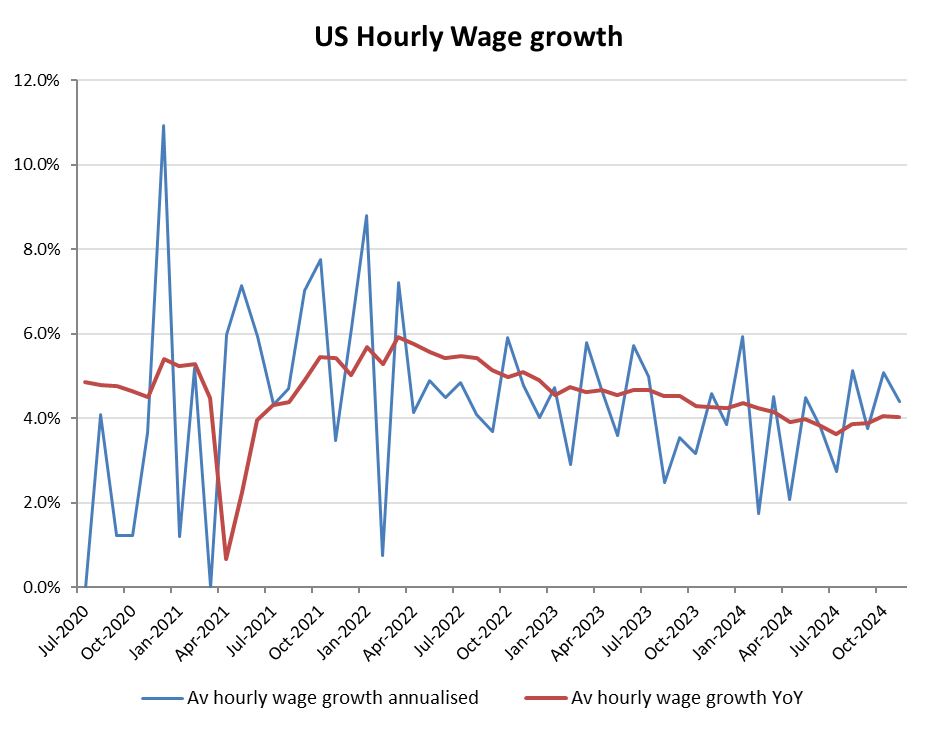

Average hourly wages seems to be firming slightly, now back up to just over +4% on a YoY basis and a bit more than that annualised. While representing an acceleration in ‘real’ wages against a falling statutory inflation figure, it also represents an lagged reflection of the previous infaltionary spike and therefore catchup, rather than some early evidence of an overheating wage market

Albeit with the caveat that these BIS numbers are guestimates and also reflect a limited timeframe, the respective employment data by industry category is of interest. That the government sensitive areas including Education/Health remain resilient ahead of and over the November elections ought not to have come as a surprise, while the improvement in Leisure/Hospitality may have incuding some post hurricane recovery along with the still substantial public funded accomodation support for the millions of univited ‘guests’. The noticable loser last month however, was retail, possibly reflecting the additional squeeze on discretionary disposable incomes and softening expenditures, particularly ahead of Christmas. A feature that seems to have also been reflected elsewhere, such as in the UK.

