Soaring gold prices and gold miners

to 2024-04-08")

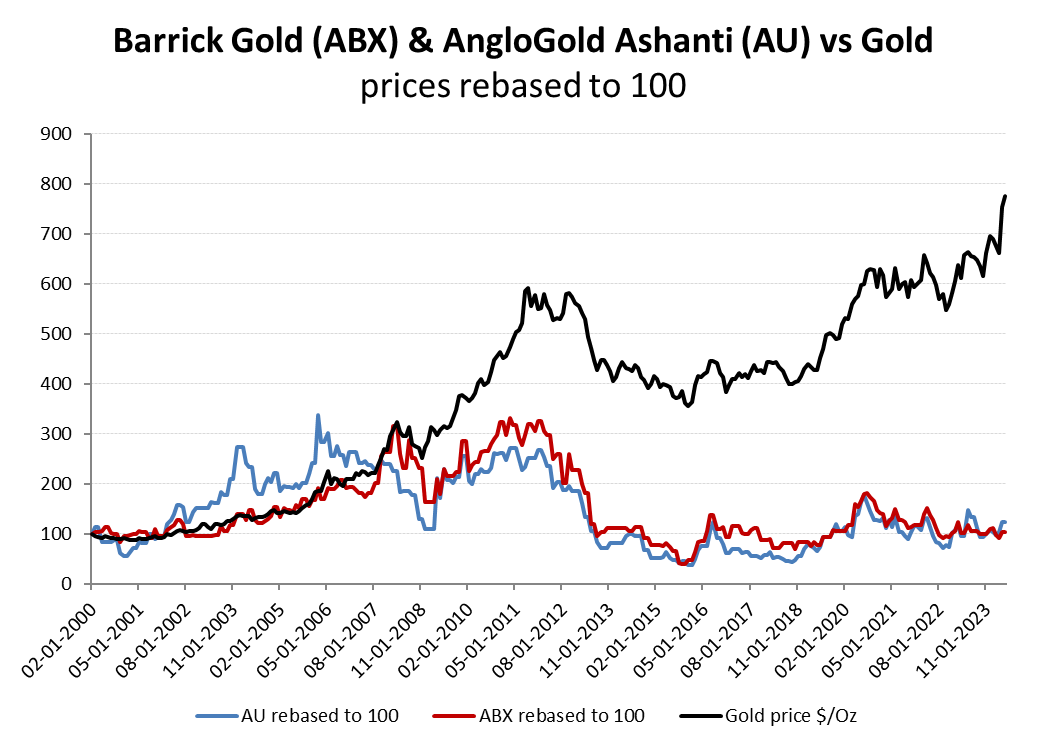

As markets lose faith in the Fed’s ability to manage its easing pivot, gold and silver prices are soaring to new records notwithstanding hardening long bond yields. For investors wanting to participate in this trade, the choice seems to be between physical gold bullion, paper gold certificates or those mining the stuff. Those with a secure depository, or access to one, must rank at the top of this food chain given the >100:1 leverage of paper gold and therefore risk of delivery default, but what of investing in miners? Surely the combination of operational and some financial leverage ought also to gear up the overall share price leverage of these entities to a rapidly rising gold price. While good in theory, reality however, has taken a drastically different course for the sector’s two largest listed corporations, Barrick Gold (ABX) and AngloGoldAshanti (AU). Although there hasn’t been much in it between the two groups since the start of the millenium, both have barely advanced in terms of share prices against a gold price that is almost 8 times higher. The root cause of this doesn’t seem to be ant significant erosion in operating margins or indeed market rating, whether that be a relative earnings rating of EBITA multiple, but a failure to allocate excess capital at an above market CROIC. As a consequence, sector valuations have been largely stripped of an opportunity premium, with the share prices broadly reflecting little more than the cash NPV of their proven/probable reserves.

What a shocker!

