Donny 2 scoops and the fugazzi

Okay, maybe we get the plan, nurse the US economy and restore domestic manufacturing, while hopefully retaining control of Congress in the forthcominhg mid-terms, but then what, because what we have got so far is just a load of ‘fugazzi’ from a NY real estate developer? GDP is up a little, but less than the expansion in public debt needed to keep pumping it up and it is only the continued reserve currency status of the USD that has maintaned the fiction this is in any way sustainable. Perhaps Trump will retain control of both houses and in the twilight of his second term will finally exhibit some fiscal rectitude, although at this stage that’s one hell of a gamble for investors to base an asset allocation decision on. What does seem fairly clear however, is that Trump is prepared to gamble for high stakes, whether it be Venezuela, Iran, his Atlantic City Casino’s, or indeed his campaign for his second term. Combine this with his need for validation and somehow I still can’t accept that he will go quietly into the night as a lame-duck for the final two years of his presidency, which would be not much of a legacy. The groudwork seems to have been prepared for a mid-term win, which with the greater control and influence being exerted on his own Rino’s suggest something more radical may be in store for thise last two years.

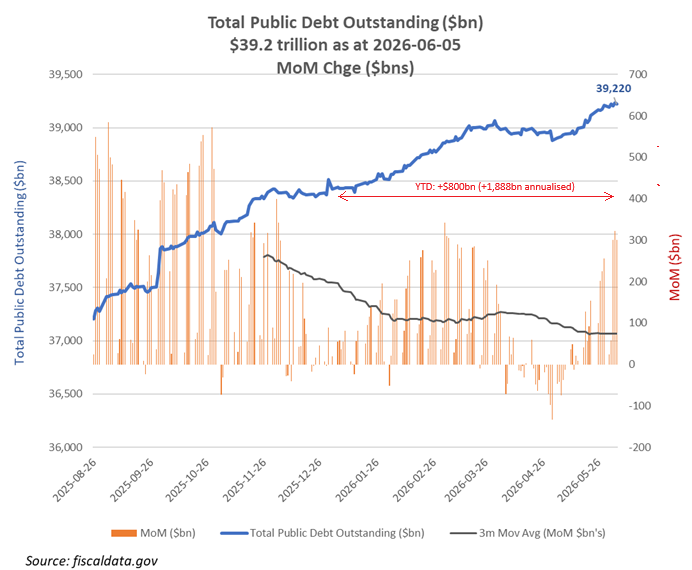

If market analysts are surprised at the resilience of the US economy into his second term, in face of higher tariffs, but easing regulatoryburdens and initially at least lower energy costs and inflation, it has in large part been due to a considerably more lax fiscal prolicy than originally advertised. In between the loud exhorations about waste and Elon’s DOGE, the reality has been the budget stretching ‘Big Beautiful Bill’ and a public debt figure that has been expanding by around +$2tn pa (+$800bn/+$1.88tn annualised YTD and +$3.0tn/$2.2tn annualised) since the 20 Jan 2025 inauguration. Against this, the last GDP print reported a nominal advance of +5.1%, or approx +$1.53tn annualised. That’s therefore around $500bn pa less than even the public debt expansion, while also excluding the approx +$120bn increase in annualised debt interest costs that are not included in the GDP estimate. Instead of a Keynesian ‘multiplier’ effect, that’s more like a ‘de-multiplier’, or perhaps a financial ‘discombobulator’. Not that markets are at all fooled by all of this, as evidenced by the falling USD, surging gold/silver prices and the the long bond yield still loitering around 5%. Has Trump capitulated to the big state, like all his predecessors? If so, then once the foreign adventures have ended, the USD is ultimately heading for a reckoning and his legacy will be one of missed opportunity. Is this the same Trump that battled a decade of Democrat lawfare, snatched Maduro, is denying Iran its sought-after nuclear weapons, controlling energy markets, while also containing China? If Trump is to leave a lasting legacy for his successor, then a focus on domestic fiscal probity to restore honest financing will be ahead of us, which looking at current market levels, may come as a shock for the complacent.

In the meantime, we get the same old made up government data on employment

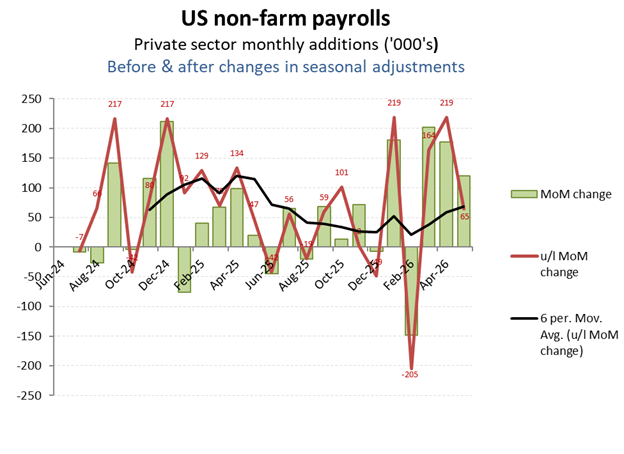

Last week’s May non-farm payrolls guestimates from the BIS meanwhile did little to alter the narrative. Underlying job formation (excl changes in seasonal adjustments) eased off to a modest +60k MoM net adds, albeit after the surprisingly robust estimates for the previous couple of months