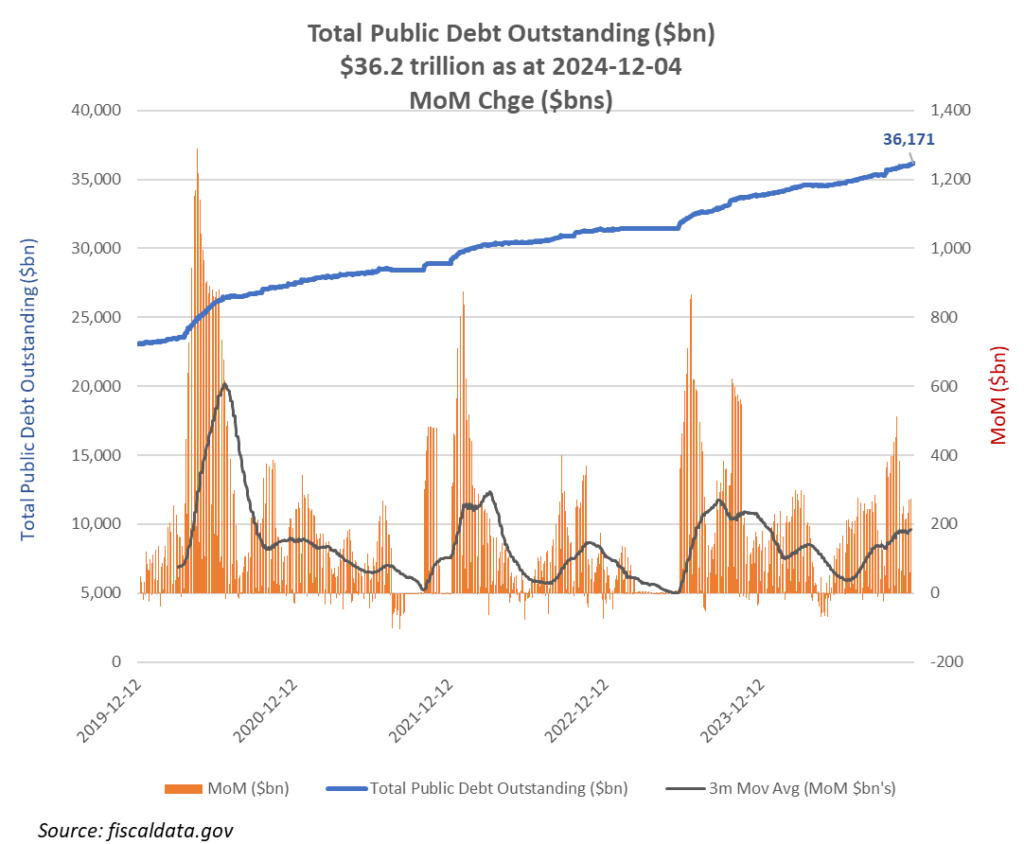

Behind any and all of these employment and economic data series is the looming debt crisis. Choose your analogy, elephant in the room, fiddling while rome burns, the quiet before the storm, or Sitzkrieg, that lull after the declaration of WW2, but ahead of the real hostilities. Whichever, all seems ominously appropriate as US public debt hits $36tn, with servicing costs now topping $1tn pa.

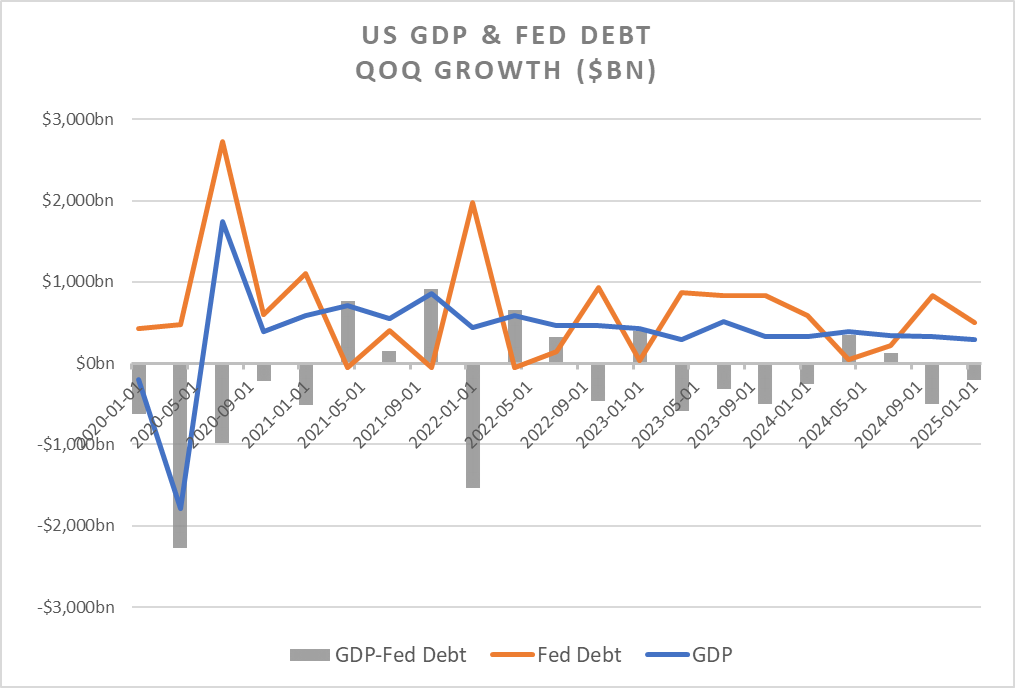

What many commentators choose to ignore is just how fake the current economic growth statistics are. Yes, the US economy has been growing by around +5% nominal, which equates to approx +$350bn per quarter. To achieve that however, has been a deficit and public debt expansion of over $800m, which therefore exceeded growth by almost $500bn! That’s taking two steps back to take one step forwards.