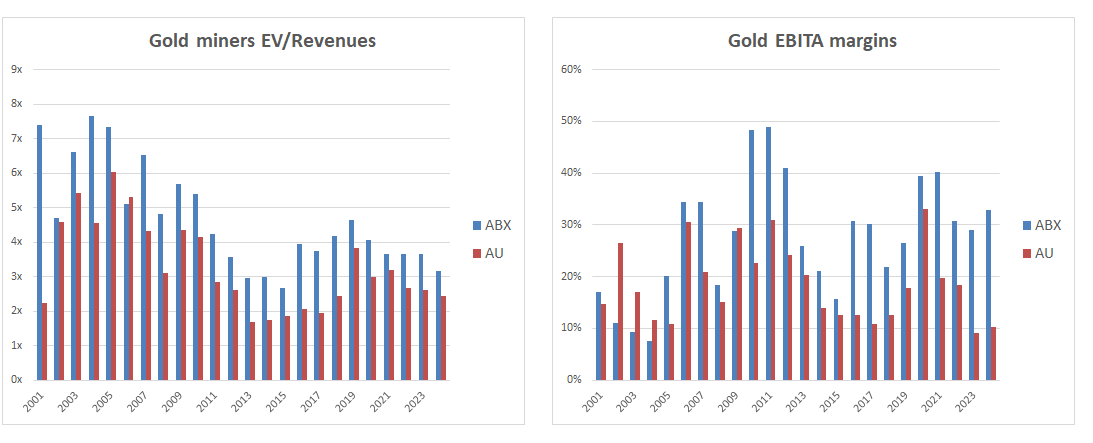

Notwithstanding an initial improvement in the earlier part of this period, operating margins and the EV/revenue multiples are broadly back to where they started and particularly for AU

