Oil shocker – producers claim to want lower prices!

Good grief, there’s a lot of tosh spouted on where oil prices are going after Russia and Saudi Arabia pulled the plug on the current rally, once Brent oil hit the magical $80/bbl target. The prize however, must go to Goldman’s straddle, where it seems the ‘technical’ analyst (someone who can draw straight lines) is suggesting a falling oil price, while their ‘fundamental’ view is that oil prices will strengthen. Presumably, they have a derivatives team who are betting the price will stay the same!

While it is easy to get sucked into the game of counting barrels of oil being produced and guessing how those get sold or added to inventories to justify some dubious forecast, one needs first to try and understand the motivations of those who are driving the market. At present, this has less to do with shifting demand, but more to do with supply, and here the swing producers of Saudi Arabia and Russia are calling the shots. With production from Venezuela down about 600k b/d (versus its -100k b/d quota) and new Iranian supply now also at risk, markets were clearly getting spooked that the original quota cuts in production of 2.7m b/d would be over-fulfilled. With the price heading up to $80/bbl, we first had Trump firing out complaining tweets (notwithstanding his Iranian policy was largely responsible), and then his client state agreeing to stabilise the price along with Russia by signalling increased production. In the tweet-sphere and online forums, this launched a storm of speculation that we would see prices now head back to $40/bbl, or at least the $60/bbl that even Putin’ appeared to be sanctioning – wrong.

Wrong, because the political environment now is very different from when the Saudi’s last crashed the oil price. Then, Saudi and the US were embroiled in Syrian regime change; in part to push back Iranian/Shiite influence and in part to attack Russian gas supply dominance in Europe by hoping to pipe gas from new Qatari gas fields as well as its squeeze Russia’s principal source of income. The Saudi’s got the added bonus of trying to crush the nascent US shale fracking industry (by taking the oil price to below fracking’s higher production costs) and thereby restore market share under the nose of the oilphobic Obama.

That strategy however, ended in unmitigated failure. Russia back-stopped Syria and was able to ride out the low oil price better than the Saudi’s, whose own budget deficits spiralled as its ‘war’ in Yemen put additional calls on expenditure. More importantly, Trump got elected as President and was more supportive to US energy self-sufficiency, which requires a higher oil price given shale’s higher breakeven point. With new LNG plants and shipping hubs coming on stream in the US, Qatar was therefore also becoming a competitor. Perhaps unsurprisingly, US tolerance of Qatari support for ‘freedom fighters’ in Syria waned rapidly and with the new leadership in Saudi, Trump was soon joining in the sword dance. Qatari’s were subsequently chastised and Saudi agreed a production cut with Russia which is why the oil price recovered from $30/bbl.

To understand the oil price therefore one needs to understand the motivations and ability to act of the principal participants. From the demand side, barring a trade war, this is probably going to continue to build gradually. Barring the extent to which they may try and buy sanctioned Iranian oil, the big players on the demand side of the equation, such as Europe and China are therefore relatively passive participants in this story. What will drive the agenda therefore are the principal suppliers, Saudi (as the principal swing producer of OPEC), the US (as now a major producer in its own right and almost self-sufficient and which also provides the military back-stop for the Saudi’s) and of course Russia. None of these has an incentive to see oil prices back below $60/bbl.

