Weak job growth? Just fiddle the seasonal adjustments!

How can the Fed contemplate cutting rates when US Q1 GDP growth allegedly came in at over +3% and June saw a +224k MoM rise in employment? Perhaps because it knows these headline numbers are garbage and that the true underlying numbers are considerably worse than these.

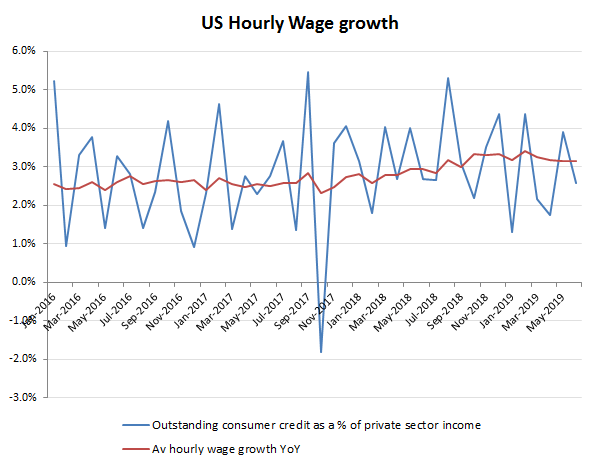

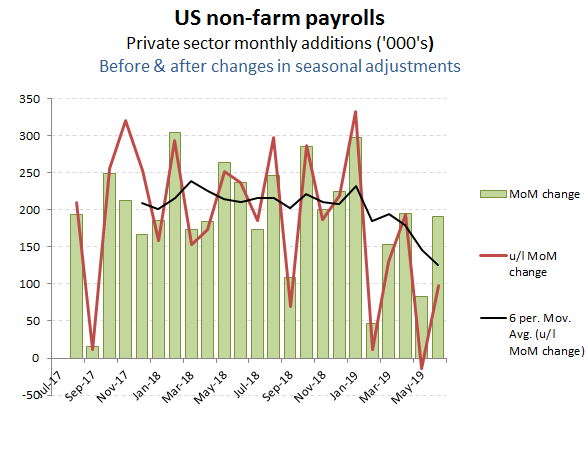

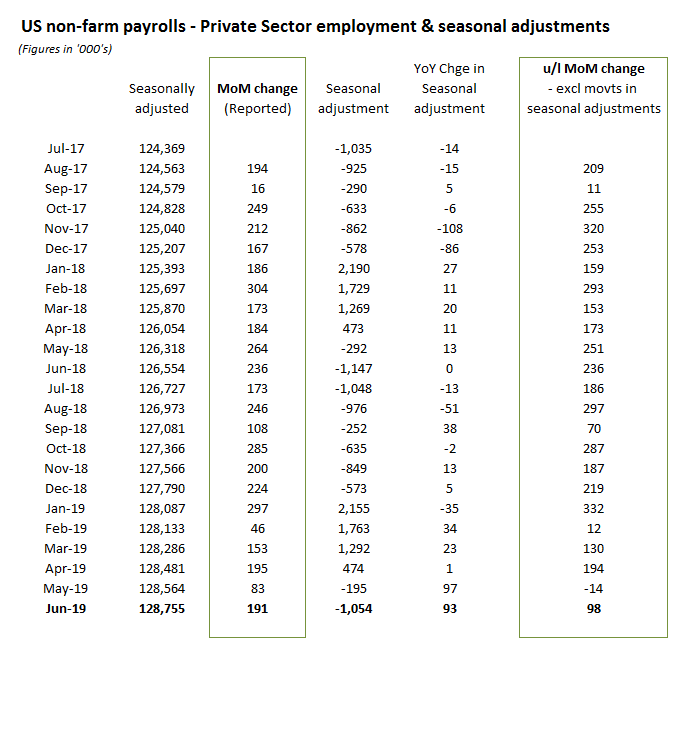

Having already commented on the fiddles used to turn a modest +1.9% rise in domestic consumption into a Q1 GDP rise of +3.2%, last month’s (June) non-farm payroll release, along with a restated prior month (May) provide yet more evidence of an apparently upbeat set of numbers having been substantially massaged. Whether one was looking at the overall MoM job growth of +224k in June after the +72k in May or just the private sectors +191k vs May’s +83k, the economy would seem to have substantially recovered from the May lull, something also supported by the +2.6% rise in annualised average wages; albeit drifting from the +3.1% actual YoY rise.

Strip out the favourable movements in seasonal adjustments however, and a very different picture emerges. For May, the +83k reported increase in private sector employment reverses to an actual decline of -14k if the 97k increase in seasonal adjustment is excluded. With a similar tailwind also applied for June of +93k, the BLS managed to transform a somewhat tepid +98k increase in underlying private sector jobs growth into a more impressive +191k. In essence, changes in the seasonal adjustments accounted for approximately 70% of the reported private sector job growth over the last two months.

Average hours worked may have edged lower, but at least average hourly wages remain solid, albeit even here the rate of annualised increase has eased back below +3%, at +2.6% for June. In themselves, the underlying level of private sector job formation and wage growth remain well above the levels that might be interpreted to suggest that we have entered a recession, although are also hardly suggestive of a robust recovery either.