Value traps and opportunities and how to spot them

With a relative lull today in the results deluge, I thought it might be interesting to review how some of last week’s stack up, but from a GrowthRating perspective. As we’ve all had to wade thru far to much verbiage, I’ve kept it simple with some annotated charts and only a very few words. The stocks chosen I think provide good examples of how some cherished brands can suck investors into value traps, which sometimes close gradually (such as with Coca-Cola and Thomson), or more abruptly (as with Nielsen).

- If you’d like a fuller version of below synopsis or to check out any of the other recent updates (list at end), these can all be found at: https://app.growthrater.com/

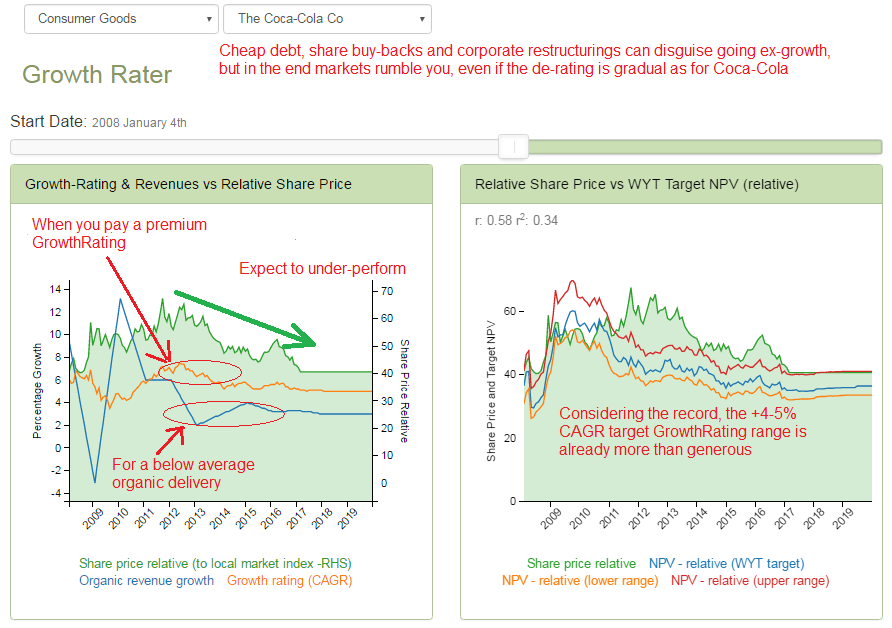

- Coca-Cola – slow de-rating

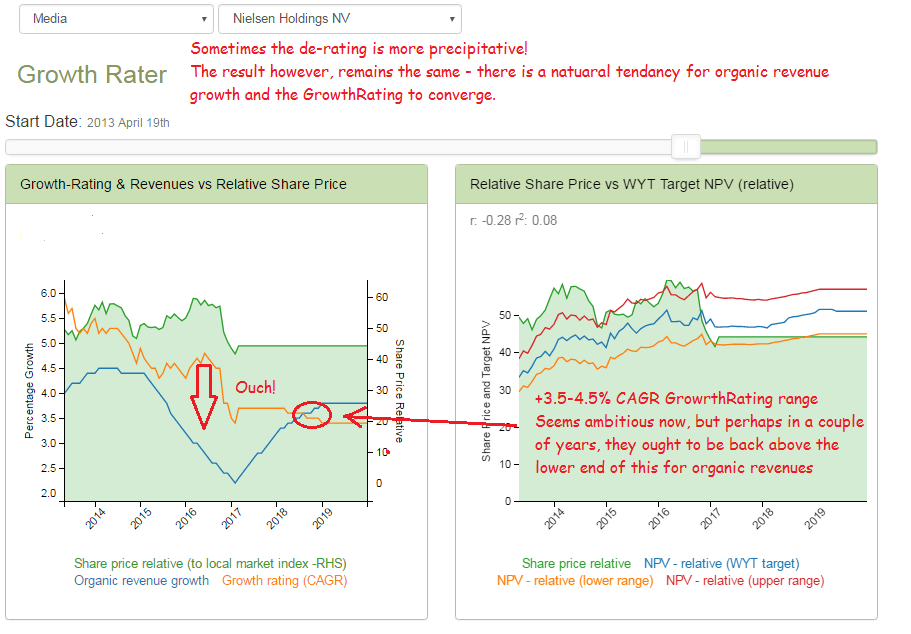

- Nielsen – the penny drops after the initial PE investors have bailed out

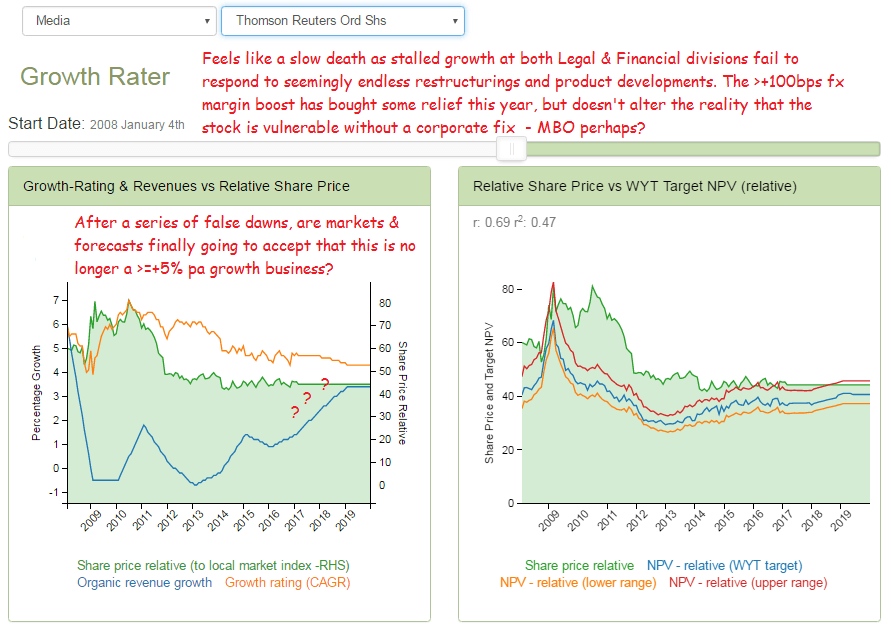

- Thomson Reuters – FX provides a >+100bps margin tailwind, but the valuation gap remains

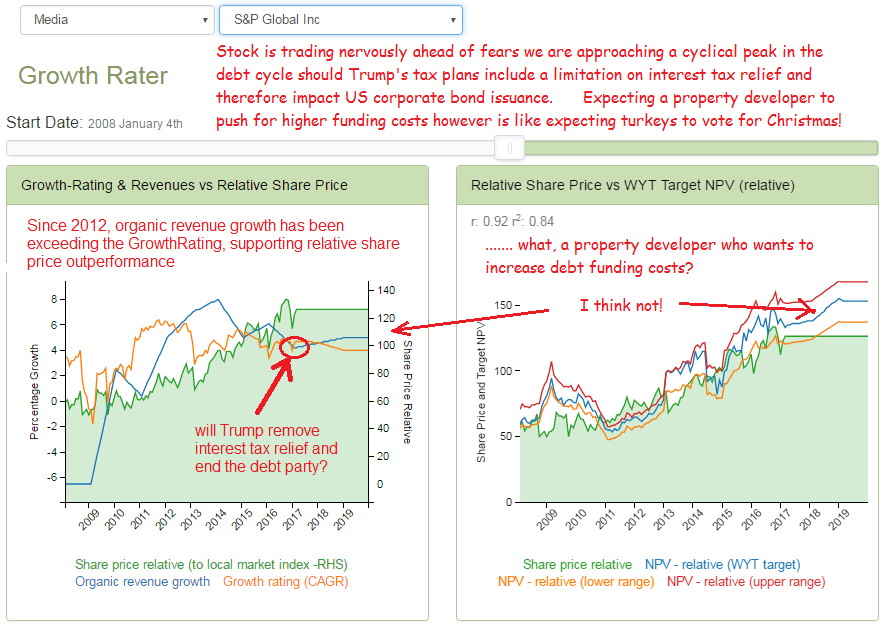

- S&P Global – where organic revenues lead GrowthRating and relative share price outperformance

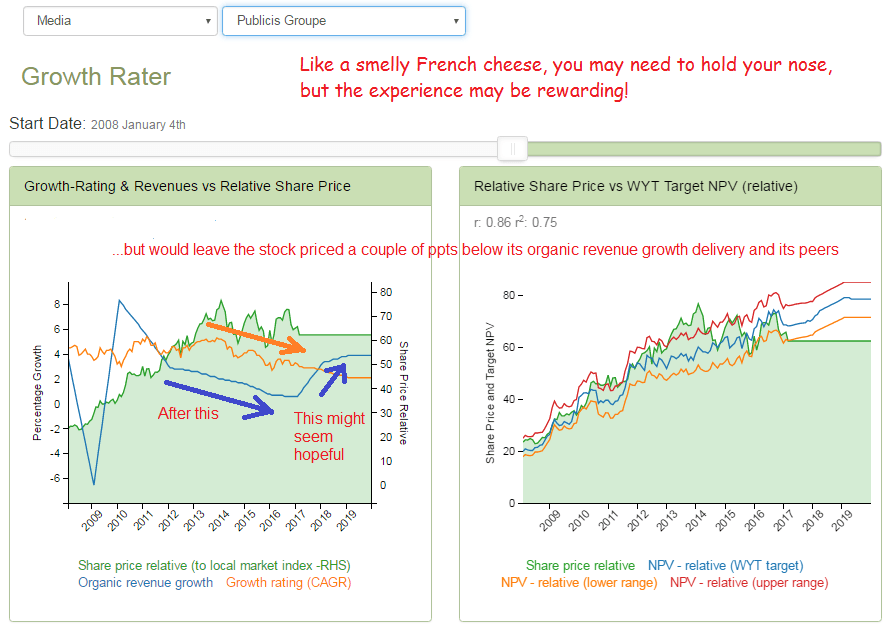

- In the agency sector: Publicis – Like a French cheese, you may need to hold your nose, but the experience might be rewarding

