eBay added to the GrowthRater model portfolio (close price $24.49)

It is comforting to see the group firm up the lower end of its constant fx revenue growth range for both Q2 and the FY16 after a better than expect outrun for Q1. The group however is not out of the woods just yet as the platform rejuvenation still needs to be completed and the top-line performance has come at the expense of gross margins, which have only been recouped by aggressive share buybacks. The last time Devin Wenig presided over rejuvenating a tired tech doyen (Reuters), things didn’t go particularly to plan, necessitating several restructurings. Hopefully things will go a little more smoothly at eBay, although with Amazon providing a formidable competitive challenge, markets may wish to discount the good news as it emerges and a bit at a time. For now however, with constant fx revenue growth expectations stabilising back up towards +5% again, the near 8% prospective Op FCF yield is starting to look compelling, with an implied growth discount (GrowthRating) of under +2.5% CAGR beginning to significantly lag the trading delivery.

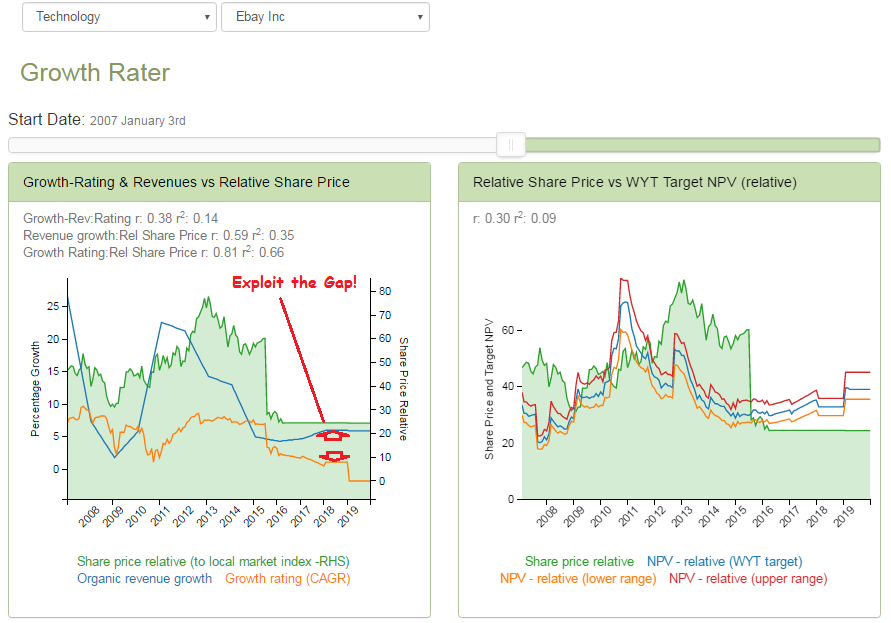

Valuation opportunity as revenue risk recedes

Last trading update – Q1 FY16: The feared revenue trough has yet to materialise, with ‘organic’ revenue growth at +6% in Q1 (vs guidance of +3-5%), albeit with increased PayPal processing costs and product investment reducing gross margins by -230bps and holding gross profit growth to only +0.3% YoY (approx. +2% at =fx). This largely dropped down through to operating margins (-220bps to 33.4% for Co adjusted excl stock-comp and -155bps to 28.7% on a headline basis including stock comp) and with EBITA slightly lower at $714m for Co adj (-2.7%/-$20m vs $734m) and -0.8%/-$5m to $625m headline. After a reversal in net interest for +$10m to -$20m and a broadly level tax rate of 20.4% (vs 20.2%), the adjusted net income on continuing activities declined by -7.3%, albeit substantially mitigated by a -4.8% reduction in average shares in issue (a further $1.0bn spent on buy-backs in Q1) to leave the Co Adj EPS figure down by -1% from $0.48 to $0.47 and ahead of the guidance range of $0.43-$0.45 ps. KPI’s for Q1 included:

• Active buyers: +4%/+8m YoY and flat QoQ to 162m

• GMV: edging ahead to a YoY increase of +1% to $20.45bn (+1.0% to $19.6bn for Marketplace and +29% to $0.9bn for StubHub).

• Revenue growth at =fx: +6% including +3% for transactions to $1.7bn (incl take rate of 8.2% vs 8.3%) and +19% for Mktg Services to $0.5bn

• Gross profit: +0.3%/+$5m to $1.66bn, with gross margins declining by -230bps from 80.0% to 77.7%

OUTLOOK: For Q2, the group is guiding for what seems to be a broadly similar performance as seen for Q1, with constant fx revenue growth in a range of +4-6% (to $2.14-$2.19bn), but with adj EPS again lagging at $0.40-$0.42 (-5% to unchanged YoY). Including stock compensation of -$100m, GAAP EPS is forecast to be in a range of $0.32-$0.34 per share. For the FY16, the group is raising the lower end of its guidance range on constant fx revenue growth from +2-5% to +3-5% and revenue range from $8.5-$8.8bn to $8.6bn-$8.8bn. While not re-stating it, we assume that the other elements of its previous guidance remains intact. This includes an adjusted EBITA margin guidance range of 31-33% (vs FY15 at 33.5%). Including tax at 19.5-20.5% and assuming further share buybacks (our forecasts assume -$3bn), the group is guiding for adjusted EPS of $1.83-1.87, with an expected GAAP EPS range of $1.55-1.87.

Note: Our adjusted EPS estimates include stock compensation expenses, whereas this company excludes these for its ‘adjusted’ numbers.