Initial enthusiasm has evaporated

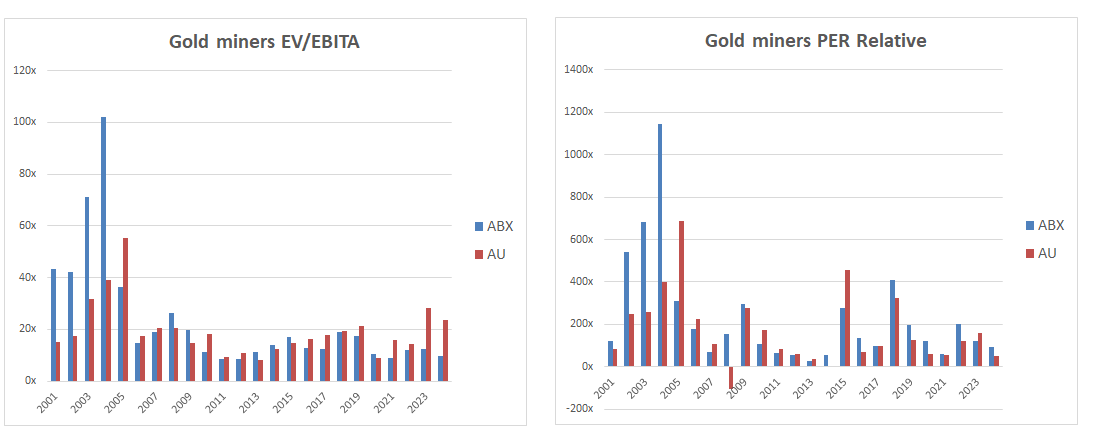

Much of the same meanwhile can be observed for earnings based metrics

Stalled valuation multiple expansion

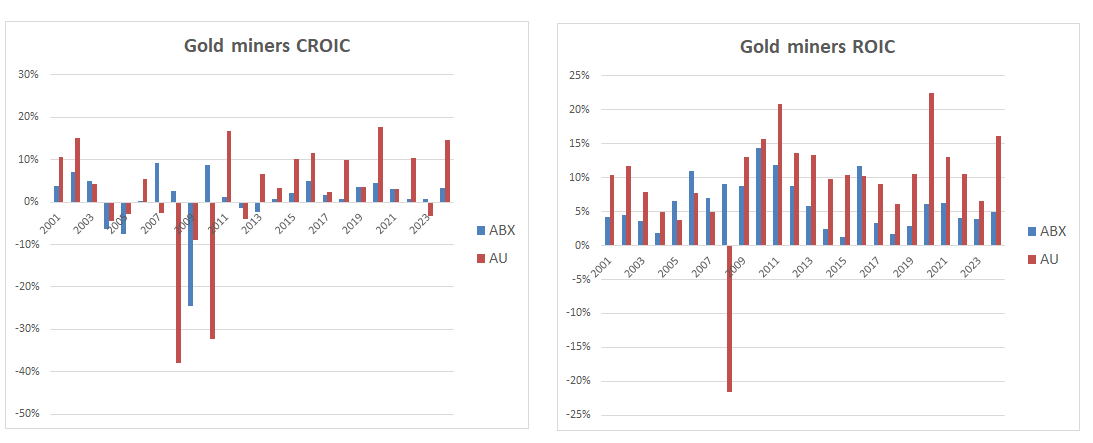

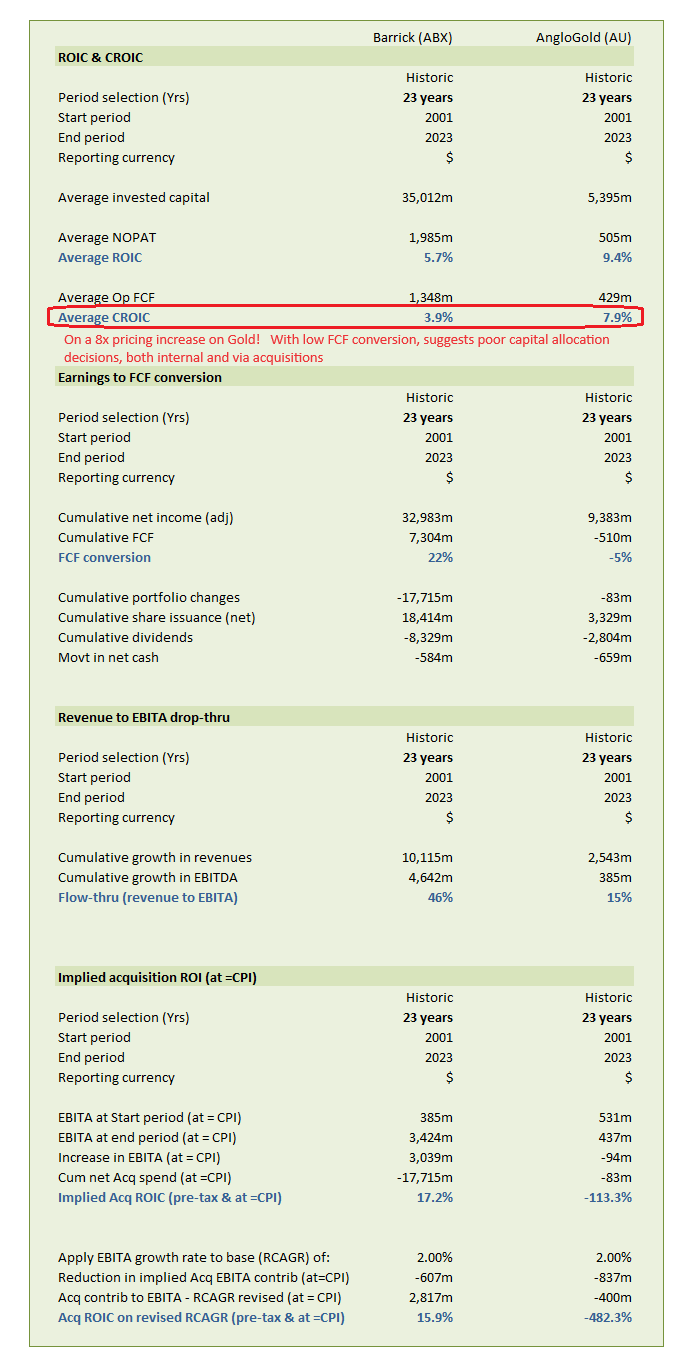

Operational and financial leverage from an 8 times increase in gold prices ought to have been reflected in some significant advances in CROIC. The fact that this hasn’t occurred is a major red flag.

