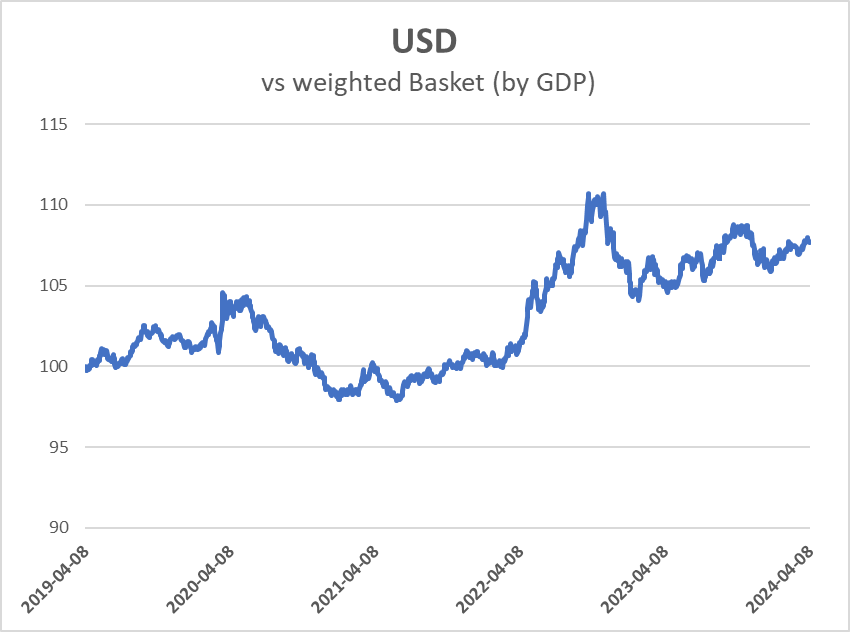

The mighty US dollar – ruling over the ashes

At times like this it is difficult to comprehend whether there are any adults left at the helm in the US. Jerome Powell’s attempts to ape his failed predecessor, Arthur Burns, is unraveling as fast as gold prices and bond yields are rising in the face of a so-called Republican Congress seemingly incapable of reining in the reckless deficits and soaring public debts within a sewer of blatant corruption and malfeasance. For those with some historical perspective, the signs of impending ‘end of empire’ have never been so apparent, although like ‘posh spice’, it may be important to be able to distinguish a relative state from an absolute one. Here I refer to the resilience of the relative value of the US dollar to its key trading partners (EU, CNY, JPY, INR, GBP,BRL), which with the US represent around three-quarters of Global GDP. Fomenting endless wars, plandemics and global chaos continues to drive frightened cash into the US dollar, even if the increased threat of WW3 seems to have elevated the attempted distractions to a somewhat extreme level now.

