More misdirection from US jobs data

Once again it is amusing to see the monthly US non-farm payroll statistics get used to provide cover for the usual misdirection by the US Fed/Govt. The approved message markets are meant to take from the BIS guesstimate of an improving trend in private sector net job additions in September (of almost +260k MoM), is that the economy is stronger than expected, which is to provide the justification and political cover for a higher and more prolonged period of interest rate increases. The real reason for this however, is a runaway deficit on top of a debt tsunami where rising inflation and the threat of a currency crisis means the cash shortfalls have to be funded from debt rather than money-printing. That this same dilemma is also being experienced by much of the rest of the World after the C19 scam and now Climate one, means a lot of borrowers chasing less cash as central banks are forced to tighten monetary policy. If the financial establishment are softening markets up for higher and more protracted interest rate increases, this has nothing to do with the BIS’s spurious monthly jobs guesstimates, but everything to do with the continued policy failures of spendthrift governments and their facilitating central banks.

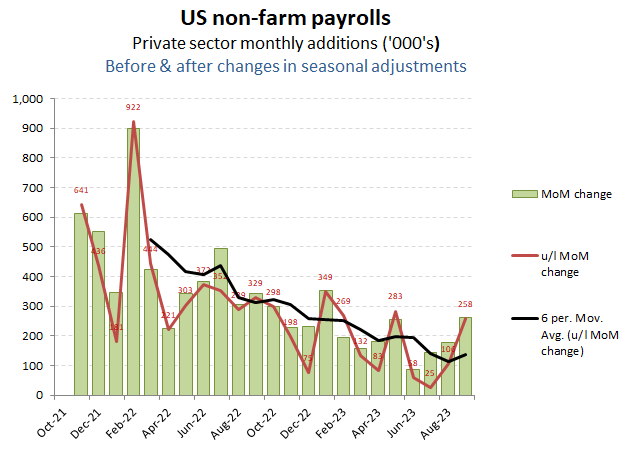

What markets are expected to react to

Read just the headlines and September US job growth seems remarkably robust. If the US is heading towards a recessionary cliff, employers seem blissfully unaware. It’s almost as if they are responding to the massive liquidity still being pumped into the economy ahead of next years crucial elections.

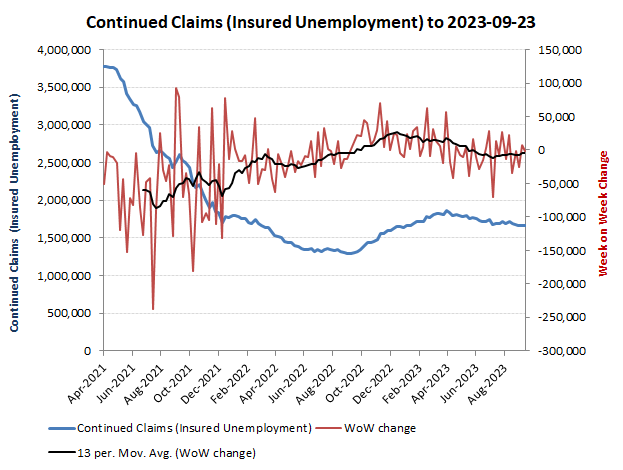

A solid employment environment apparently also reflected on in stable insured unemployment claims data

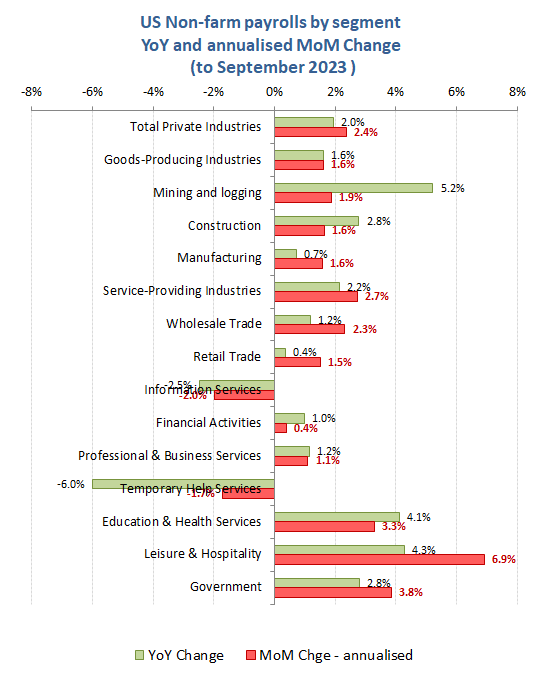

Even when drilling down to the various industry categories, there doesn’t appear to be too many obvious warning signals. Yes, Tech and Financial Services remain weak, and the weight on new jobs seem heavily focused on Govt and Leisure. The slippage in Temporary Help however, might offer a red flag, as this is where employment reversals start, as this category is the easiest and cheapest to fire and therefore often the first area to decline into recession.

A broad front of gains by category, albeit some cracks in Tech & Financial

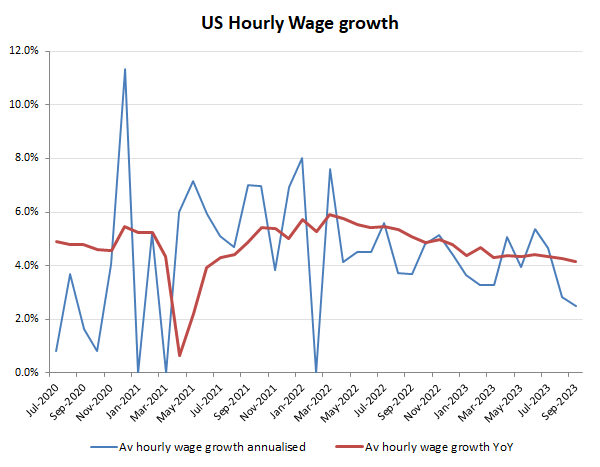

For a resurgent jobs market however, the average hourly wage growth is suspiciously weak and declining faster even than the temporary drop in official inflation statistics.

