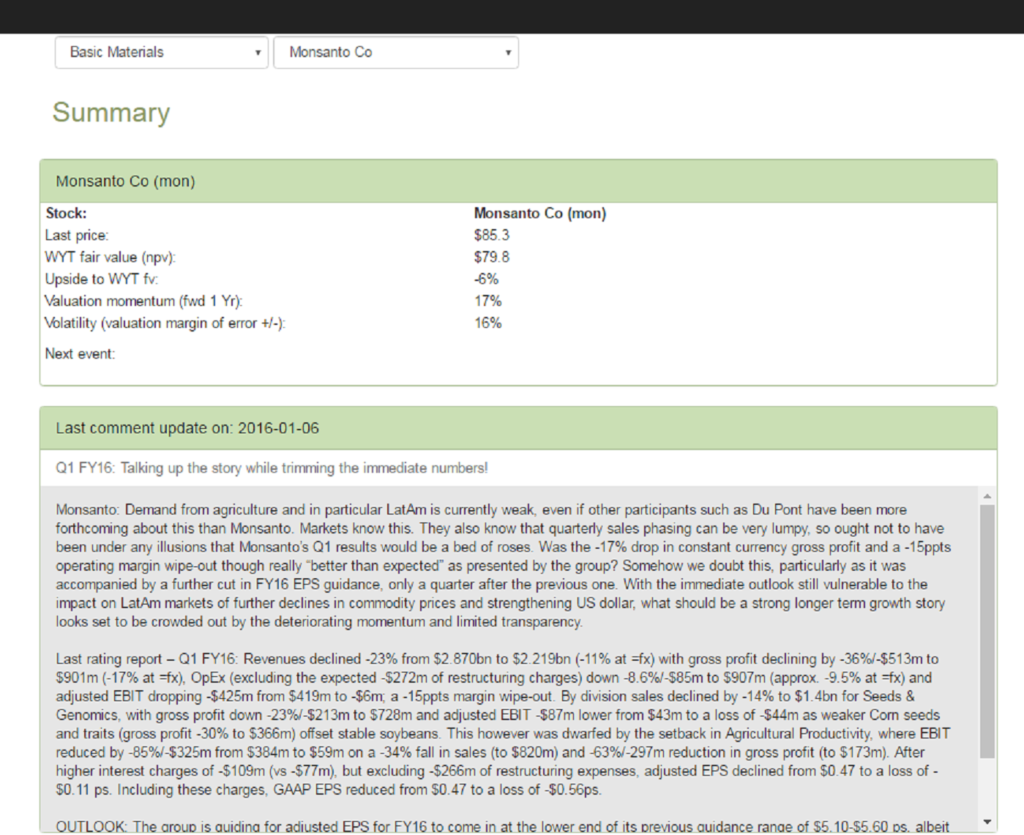

Monsanto: Demand from agriculture and in particular LatAm is currently weak, even if other participants such as Du Pont have

been more forthcoming about this than Monsanto. Markets know this. They also know that quarterly sales phasing can be very lumpy, so ought not to have been under any illusions that Monsanto’s Q1 results would be a bed of roses. Was the -17% drop in constant currency gross profit and a -15ppts operating margin wipe-out though really “better than expected” as presented by the group? Somehow we doubt this, particularly as it was accompanied by a further cut in FY16 EPS guidance, only a quarter after the previous one. With the immediate outlook still vulnerable to the impact on LatAm markets of further declines in commodity prices and strengthening US dollar, what should be a strong longer term growth story looks set to be crowded out by the deteriorating momentum and limited transparency.

Last rating report – Q1 FY16: Revenues declined -23% from $2.870bn to $2.219bn (-11% at =fx) with gross profit declining by -36%/-$513m to $901m (-17% at =fx), OpEx (excluding the expected -$272m of restructuring charges) down -8.6%/-$85m to $907m (approx. -9.5% at =fx) and adjusted EBIT dropping -$425m from $419m to -$6m; a -15ppts margin wipe-out. By division sales declined by -14% to $1.4bn for Seeds & Genomics, with gross profit down -23%/-$213m to $728m and adjusted EBIT -$87m lower from $43m to a loss of -$44m as weaker Corn seeds and traits (gross profit -30% to $366m) offset stable soybeans. This however was dwarfed by the setback in Agricultural Productivity, where EBIT reduced by -85%/-$325m from $384m to $59m on a -34% fall in sales (to $820m) and -63%/-297m reduction in gross profit (to $173m). After higher interest charges of -$109m (vs -$77m), but excluding -$266m of restructuring expenses, adjusted EPS declined from $0.47 to a loss of -$0.11 ps. Including these charges, GAAP EPS reduced from $0.47 to a loss of -$0.56ps.

OUTLOOK: The group is guiding for adjusted EPS for FY16 to come in at the lower end of its previous guidance range of $5.10-$5.60 ps, albeit with timing changes in restructuring charges expected to bring GAAP EPS to the upper end of its $4.12-$4.79 ps range. The group is reiterating its $500m pa of cost savings by end 2018 as well as its targeted CAGR in EPS from 2016-19 of +20% pa.