MMT – Safe and Effective?

An experimental theory adopted by a financially rewarded ruling oligarchy has always been difficult to fight against, so you won’t find many among those beholden to them that will be prepared to risk their careers by challenging the status quo. Until it is too late, that is!

We therefore have entered a twilight zone where the official narrative doubles down on a belief system that is increasingly exposed as fraudulent, notwithstanding it being simultaneously dismantled by events as they unfold. As with a proverbial rubber band, those currently in control of the narrative can try and keep on stretching the credibility of markets, but at some point, risk will pass the point of no return and snap the elastic. While recency bias will often encourage the herd to assume some sort of gradual and linear adjustment, others may appreciate that a more realistic outcome may be better explained by the Catastrophe Theory. It wouldn’t be the first time ‘safe and effective’ was followed by ‘died suddenly’.

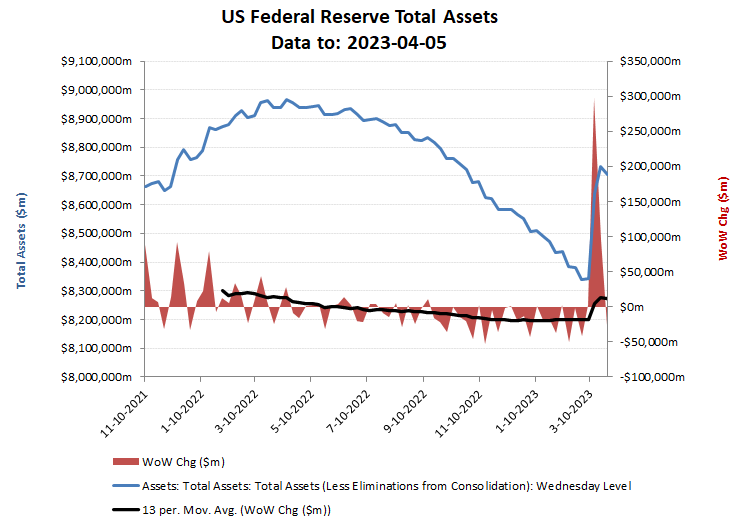

After the loss of the House (of Representatives) to the GOP last November, it was to be hoped that further damage from the Democrat’s irresponsible fiscal and energy policies might at least be controlled and then possibly reversed after the forthcoming the 2024 elections. Indeed, the recent push-back on the administration’s request to raise the debt ceiling and the rollout by the US Fed of its $95bn per month balance sheet reduction suggested the start of this process, something that was well received by currency markets. Remove the US Federal Reserve debt monetisation and the inevitable consequence is the return to market pricing of capital and the normalisation of interest rates. Unfortunately, instead of doing this a decade ago while economic conditions were robust, this has now been forced on the Fed into a stagflation, perhaps predictably!

However, after a couple of bank failures, (SVB and Signature), the US Treasury and Fed have been panicked into pumping liquidity back into the system, with the usual excuse of stopping contagion. This has taken the form of a backstop facility to banks and ‘eligible’ firms to borrow against Treasuries, mortgage backed securities and other eligible collateral at face value of these instruments. Firms can do this for up to a year at a borrowing cost of the one-year overnight index swap rate plus 10 basis points. This therefore means that all those banks caught out buying long dated bonds when yields were low can use them to access liquidity from the Fed at their par, rather than market value. IE kick the can down the road for another year with a liquidity fix to disguise a solvency problem – some things clearly never change!

As well as being yet another example of encouraging moral hazard, the privileged treatment of SVB and Signature Bank depositors raises a couple of further red flags. Here, the $250k deposit insurance cap was extended to all depositors; something the Treasury Secretary Janet Yellen refused to confirm would now be extended to all US bank depositors. Firstly, this appeared to confirm a two-tiered application of the rules, as both these banks vigorously promoted Democrat political agendas and included a substantial number of wealthy Democrat donors accounts, which would have particularly benefited from the having the deposit insurance limit raised. Presumably, so too would have been the >10 reported billionaire Chinese accounts who may or may not have been connected to the ‘Big Guy’ and Mr 10%! For less woke or politically connected smaller regional banks, these actions meanwhile will have merely increased the risk of bank runs for this group (as the $250k deposit insurance cap presumably would still apply) and into the larger and more politically favoured ones.

The good news perhaps, is that the systematic risk to the US banking system to a partial normalisation of bond yields back to around 4% may not be as severe as the headlines surrounding SVB and Signature suggested and that their focus on rampant wokery rather than risk management and CROIC were more significant causes. While effective in bouncing the Fed into covering for their wealthy donors caught with large deposit accounts in these banks, it still has that whiff of corruption about it, which with the disastrous testimony of Janet Yellen to Congress on the 16 March has done much to hole the US dollar and drive up the gold price.

It’s Okay, just another $400bn ‘temporary’ emergency expansion!

Janet Yellen: 16 March 2023 Congressional Testimony

Having colluded in funding via debt monetisation the deficit spending while as US Federal Reserve Chairman, Janet Yellen (JY) now as US Treasury Secretary is now understandably trying to (CYA and) defend these fiscal and monetary expansions as the government funding edifice crumbles under her feet as previous policy expansions come back as inflation, which in turn challenges the capacity for further monetisation.

I have included here two clips from this testimony, with Senator Ron Johnson (RJ).

