Trump’s oil supply leverage

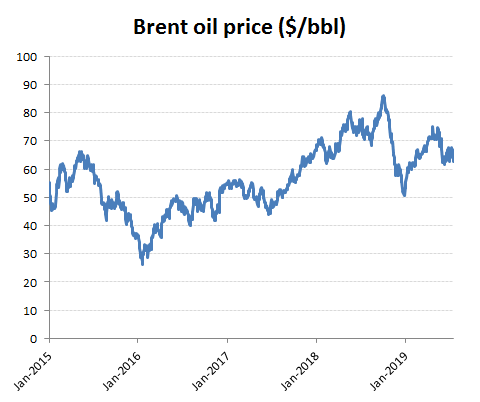

It says a lot for either the weak outlook for global GDP growth or the limited threat posed by the Iranians, that a series of attacks and seizures of oil tankers in the Straits of Hormuz, a conduit for around 20% of the world’s oil needs, as had no appreciable impact on crude oil prices. Indeed, the price is actually down over -5% on the week.

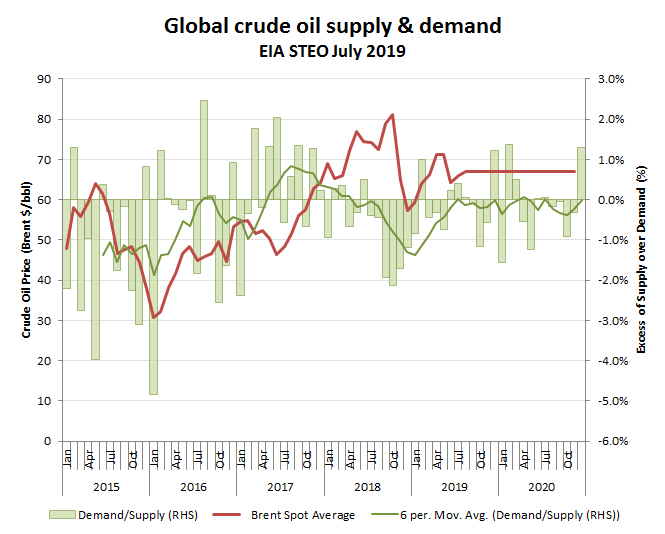

What is clear from the EIA’s last estimate of global crude oil supply and demand, is that the anticipated overhang of supply into the back-end of this year, which given the softening global GDP expectations, would presumably provide additional headwinds to oil prices. What is also evident however, is the very slim variance of supply to demand (often less than +/- 1ppts), that historically has resulted in some highly exaggerated price movements, both up and down. In this context one has to wonder therefore how markets can be so sanguine to the most recent threats to interdict the supply route for around 20% of this black stuff. Perhaps the focus of Iranian seizures to British connected tankers, while the toothless British government is distracted by its leadership contest, is seen by markets as a limiting feature, particularly given the current un-supportive attitude of the EU to both the UK and Iranian sanctions.

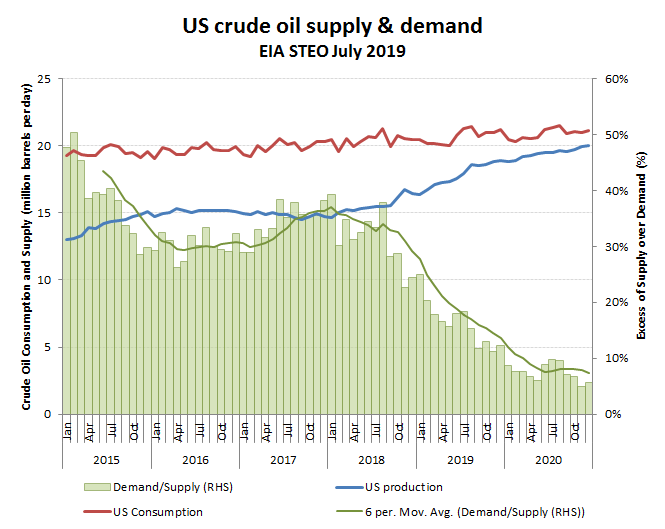

Against this however, is a US under Trump that would very much like to prise the UK out from under the control of the EU and has indicated a willingness to offer support. While claims of oil self-sufficiency by the US seem premature, its reliance on imports could drop to under 10% of consumption by the end of this year, which suggests it is largely immune to a cut in supplies from the Persian Gulf. Indeed, one might go as far as to suggest that any disruption via this route would offer some benefits, including a higher and more commercially viable oil price for domestic US frackers, More significant however, would be the pain exerted by the principal importer of this oil, China. The US might like nothing better than seeing a disrupted supply which could be blamed on China’s Iranian ally, while its own military assets in the region control whether to open or close this tap. By now, they ought to expect Trump’s asymetric warfare and that he’ll continue to stir the pot in the region to his own advantage, but will probably avoid getting sucked into putting “boots on the ground”, as the Iranian’s rash provocations would seem to be goading him to do. Perhaps Trump is learning a few tricks from Putin and Lavrov!