Currency tail wagging investment dogs

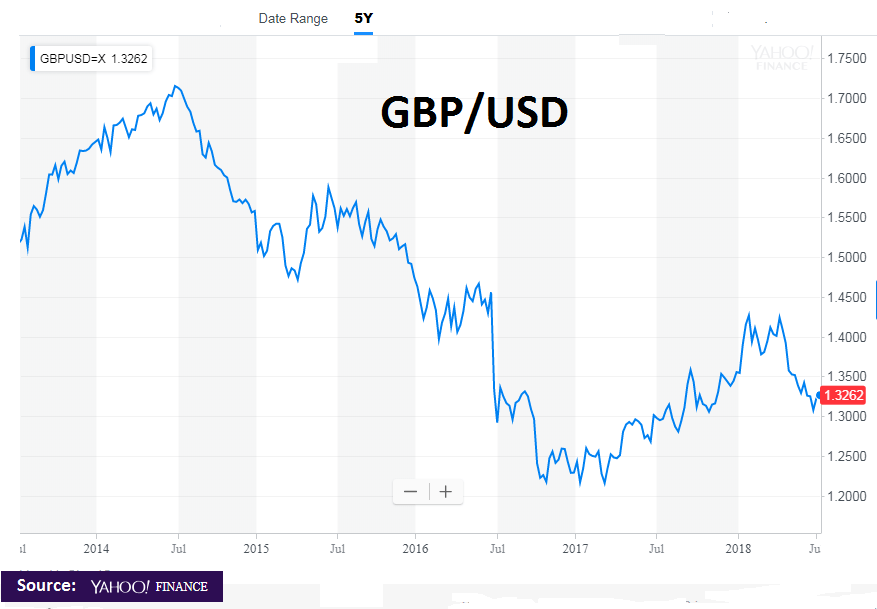

A safe play would seem to be to bet on UK Sterling weakening further. What matters is not that a ‘Hard Brexit’ might turn out a lot better for the economy than portrayed by ‘Project Fear’, or that Theresa May could still manage to secure Brino, but that evidence of the former would be beyond the time horizons and conditional responses of most currency traders, while the latter could only be achieved by May relying on opposition votes to pass the necessary legislation. With recent polls suggesting 70% of Tory constituency members support a real Brexit, a betrayal of this magnitude however, would break the party and consign it to oblivion for a generation, thus potentially letting in Jeremy Corbyn and a return to socialism. Neither eventuality therefore seem particularly conducive for the short term outlook for Sterling.

Project fear = lower GBP?

For the UK equities, markets look set to be driven by traders, rather than investors. Stocks with a high proportion of profits generated outside of sterling will obviously benefit from the conversion back into GBP, while exporters with an above weighting of domestic costs will get some additional leverage on margins. A complicating factor for this latter group however will be the shifting base of tariffs, both between the US and everyone else and possibly also between the EU and UK after March next year.

As a short term trader, what you might want therefore is a business with an above weighting of GBP costs relative to a high export component, but which is below the radars of the current tariff wars.

One such area is amongst science journal publishers. They are not exposed to higher imported costs when sterling falls, while the pricing of overseas journal subscriptions are usually set in respective market currencies or in USD. Lower Sterling therefore means an increase in marginal revenues over a stable cost base and therefore a further leverage to margins and earnings. This is why the two main stocks in this area, RELX and Informa have been outperforming as sterling weakens and markets drop on trade war fears.

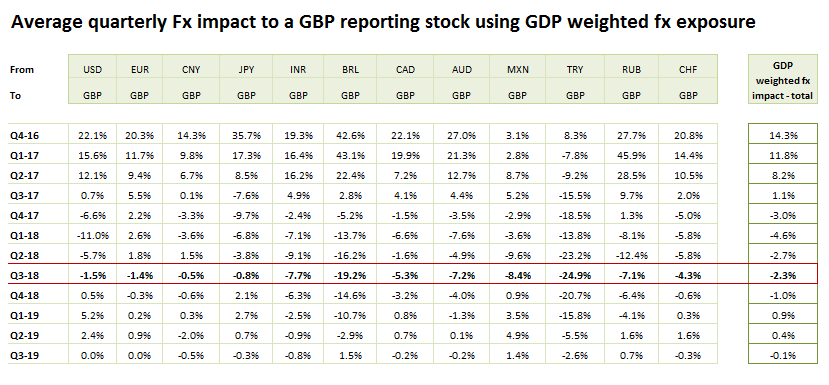

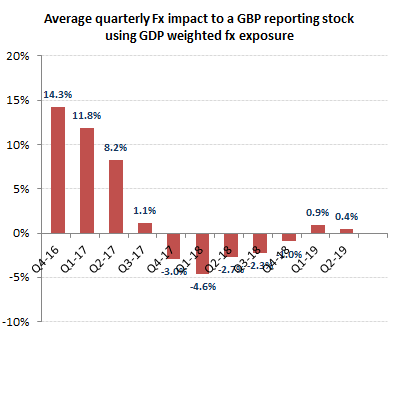

This however, is more of a short term defensive trading tactic rather than as a recommended investment strategy. While the margin leverage is welcome, the actual impact is relatively modest in the context of current exchange rate movements (see table below). Operating margins in this space are also very high and can range from 30-40%, which dampens the percentage impact. For example, even assuming a full USD revenues and full GBP costs on the highest impacting quarter (Q1 2019) with its +5.2% fx tailwind, this would add only around +14% to that quarter’s EBITA, assuming a base margin of 35%. Include exposures to other currencies, some of which are falling faster the sterling (hit more by the tariff wars) and overseas marketing and distribution overheads and that actual benefit could shrink significantly. To buy into a low growth and structurally declining business just for a possible future currency benefit seems like the tail wagging the dog. A good trading ideal for a week or so, but a poor basis for an investment.

re Informa: this stock is mainly exposed to overseas exhibitions, including HK and some legacy slow growth events in the US and UK, so not without some offsetting cyclical/tariff exposure.