Low cash conversion combined with a weak ROIC

Drill down to analyse the cumulative progress for each company over the period highlights the problem. ABX has focused on acquisitions, while AU’s capital has been invested primarily internally, but the net effect has been broadly the same. On the basis of this performance it is not surprising that markets are reluctant to award an opportunity premium for the potential returns from applying excess capital.

How not to allocate capital!

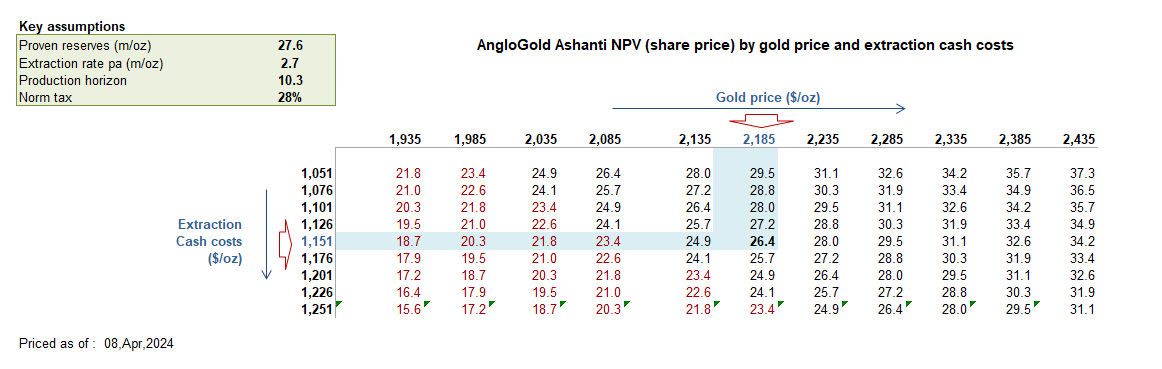

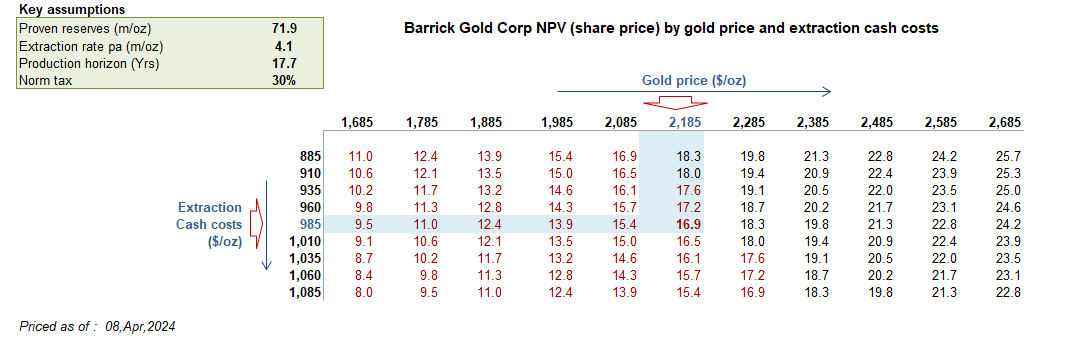

Valuation – cash NPV and valuation sensitivities

In light of the above experience, it is perhaps unsurprising that the share prices of both ABX and AU have been largely shackled to the cash NPV of their proven/probable ore reserves and bases on prevailing gold prices. Below are copies to the current NPV sensitivity models for both ABX and AU, with the highlighted column reflected the estimated average price per troy ounce for 2024. Those expecting the price to hold at the current level of approx $1,350/oz can therefore see the impact on the share NPV.

Barrick Gold (ABX)

Cash NPV valuation and sensitivities to gold prices

AngloGold Ashanti (AU)