The key to US hegemony & strategy imperatives

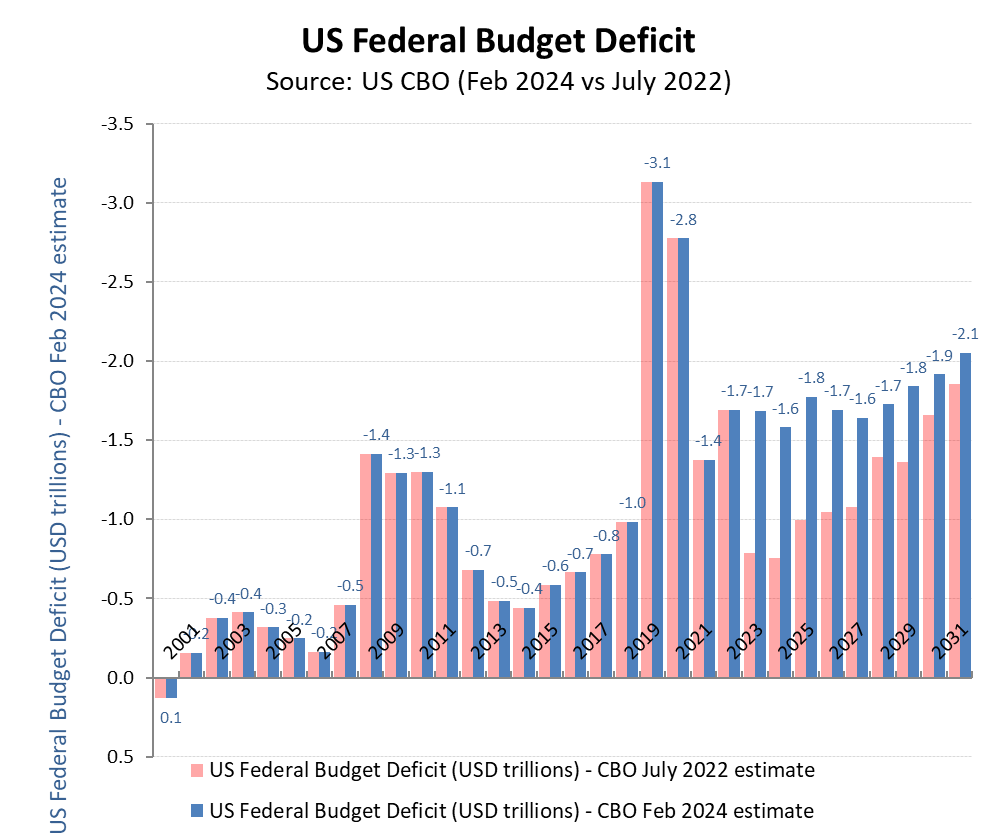

Attempting to talk down interest rates to encourage demand for this year’s tsunami of bond issuance was always going to be risky strategy for Jerome Powell, as current events now seem to be confirming. The parallels with Arthur Burns’ similar attempt have always be clear to markets, so a few disappointing core CPI releases together with a doubling in the estimated rate of federal budget deficits over only 18 months has been enough to spook markets into precious metals, notwithstanding bond yields heading back up. While GDP expectations and equity markets continue to take comfort from the short term benefit from these pre-election deficit expenditures, at some point markets will be forced to recognise the transitory nature of what is merely political window dressing of the reported statistics ahead of an election cycle. Once passed, tax-payers will be left with even higher servicing costs (estimated to over $1tn pa) on an even higher deficit over-hang which will only further increase interest rates as big government competes for debt and crowds out the private sector. At some point after the election, either the bloated state budget gets a Javier Milei style haircut, or the US will be heading further into a stagflationary spiral.

Gold soars as inflation/currency fears increase

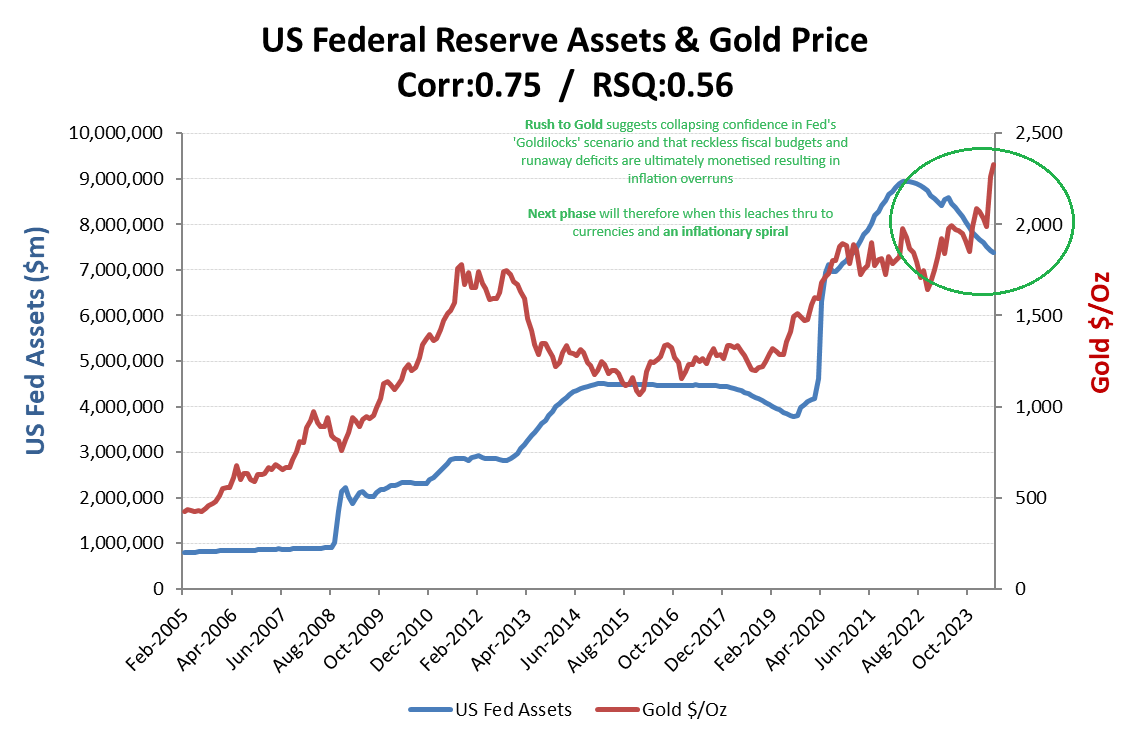

If the gold price is a bellwether for the credibility for Jerome Powell’s ‘easing pivot’ in Nov/Dec last year, then it is not a favorable one. While bond yields initially declined on post 5 year maturities, these are now back up again, while equity prices seem to have tried to hold on to their gains, albeit only with copious amounts of AI hype. For now, these have yet to permeate into currencies, as the war rhetoric is again turned up, although holders of cash are increasingly rushing into precious metals. This asset re-allocation suggests an expectation that Powell will persist in his easing pivot to serve his political masters (rather than his advertised mandate) and thereby risk a rising spiral of bond yields, deficits and inflation. Then again, the shock of seeing gold and yields spike together with a possible change of administration in 2025 may just be the necessary catalyst to awaken voters and legislators for the need to radical change in policies. Ergo, more sheep need to be scared into appreciating the hole they are in!