Average hourly wages however, suspiciously weak

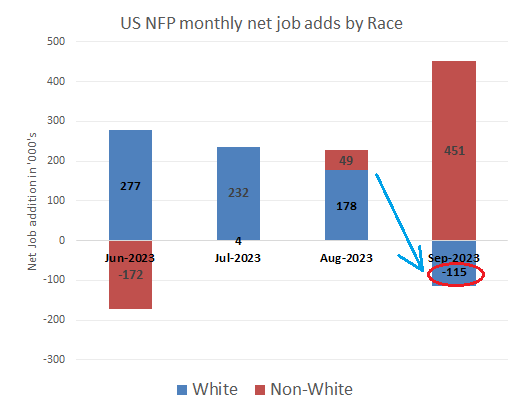

Well, what can one say? Low wages and an employment improvement only among non-whites while the administration’s open borders have seen millions of new potential low cost workers all competing for unskilled employment. Meanwhile, for whites, there was a net decline of around -115k jobs in September. Was this a result of unconstitutional diversity hiring policies by the many woke institutions and corporations (such as Oracle) which brazenly discriminate against some applicants on racial grounds, or just an opportunity to get some cheap labour while exploiting an opportunity for some virtue signalling? If white workers represent a higher proportion of workers with dual parent families and mortgaged properties, this doesn’t bode well for consumer expenditure as the threat of redundancy on incomes already whittled down by inflation and higher mortgage and car loans encourages this group to rebuild savings.

HaHa, welcome to diversity hires and open borders!

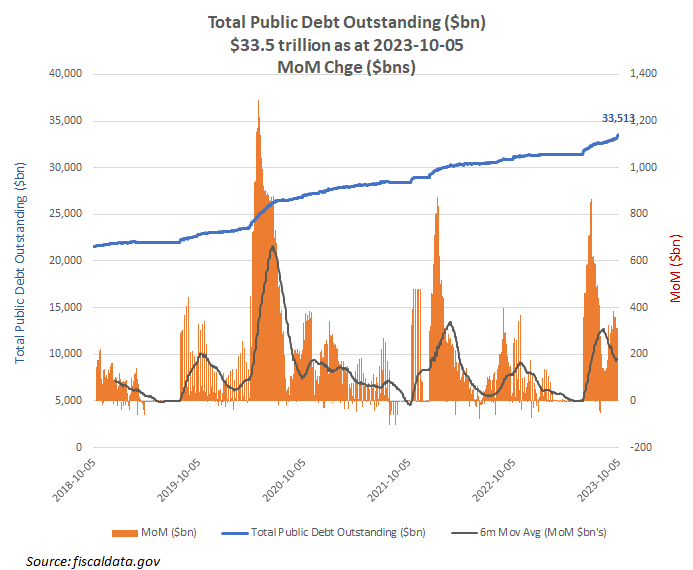

The below chart of US public debt is a terrifying precursor of what what lies ahead, with total debt increasing by over $600bn in the last month alone to now stand at over $33.5bn. As we already noted in a previous post that over $7.5tn (30%) of the previous debt is due to mature over the next 12 months and at the considerably higher prevailing rates and this on top of all the new liabilities. Having blown trillions on C19 and proposing yet more on climate agendas, governments seem to be betting on still being able to endlessly double down to forestall a solvency crisis with ever-more liquidity. This time however, they need to fund it with debt rather than the money printer and to avoid a currency crisis as inflation remains stubbornly high for all this largesse. What that means is a massive spike in competition for cash, which in turn means a demand imbalance and therefore the cost of money rises. If punters are being warned that rates will be higher and for longer, it has little to do with the monthly non-farm payrolls, which are merely useful camouflage for the authorities to manage expectations while helping to deflect blame from the real culprits!

Scared? You ought to be!

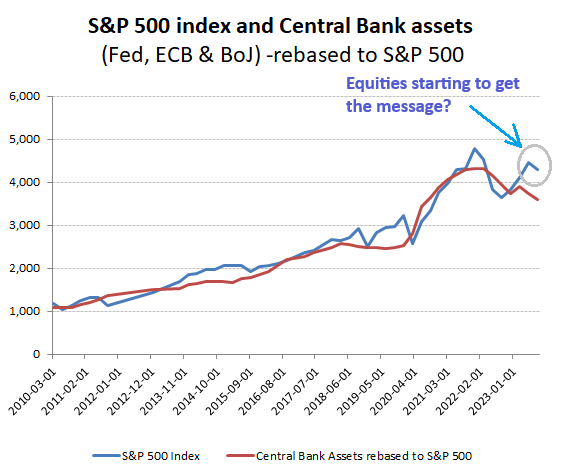

So it’s back to this old reality, where valuations are driven by liquidity. Much as financial markets will always want central banks to keep lubricating the industry with endless liquidity punch-bowls this is no longer possible as inflationary pressures come through. That means a monetary squeeze into a probable recession where higher rates will also substantially reduce the rate of corporate demand for equity, both their own (share-buybacks) or for others. Less cash chasing weaker returns is now on the horizon as in the war of monetary and earnings contraction with fiscal irresponsibility, the latter invariably is the casualty. It’s a shame that those still partying in the last chance fiscal saloon seem oblivious to this.

When liquidity drives asset demand and therefore valuations