Coca-Cola – slow de-rating

Behind the treasury management, share buybacks and corporate restructurings, the reality is a GrowthRating (and relative share price) being dragged down by a lower organic revenue delivery

The coke choke?

Nielsen – the penny drops after the initial PE investors have bailed out

For Nielsen, the reaction to an under-performing top line has been more precipitative. Perhaps markets were spooked that the growth and margin story was being walked back once the PE investors had bailed out! For the patient however, the current GrowthRating of approx +3.5% CAGR is not unreasonable given the substantially syndicated business and as we’ve seen with GfK, the space still has its PE supporters and potential corporate deal makers.

The precipice

Thomson Reuters – FX provides a >+100bps margin tailwind, but the valuation gap remains

How many years of markets believing analyst forecasts of recovering organic sales momentum by year 3, before they finally capitulate and accept that after series of restructurings and new product initiatives, this might no longer be a >+5% pa growth business? Cost cutting and the recent fall in GBP (the latter adding >+100bps to margins) have bought some time and stabilised the relative share price performance, but with Legal & Financial publishing still flat-lining, the group will need to pull another rabbit out of its hat to defend the shares. More restructuring, or perhaps the long rumoured MBO?

Slow death

S&P Global – where organic revenues lead GrowthRating and relative share price outperformance

Since 2012, group revenues have run ahead of the growth rate implied from the OpFCF yield and notwithstanding legal settlement costs, this has also accompanied a share price outperformance. Given the high levels of operational gearing inherent in its Ratings and Indices activities and their sensitivity to bond issuance and AUM growth at associated EFTs, the chief concern for the valuation will be whether we are approaching the top in the debt cycle, which may also be hastened by speculation the a Trump tax reform may include reductions, or even elimination, of interest tax relief for corporations. However, as a debt fueled property developer, this would seem to go against the grain, suggesting these fears may be over-done.

Will Trump’s tax plans limit interest tax deductabiity?

In the agency sector: Publicis – Like a French cheese, you may need to hold your nose, but the experience might be rewarding

The stock carries some baggage (more like Louis Vuitton) following its aggressive digital acquisition spree, subsequent merger attempts, over-ambitious forecasts, insider sales and more over-ambitious forecasts. It is not the first marketing services group to over-reach themselves in trying to buy in growth and new skills and probably won’t be the last. WPP has done it at least a couple of times and IPG struggled for years, but look at them both now. Fortunately for them, markets are forgiving and blessed with conveniently short memories once top line growth is restored. For Publicis, the question is whether some of the recent business wins and the inclusion of Sapient (last seen raising sales by approx +7%) makes the prospect of a return to positive organic revenue growth in the second half of 2017 a realistic prospect. If so, while it may pain me to say it, the stock may not be unattractively priced on a GrowthRating of under +3% CAGR

A case of holding one’s nose

Recent Reviews

| Date | Company | Event |

|---|---|---|

| 2017-02-12 | S&P Global Inc | Playing safe: Mid-range valuation on a mid-range guidance ahead of Trump tax/tariff uncertainties |

| 2017-02-12 | The Coca-Cola Co | Q4 FY16: u/l headwinds to rating and shares likely to persist |

| 2017-02-12 | Nielsen Holdings NV | Q4 FY16: Markets finally seem to be getting the message! |

| 2017-02-11 | Thomson Reuters Ord Shs | The longer the recovery is deferred, the greater the risk of a more precipitative de-rating |

| 2017-02-11 | Interpublic Group of Companies Inc | FY16 results: Solid delivery, barring the W/Cap inflow which is something to check for in Q1 FY17 |

| 2017-02-09 | Publicis Groupe | FY16 results: Maurice promises another H2 recovery – 3rd time lucky? |

| 2017-02-07 | Kraft Heinz Co | Review: After the cost savings the narrative will turn top line growth, or the lack of it! |

| 2017-02-07 | Omnicom Group Inc | Q4 & FY16: A solid risk/reward agency play for FY17 |

| 2017-02-06 | Ryanair Holdings | Q3 FY17: Race to the bottom will be won by the lowest cost operator |

| 2017-02-05 | Gartner Inc | Review: Slowing underlying EBITA growth ahead of earnings accretive acquisition |

| 2017-02-03 | Amazon.com, Inc. | Q4 FY16: Short-term top slice around a longer term over-weight position |

—