Soaring gold prices suggest investors believe Powell will persist with his easing pivot

Notwithstanding the reported better than expected GDP outruns (at approx +5.8% nominal & +1.9% real), this is no more than the increase in expected Federal budget deficit in just 2023, let alone 2024 or 2025!

Forecasting error hardly builds confidence

Reckless budgets stuffed with pork and the steepening trajectory in Federal debt comes as no surprise, although when the bill comes in, the squeals will no doubt remain.

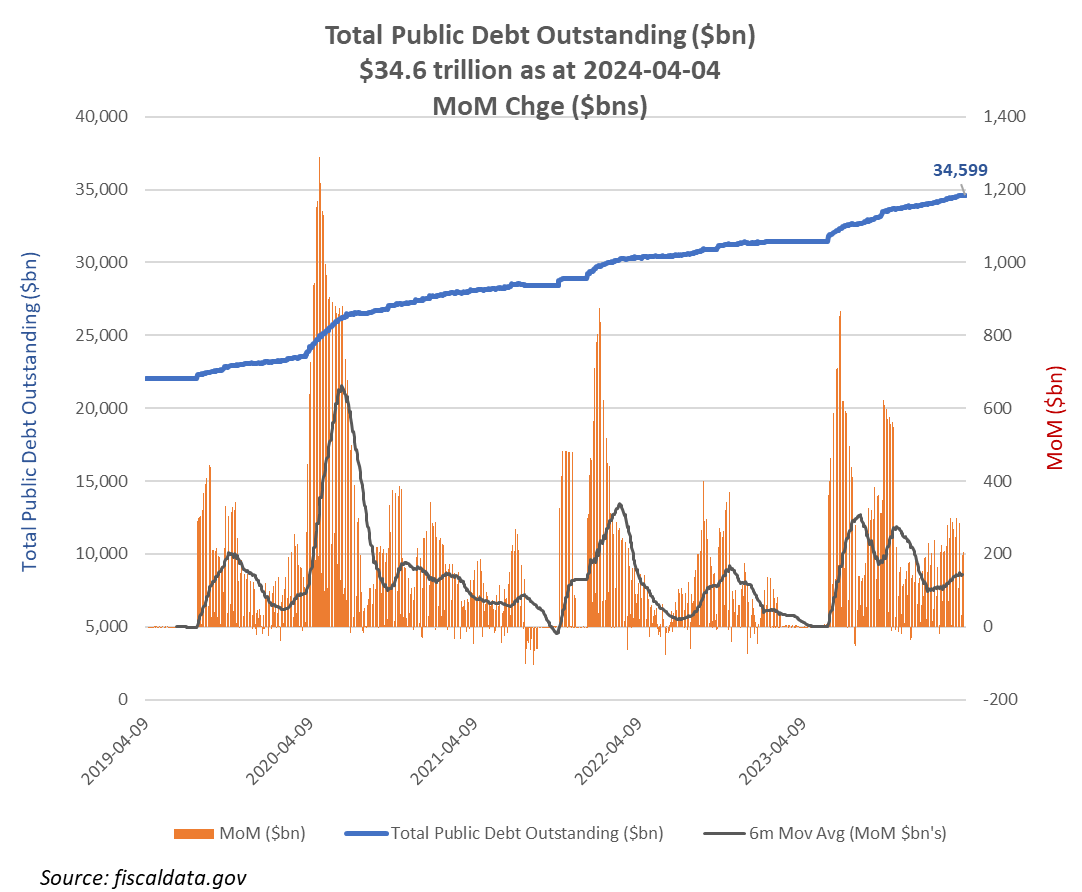

$1tn every 100 days!