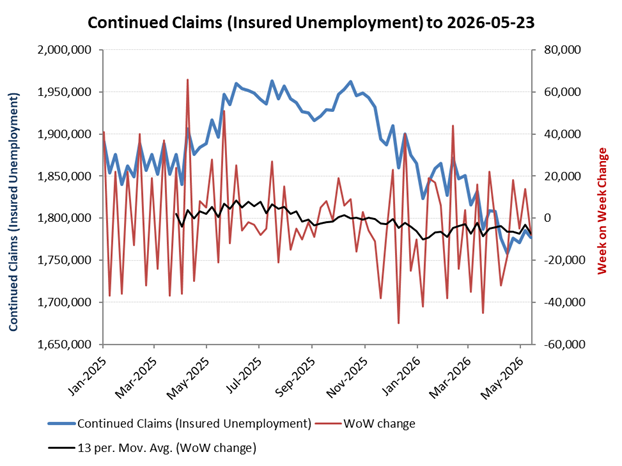

While job formation may be muted in the BIS guiestimates, the insured unemployment claims remain broadly unchanged, after the 2025 increases.

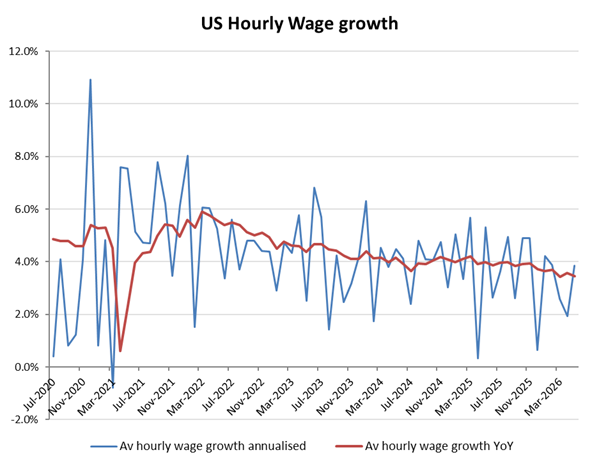

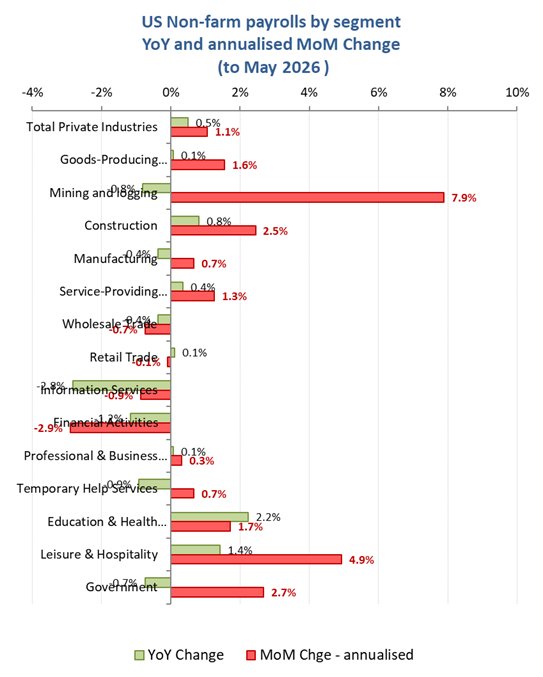

That muted, but still advancing narrative on job formation is also refected in average hourly wages, which continue to ease back after the inflationary spike in 2021, although this may also relect the changing mix in employment, with AI investment culling high value jobs in IT and finance and as can be seen from the chart on job formation by category.

High oil prices following the Iran attacks seem to have helped domestic extraction and with it the jobs, while the strength in Hospitality & Leisure remains consistent with the recent quarterly results from theme park operators. Information Services and Financial activities meanwhile continue to be substituted by AI investment

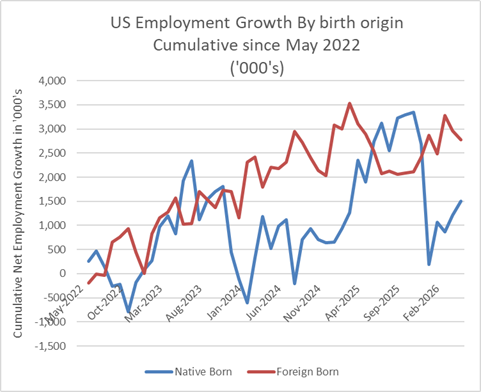

As most of the large Tech firms have work-arounds for the new $100k H-1B visa’s, these have so far done little to rebalnce new job formation to domestic applicants yet