In the first, we can see how far apart Senator Johnson and Janet Yellen are in terms of monetary theory. Here RJ adopts a Milton Frienman classical monetarist position in that inflation is ‘always and everywhere a monetary phenomenon’ — a problem of printing too much money. By contrast, JY adheres to Modern Monetary Theory, which denies this and is therefore understandably popular with governments eager to hide their deficit spending by monetising it. It is perhaps unsurprising to find that governments prefer to employ MMT economists rather than classical monetarists. The same of course applies to financial institutions which will profit on the teat of all this monetary expansion. Most economists (and therefore published opinions) are therefore are MMT ones (as they get the jobs), but now have a problem of shifting the blame for the current surge in inflation as unsustainable increases in debt remove the camouflage of suppressed interest rates for monetised debt buy-ins (QE). As it would also be politically incorrect to ascribe it to climate change and other socially virtuous policies, expect the focus to be on Putin instead!

- RJ: “Would you agree that those are the top three causes of inflation, deficit spending, high energy costs and supply dislocations?”

- JY: “I don’t believe that deficit spending is one of the main causes”

- RJ: “You don’t! Inflation is too many dollars chasing too few goods”

Here, we see the collision of two world’s. The incumbent official narrative that is convenient to the vested interests of the money printers and those in close proximity against those suffering the now more punitive effects of this debasement.

[videopack id=”16271″]https://growthrater.com/gr_web_m1/wp-content/uploads/Yellen-Congressional-Testimony-Deficit-spending-and-inflation.mp4[/videopack]

In this second clip, I have included the section where Senator Johnson challenges Secretary Yellen first on the quantum of the planned deficits in the current administration’s budget and then on how it intends to finance it.

After having to interject to reveal the extent of the planned deficit spend in the budget over the next 10 years (of $17 tn), when Janet Yellen struggles to disclose this figure when asked. RJ helps to add this up for JY, by asking

- RJ: “You’re going to drive the debt from somewhere around $32 tn up to around like $50 trillion, correct?”

- JY: “Yes, but..what, what I believe is the single most important metric for judging the fiscal stance of the country is the real net interest as a share of GDP”

- RJ: So when you’re taking the debt up from $32 to $50 tn, the concern is who is going to buy that debt and also at what rate they’ll expect to be compensated for buying riskier and riskier debt? Are you concerned about that?

- JY: Well if the real net interest costs of the debt remains low relative to GDP and we’re on a sustainable fiscal ..

- RJ: No we’re not on a sustainable fiscal path

This reply by JY is revealing. While correct in that it is the level of interest costs relative to GDP that is the relevant measure of debt affordability, it utterly ignores the obvious flaw that RJ highlights in the second clip, that of the rate of interest that the US Treasury will have to offer on future bonds in order to sell them. This is where the credibility of US Govt financing and inflation management is so important, along of course with the credibility in the US dollar itself as the World’s reserve currency.

[videopack id=”16273″]https://growthrater.com/gr_web_m1/wp-content/uploads/Yellen-Congressional-testimony-deficit-rising-from-32-to-57-trillion.mp4[/videopack]

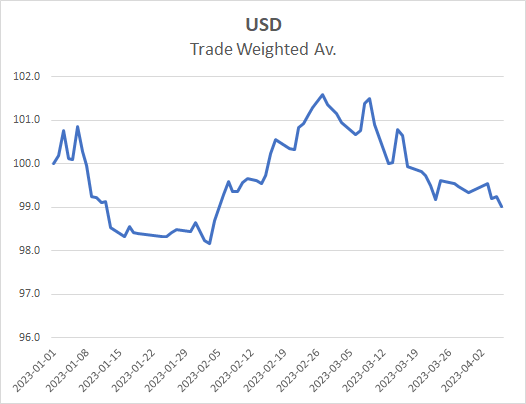

Following this congressional testimony and the US Fed’s $400bn balance sheet expansion to backstop bank liquidity and bond portfolios, the US dollar has reversed much of its earlier gains following the $95bn pm QT programme, while the Gold price was initially up over +7%/+$140/Oz to $2,045/Oz, albeit now has settled back to MoM gain of approx >+5%/+$100/Oz.

After the meeting of Xi in Moscow with Putin, support meanwhile for de-dollarisation has been gathering pace and even raised speculation that the Saudis might sell oil to the Chinese for Yuan, rather than US dollars. The Saudi Minister of Finance, Mohammed al-Jadaan, has already made no secret that Saudi Arabia might sell oil outside the traditional US dollar and in January at Davos in an interview with Bloomberg said:

“There are no issues with discussing how we settle our trade arrangements, whether it is in the US dollar, whether it is the euro, whether it is the Saudi riyal,”

While at this stage, this is perhaps meant as a warning shot to the current US administration, but given the importance of the ‘petro-dollar’ to the USD reserve currency status this can not be underestimated. Under Yellen’s budgetary plans, the US deficit was projected to top $1.6tn for 2023 and $1.85tn for 2024, while never dropping below $1.5tn pa. A rising deficit towards $50tn and without a reserve based demand for this, the US will have to compete for capital along with everyone else. Assuming it is unable to print its way out, the real Treasury yields could normalise back to a 1.5-2.5% range and possibly the higher end of this range with people like Yellen and Biden at the helm. Assume an average inflation rate of 3% and that could suggest a bond yield of at least 5.5% will need to be paid, which on the additional $17 tn of deficit spending would equate to an additional interest bill of almost $1 tn pa by the budget period end and a total Federal Government annual interest bill approaching $3 tn pa. – to answer Senator Johnson’s question

“what rate they’ll expect to be compensated for buying riskier and riskier debt? Are you concerned about that?”

Reverse QT and reverse all that good work supporting the USD