US Q3 GDP bounce exaggerated by soyabeans and deflator

Q3 US GDP was “better than expected” at +2.9% and according to Capital Economics, “confirms that the economic recovery has regained some of the momentum lost with last year” and ..”As such leaves the Fed firmly on track to raise interest rates in December”

Well there you have it, the consensus view from economists!

Before you get too carried away by the narrative however, it might be useful to at least check out the original data from the bea

http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm

What you’ll find here is the usual small print and caveats, but also evidence to suggest the Q3 rebound may not be as good as being presented.

Firstly, when looking at the +150bps increase in GDP growth from +1.4% in Q2 to the +2.9% reported for Q3, how many of you will be aware that this was also after a -50bps reduction in the assumed inflation deflator from +2.1% in Q2 to +1.6% for Q3 and that the current price improvement in the rate of GDP growth was a less impressive +70bps, from +3.7% to +4.4% (+$201.1bn YoY to $18.651tn).

But hang on, this is still better, isn’t it?

Well perhaps not. Peel away some of the veneer and one finds that the additional growth in Q3 was supported by

- Increased inventory build,

- exports and

- a smaller decrease in state/local government spend.

So let’s look at some of these great pillars of growth, starting perhaps with state/local government expenditures.

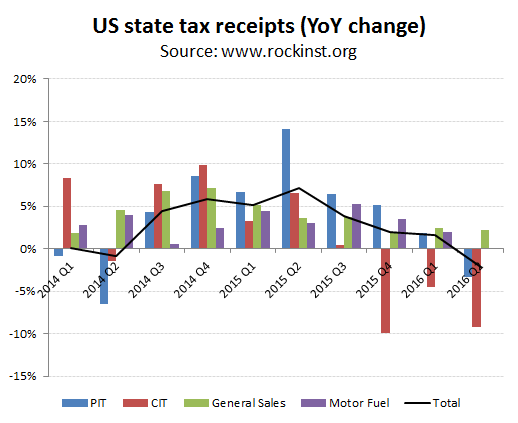

- State/Local expenditures may be perking up ahead of the elections, but what would you expect from politicians wanting re-election? What is clear however, is that this is not a result of buoyant revenues as we already highlighted last month, when we reported on data from the Oppenheimer Institute showing a -2.2% decline in State tax receipts

http://growthrater.com/us-state-tax-receipts-fall-2-2-hardly-prelude-fed-rate-increase/

Q2 2016 state tax receipts down -2.2%

- Exports: Zerohedge provided an interesting analysis of this which can be found here: http://www.zerohedge.com/news/2016-10-28/soybean-exports-were-responsible-one-third-q3-gdp-growth. The nub of the piece is an analysis by Standard Life that identified that the surge in exports reflected what seems to have been a one off phasing shift in soyabean exports in response to a weak harvest in LatAm. Out of a +$43bn increase in chained dollar goods exports, $38bn of this increase are believed to have been due to Soyabeans, or +0.9ppts of the +2.9% ‘real’ GDP growth in Q3. The analysis goes on to suggest that if Obamacare and the inventory build are also excluded, then the Q3 ‘real’ GDP growth would have fallen from the reported +2.9% to only +0.9%. Assuming one could apply the same deflator as for the overall GDP calculation, this would imply a nominal GDP growth dropping from +3.7% in Q2 to only +2.4% for Q3.

Soyabean export growth of +$38bn accounted for +0.9ppts to Q3 GDP growth

- Inventory build: should one exclude this? If it reflects a realistic expectation of future consumption, perhaps not. This however would not be compatible with what’s actually happening on the ground, as evidenced by falling consumer confidence (the University of Michegan confidence index fell more than expected to 87.2 in October, from 91.2 in September) as well as personal disposable income growth which fell from +4.1% YoY in Q2 to +3.6% in Q3. Without a follow-thru in consumption, the inventory build contribution in Q3 may just as easily be reversed in the reported Q4 GDP numbers, which conveniently will be beyond the ability to influence voting preferences!

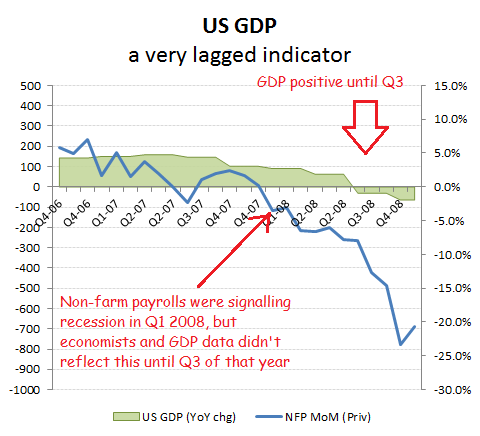

GDP figures are often pretty unreliable measures of economic performance, particularly the initial (guess-) estimates. Back in 2008, GDP remained positive right up to Q3, yet corporates were voting with their feet and sacking staff aggressively as they were looking at softening order-books rather than economist forecasts. From around February 2008, private sector job losses were clearly indicating recession, yet consensus forecasts and GDP data took almost 9 months to reflect this, with some vigorous adjustments in deflator assumptions being used to bump up export contributions for the Q2, which did little more than encourage passengers not to get in the life-rafts.

By the time you see it in the GDP data it’s often too late!