SVB failure – Moral Hazzard? Yellen Says No Bail Out

Will the US government again be bounced into bailouts following last week’s shock failure of Silicon Valley Bank (SVB) and subsequent seizure by the FDIC? The seemingly emphatic answer from ex US Fed chair and now US Treasury Secretary Janet Yellen is not. “We’re not going to do that again,” she is reported to have said with regards this possibility in an interview on CBS’ “Face the Nation”.

So for those fearing another slide into ‘Moral Hazard’, this will come as a relief, albeit these commitments are as reliable as the politicians that utter them! SVB however, is not just some mid-west agricultural lender, but an important facilitator for many of the tech startups that are central to the new ‘green’ eco-system that is being promoted, but perhaps even more importantly includes some very large political donors and supporters amongst the bank’s depositors. SVB, may not be bailed out by the US government, but I would not be surprised if some of the similarly politically inclined tech giants, conveniently flushed with cash and eager to mop-up future potential competitors, did not step in to acquire the business. Where there’s a ‘quid’, a ‘pro quo’ is usually not far behind, so don’t be surprised if many of the proposed regulatory investigations and potential restrictions recently being proposed on big tech mysteriously get lost in the weeds.

An apparently hard line on bailouts, even for a ‘progressive’ an operations as SVB, sends a firm message of resolve not to return to the money printing at the first instance. This was also the message from current US Fed Chairman Jerome Powell in his 7 March Congressional testimony, which helped puncture much of the recent enthusiasm for financial assets. As has already been apparent from the BIS and Dpt Labor statistics, Jerome Powell reminded Congress that

“Despite the slowdown in growth, the labor market remains extremely tight.”

So as not to leave them in any doubt meanwhile he went on to say

“As I mentioned, the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes. Restoring price stability will likely require that we maintain a restrictive stance of monetary policy for some time.”

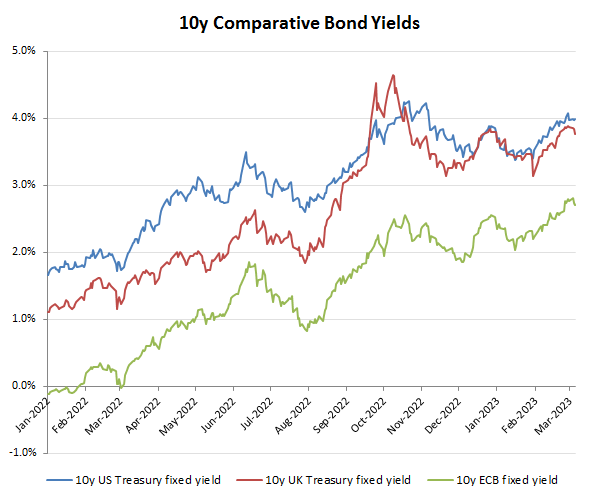

So will this SVB failure now moderate the Fed’s tightening stance, as some market commentators are suggesting (hoping)? We’ll see, but for the moment markets have been retreating from that position to anticipate Fed rates perhaps rising to 5.5%, or beyond, with earlier declines in 10 year Treasury yields now being reversed.

10Y Treasury Yields heading back to >4% again

Of course, talk is not only cheap, but a weapon of choice for central banks in order to manipulate markets. What is more relevant is therefore action and in this case, the extent to which the US Fed continues to adhere to is planned monetary tightening. So far, so good it seems from the evidence to date. While lumpy week by week and even monthly, on average the US Fed is still meeting its target to unwind its balance sheet asset position by approx -$95bn per month. As a reminder, that means the Fed is sucking over $1.1tn pa of liquidity out of bond markets and representing over double that amount compared to when it was inflating its balance sheet. That means a reduction in net demand from the US Fed alone of possibly $2-3tn at a time when all other leading central banks/Govts are being forced to do the same in the face of burgeoning deficits and therefore increased supply. Whatever the narrative on interest rates, the reality of supply and demand seems set to keep rates higher and for longer than those promoting an early easing and market bounce might suggest.

$93bn of re-purchases in February vs -$117bn in January