Facebook shareholders finally get the message

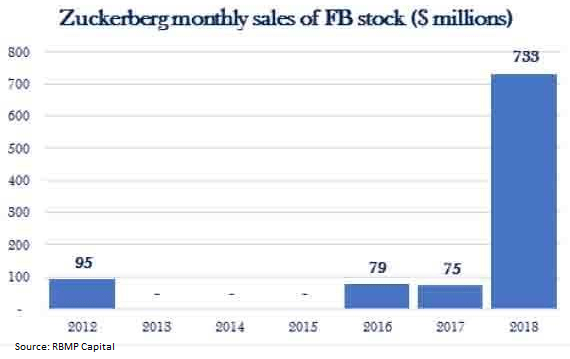

What is it about the warning that advertising growth was going to “come down meaningfully”, that markets didn’t understand from last year’s guidance? Perhaps it was our old friend ‘recency bias’ at work, given the sustained high rates of top line growth through both the second half of last year and into the first half of this one. Clearly markets thought Zuckerberg was crying wolf as they continued to drive the stock to record highs on each subsequent quarterly results. Given the almost complete lack of transparency on how FB really makes its money (*1), this seems quite bold of investors to assume they know better than the controlling shareholder what’s about to hit the fan, particularly when that insider was dumping record amounts of stock back into the market.

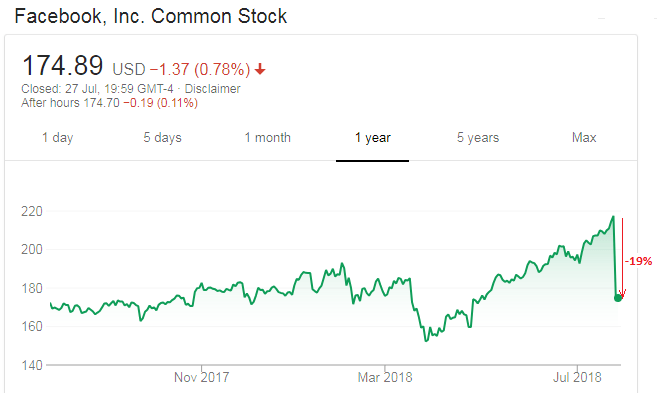

So what was it that triggered the -19% one day reversal in stock price? Organic sales growth slowed, but certainly not precipitously, or more than previous sequential reductions. This time however, it was accompanied by a hefty contraction in operating margins of -3.5ppts (to 45.6%) and a more specific set of forward guidance that had to spell it out to markets that this operating margin is expected to fall by a further -10ppts over the next “several” years. In case analysts hadn’t got the message, Facebook also made it very simple on revenues, in that one should expect a sequential slowdown in the rate of growth of up to -10ppts in each of both Q3 and Q4 of FY18. In other words, the current year which had started with a Q1 sales growth of +49% and delivered a still respectable +42% for Q2, could end the year with a Q4 growth rate nearer +22%.

Someone clearly was surprised!

Although not Zuckerberg, given the acceleration of his divestments.

(*1) Faith ought to be consigned to church rather than equity markets, but unfortunately that is rarely the case. Offer untold riches and a semi-credible growth story and there is no shortage to willing investors who are prepared to suspend their normal rational faculties to jump aboard what can soon become momentum plays. I am always impressed at the confidence of analysts on many of these wunder-kind internet stocks. Either management is breaching RegFD and disclosing privileged data on trading denied to the rest of us, who have to rely on a few lines of disclosure to try an piece together what’s really going on, or there’s a lot of hope and bluster going on amonst the share pushers. By being free of any sense of obligation towards management however, can be very liberating, particularly when something doesn’t quite add up. For instance, if you are touting yourself as an online retailer with a technological advantage in fulfilment, it would not be unreasonable to expect some scale advantage to become apparent, at least in terms of gross margins, once the operation has established its initial geographical rollout. When the reverse occurs and fulfilment costs continue to exceed sales growth, as too often seems to be happening with JD.COM, one might do well to question how the operation is really being run. The lack of real transparency is not just limited to Chinese internet operations, but also with the big US ones. For example, how much is really known about Facebook’s added value? It purports to make over 98% of its revenues from advertising. The owner of the world’s richest vein of personal data leverages this just to help businesses reach their target audiences it seems. Somehow, when even modest operations such as the DVLA in the UK are happily selling personal data on drivers to all and sundry, we are expected to believe that Zuckerberg holds FB to a higher ideal. Does anyone believe that the US intelligence services wouldn’t want to have access to all this data and if so, wouldn’t find ways to do so. The real question is whether FB gets paid for it and if so, would they actually want to admit to it.