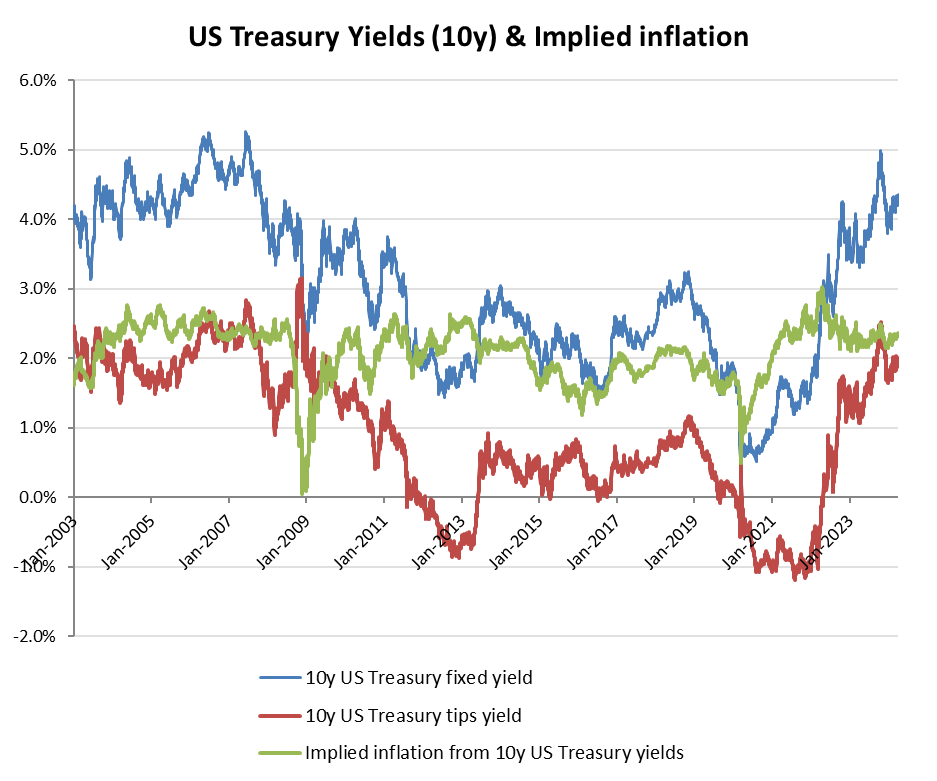

Jerome Powell’s easing pivot honeymoon doesn’t seem to have lasted long as much of the initial yield reductions at the medium maturity ranges have now been largely reversed. The return of 10 year real (TIPS) yields to 2% and an implied inflation rate of still under 2.5% when compared with the fixed yields however, suggests that the current movements are still no more than a broad normalisation in returns after the MMT manipulations following 2008. If markets lose hope for a significant reversal in current fiscal policy in 2025 however, then the current yields could well rise further and possibly significantly so.

Yields could yet rise a lot further

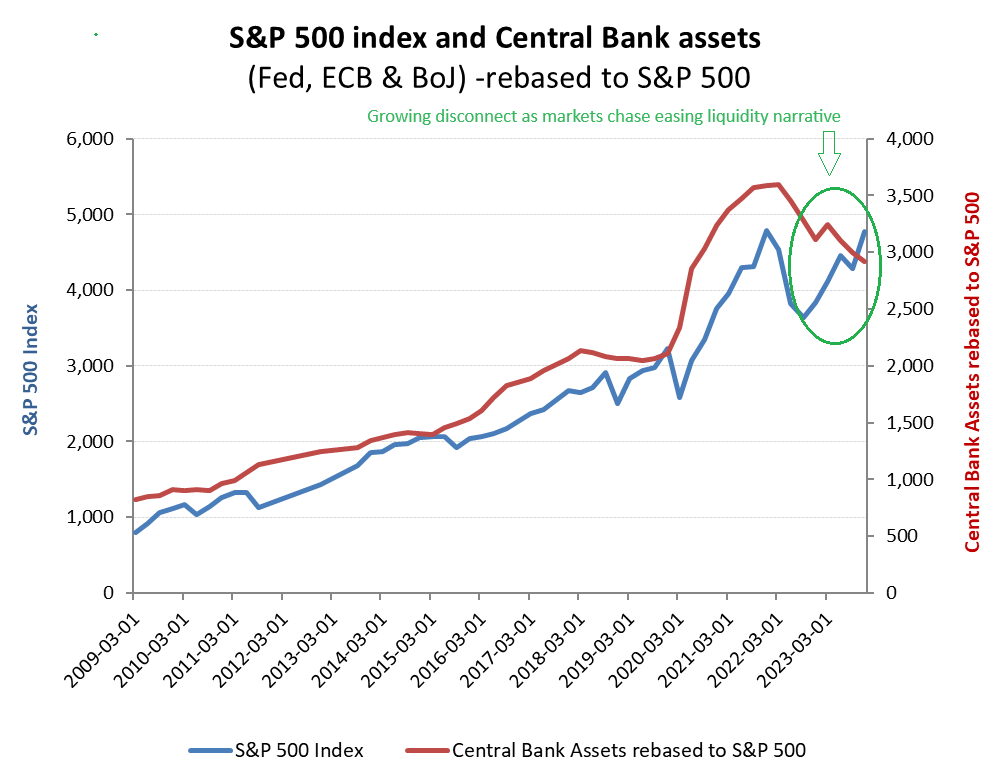

Equity markets have rushed to anticipate the return of the liquidity punch-bowl