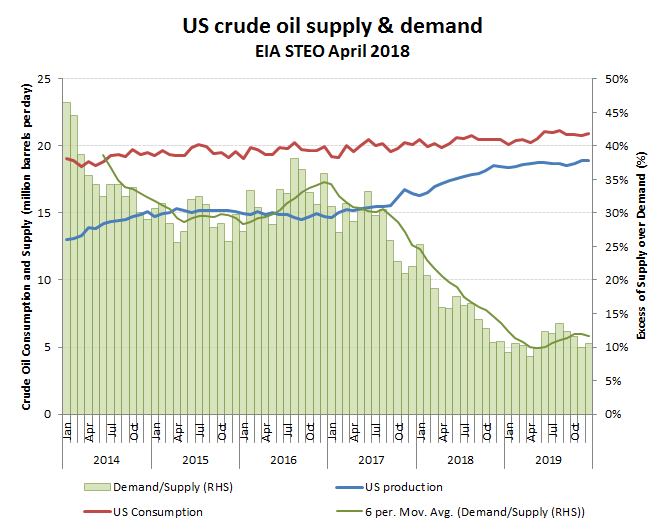

Of these three key players, the US might seem to have most to gain from low oil prices as a net consumer of hydrocarbon energy. This deficit however, is projected to decline from 35% last year, to only 10% next year; a function to a large extent of the rise in the oil price over $60/bbl, which has expanded the number of viable fracking fields. While this means a penalty to motorists in fuel costs, this increased activity and production has also stimulated employment in the associated industries (as noted in our non-farm payroll analysis) and trade balances. While new LNG liquefaction plants will open up export markets (such as trying to get Poland away from Qatari LNG) for excess US natural gas production, there should still be enough excess to keep US natural gas prices at a competitively low level to aid its basic chemical industries. Trump may not wish to see oil prices rise too aggressively, particularly ahead of the holiday season and all important mid-term elections, but as long as it doesn’t stifle consumption, raise inflation or be laid at his door, his tweets are mainly PR. A sudden price spike to over $80/bbl is politically uncomfortable for him this side of the mid-terms, but doesn’t mean he would like them below $60/bbl which would threaten shale investment.

US is still a net consumer of oil, but only just

Saudi Arabia will ultimately do as it’s told by the US as long as the monarchy wants to be protected by its defence umbrella and have support against its Shiite rival, Iran. The change of leadership following Trump’s election and subsequent policy volte-face on production, sword dances, US arms purchases and stomping on Qatar ought to make that fairly obvious. The recent actions to cool to oil price rise following Trump’s tweet complaints meanwhile plays well to his home audiences that he’s a president who gets things done. Saudi however, has a cash flow problem paying off its relatives and bombing its neighbours on a low oil price and notwithstanding the Crown Prince’s corruption ‘shake downs’, the price of oil is still trailing the budget break-even point. This was estimated by the IMF (Jihad Azour) to be $83/bbl for 2018, but to rise to around $85-87/bbl for 2018. The Saudi’s are also still planning to float Aramco in 2019. Their vested interests therefore are served by

- appearing to be customer friendly on price for Trump, but

- to edge the price to preferably above $90/bbl , while

- also keeping things steady so as to encourage future investors in Aramco to reduce the risk premium on oil, which would be difficult if it was bouncing around by +/-50% each year.

Russia under Putin and Lavrov, is a smart PR operator. There has been plenty of newsflow out of the place recently which might give the impression that they would be happy to see the price fall to below $60/bbl, which is what they want you to believe, rather than what is really in their interests. Putin himself is reported to consider $60/bb as a “balanced” price for oil, while Gazprom Neft is maintaining its long-term forecast of $50/bbl, with a range of $50-60/bbl as being ‘optimal’. Behind this bravado however, is an oil price reliant federal budget that needs a price nearer $75/bbl to be in balance. In November 2017, the Federal budget deficit for 2018 was estimated at approx $35.2bn/R2.0tn on expenditures of $295bn/R16.7tn and revenues of $260bn/R14.7tn, which I assume was based on a prevailing oil price (and EIA forecast) of around $60/bbl. Less than a year earlier (in Dec 2016), Putin indicated a Federal budget sensitivity to every $1/bbl movement in oil prices of +/-$2.86bn/R175bn. On that basis, he’d need an average price of over $72/bbl in 2018 to balance his budget, assuming no significant increase in either production (following the June 22-23 OPEC meeting) or pent up expenditures after a couple of very tight budget years.

So there you have it. A lot of jaw-boning, but those driving the oil price are more interested in removing price volatility and a potential early spike in prices; politically damaging for Trump and consumer confidence while destabilising future price expectations from the inevitable stimulus to new production investment. Make no mistake, the newsflow you have been reading, including possible increases in production are not a philanthropic gesture from Russia and Saudi Arabia aimed at getting less from their oil, but more. Not necessarily immediately, but certainly in the longer term. Both need a sustainable oil price of over $80/bbl, but need to edge this up progressively until consumers to come to terms with this. The message from Vienna on the 22-23 June will be of responsible producers increasing the taps to offset lost production from Iran and Venezuela and increased demand in order to restore “stability on a sustainable basis”. OPEC Sec General’s opine that the “oil price is not OPEC’s objective”, may for once be correct, but only in the very short term. Longer term, the tactics are there to reinforce a higher and more stable average price for producers and preferably at over $90/bbl. Something to keep in mind when forecasting the key inputs for the oil majors and evaluating their stock price potentials!