Last comment update on: 2016-11-03

Q3 FY16: Facing short term investment pain, albeit with a credible future gain

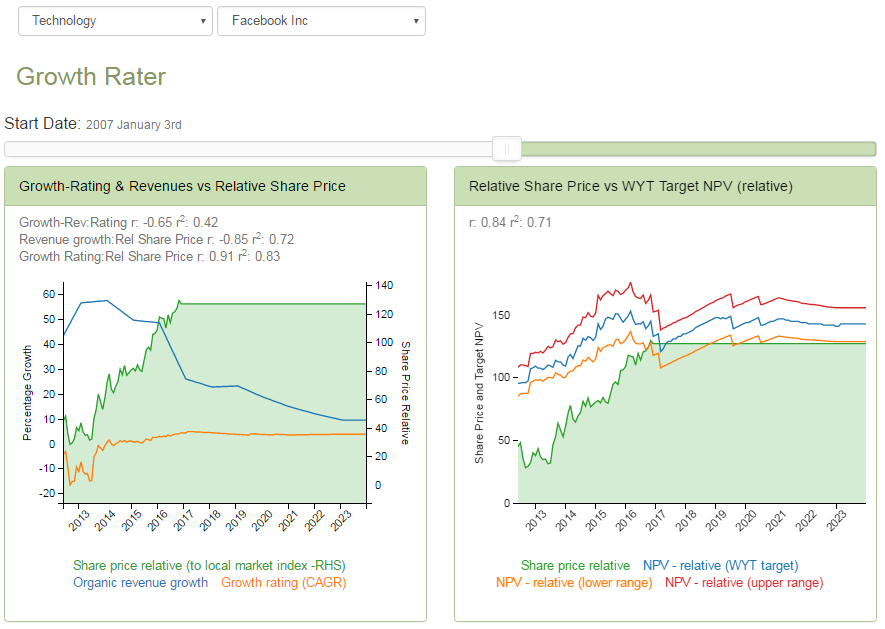

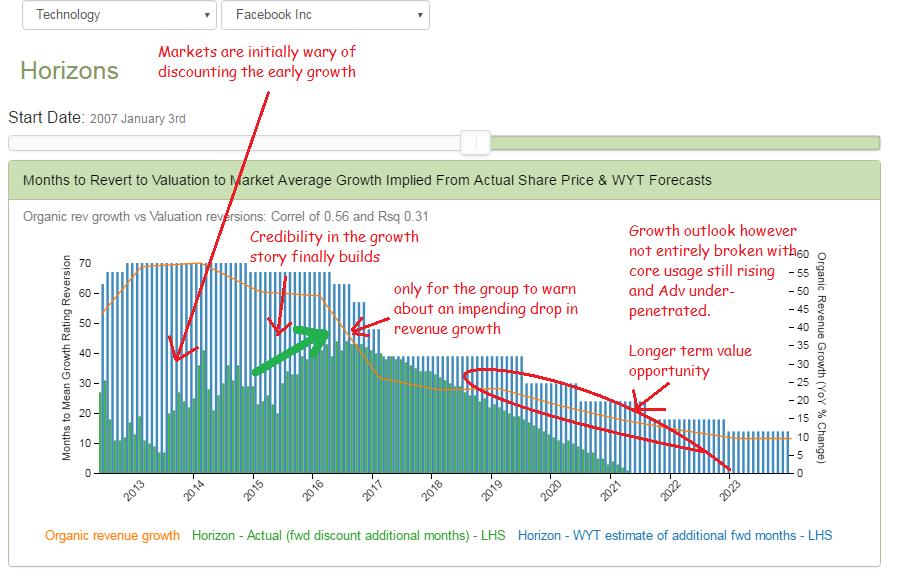

Facebook: For those that didn’t get the message at the previous quarter’s results, the group has reiterated its guidance for a slowing rate of revenue growth into next year, as advertising loadings near saturation, while also warning that costs will be moving the other way in what is now described will be “an aggressive investment year”. For now, the group has yet to provide the quantum on either revenue or OpEx which means there may be a healthy divergence in forecasts for FY17 as well as a possible reluctance by momentum investors to chase the longer term growth story until clarified. With Instagram, WhatsApp and several more projects such as Marketplace to develop, there is no shortage of potential to feed that growth story, albeit with an accompanying short term sacrifice to earnings. For deep value investors this will tick many of the right boxes; market leading and extendable brands in growing segments where capital can be applied and a controlling shareholder who is protected from short term restraints. For our GrowthRater valuation model, this confidence in a group’s longer term growth potential is also paramount in that super-normal organic revenue growth pushes out the horizon point on our mean reversion algorithm. With core usage still growing by +17%, an under-penetrated advertiser based to be exploited and then as the new investment areas come on stream we could still be looking at organic revenue growth running at +20-30% pa out to the end of the decade. If so, then we would expect a mean reversion on the GrowthRating to be pushed into 2020 to support a target NPV range of approx $120-150 ps.

