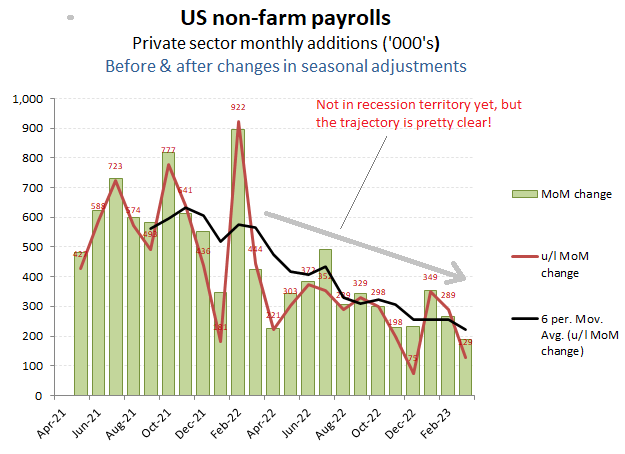

March Jobs data – further softening, but not there yet!

While the real action is increasingly out in currency markets, the monthly guesstimates from the BLS provide an element of background mood music. For March, the picture remains one of gently easing rates of net job additions, but not yet in negative terratiory, but with real incomes failing to keep pace with inflation and indeed, with the annualised rate of hourly wage growth heading in the wrong direction and at approx half the rate of February’s CPI of 6.0%.

While seemingly good for future core inflation expectations, as it suggests employment markets may not be as tight as previous feared, which in turn eases concerns regarding a potential wage/inflation spiral, it also might suggest a weaker economic situation than the current headline employment figures might suggest.

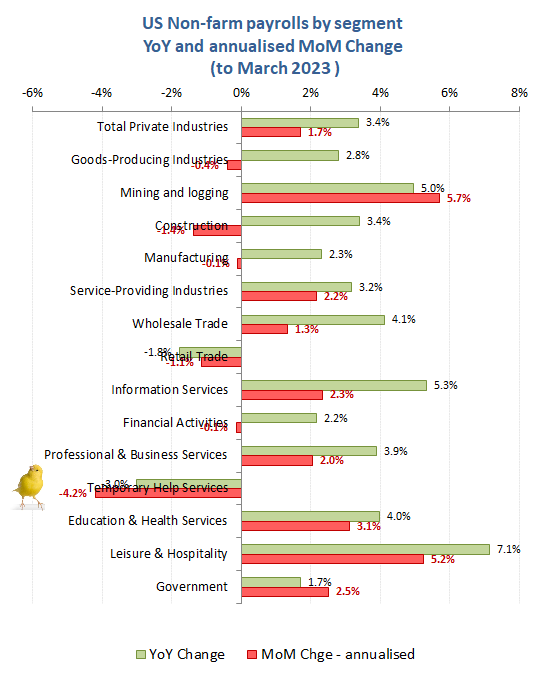

This might also be the conclusion drawn when drilling down into the employment categories (below chart). Here, the notable standouts in March was the contraction in employment in construction following the rise in mortgage rates, but also in manufacturing, which suggests the post lockdown rebound is now over, while rising feedstock and raw material prices is squeezing demand. The other interesting development was the sharp contraction in temporary help services. While in good times this can reflect a hot/tight job market which encourages employers to offer full time and better contract jobs. However, in bad times this can also suggest employers are initially shedding the easy fires first, but prior to cutting into the meat should demand remain depressed. The combination of falling temporary employment together with weak average wage growth would suggest such an environment is indeed underway, apparently supported by the public announcements of layoffs by a number of large employers in retail (Walmart) and restaurants (MacDonalds), which may be more apparent in future BLS job statistics

Falling Temp jobs + weak wage growth = the Canary in the mine

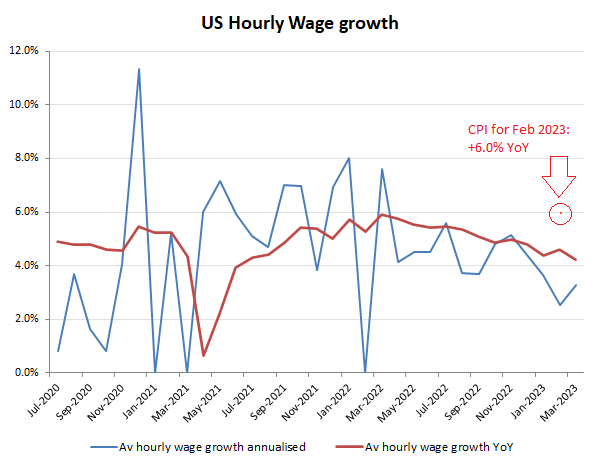

Labour market not as tight as some suggest, with average hourly wage growth in March almost -2ppts below the last reported YoY CPI figure (of +6.0% YoY for February), while annualised rate of hourly wages was nearer -3ppts below CPI.

Real wages still in decline

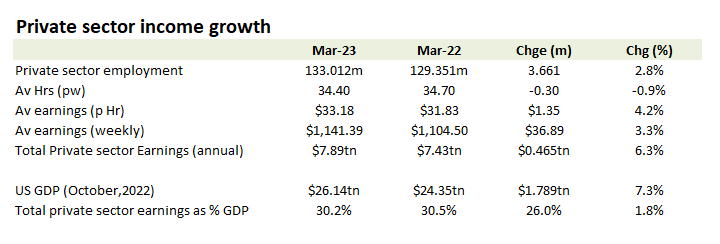

An additional feature picked up in the below summary table has been the squeeze on average hours worked. On a YoY basis, that stripped almost -1ppts from whatever benefit one recognises from the average hourly wages (either the +4.2% YoY figure or the lower annualised rate for March of around +3%. Even taking the higher of these, suggests YoY average private sector earnings per capital rose by only +3.3%. With higher mortgage rates, energy and taxation, it would seem the squeeze is on, unless of course one cab get some of that new easy money being doled out by the Fed to bailout their woke failing banks!

Average wages up only +3.3% YoY in March