Last trading report – Q3 FY16: Revenues increased by +56%/+$2.5bn to $7.0bn (o/w advertising of +59% to $6.8bn and payment & fees down -3% to $195m) with EBITDA up +91%/+$1.8bn to $3.7bn (vs Q1: +84%/+$1.2bn and Q2: +92%/+$1.6bn) after a +29%/-$742m rise in OpEx (vs Q1: +31% and Q2: +34%) and margins rising by +9.7ppts (vs Q1: +8.4ppts and Q2: +8.9ppts), from 43.2% to 53.0% on a 70% marginal revenue drop-thru rate (vs 64% in Q1 and 67% in Q2). After a +29% rise in depreciation charges to $396m (vs CapEx of $1,095m in Q3 and $3,222m YTD), EBITA increased by +102%/+$1.7bn to $3.1bn (vs Q1: +97%/+$1.1bn and Q2: +102%/+$1.5bn) with margins advancing +10.9ppts (vs Q1: +9.3ppts and Q2: +9.7%) from 36.4% to 47.3%. Including a slight increase (+8%/-$15m) in acquired intangible amortisation charge to -$195m, but a +$74m swing in net interest income (from -$27m to $47m) and -12.5ppts reduction in effective tax rate (from 37% to 25%) and GAAP EPS almost trebled from $0.310 to $0.830 (+165%). Excluding an 8% increase in stock comp expenses (from -$757m to -$815m), the above mentioned intangible amortisation and after a -7ppts drop in tax rate (from 31.3% to 24.3%), the company defined adjusted EPS increased by +91.3% from 0.567 to 1.085 ps.

KPI for Q3 included:

- Daily Av. Users: +17% YoY and +4.5% QoQ to 1,179m (o/w US +6.6% YoY and +1.7% QoQ to 178m, EU +9.9% YoY and +1.6% QoQ to 256m, APAC +22.7% YoY and +6.4% QoQ to 368m and RoW +22.4% YoY and +6.2% QoQ to 377m). Mobile DAUs meanwhile increased by +22% YoY and +5.6% QoQ to 1,091m

- ARPU +35% YoY and +5% QoQ to $4.01 (o/w N.Am +49.2% to $15.65, EU +36.0% to $4.72, APAC +36.0% to $1.89 and RoW + 28.7% to $1.21).

- Revenues: Advertising +59% to $6.816bn (97% of revenues) with Payments and other fees -3% to $195m.

Outlook: FY16 guidance, where provided is broadly unchanged on the one provided at the prior quarter, except for a further -5ppts reduction in the OpEx growth guidance ranges. Q4 revenue growth is expected to slow as the group cycles against high prior year comparatives (of +67.5%), a further drop in fees and a slowing rate of growth in Adv loading.

- Key guidance for FY16 includes:

• OpEx: GAAP expected to be at the lower end of the +30-35% guidance range

• OpEx: Adjusted (excl stock comp) +40-45%. Guidance trimmed from +45-50%

• Effective Tax Rate: FY16 estimated to be in line with YTD rate of approx 26%.

• CapExp: Estimated at approx $4.5bn – unchanged.

• Stock Comp: $3.1-3.3bn for FY16. Guidance unchanged.

• Amort: $700-800m for FY16. Guidance unchanged.

Q4 FY16 GrowthRater forecasts: For Q4, the group will be cycling against a comparative headwind of almost 16ppts compared with Q3 (with Q4 FY15 organic growth at +67.5% vs Q3’s +51.8%) which might suggest revenue growth for the forthcoming Q4 slowing to nearer +40%, even without a reduced rate of advertising loading growth. Including this, I have what may be a below consensus organic revenue growth assumption settling back to +30% with revenues of $7.332bn. With staff numbers already on the increase in Q3 (by over +30%) and against a soft comparative, I have Q4 OpEx rising by +36% YoY (vs Q3’s +29%), which reduces the rate of Q4 EBITDA growth to +25% (to $3.885bn and margins -2.1ppts to 53.0%) and a GAAP EPS up +55% from $0.54 to $0.84.

For FY17: No formal guidance is provided at the stage beyond an expectation that the increase in Ad loading that has been underpinning the surge in FY16 advertising revenues is estimated to only “grow modestly over the next 12 months” and will be a “less significant factor driving revenue growth after mid 2017”. Future areas for growth that will be developed will include WhatsApp and Instagram, although initially, this will come at an OpEx cost penalty. With advertising growth expected to slow “meaningfully” and FY17 representing an “aggressive investment year” (NB Q3 FTE’s +>30%), the group is again signalling a slowing outlook in earnings, albeit until the new development areas (such as Instagram and video) start to kick in.