Will the Euro replace the US dollar? – Unlikely!

It may not feel like it, but it’s over. What that means is that having failed to burn down the warehouse for the insurance, the business owners are now left in an even more precarious position of insurmountable liabilities, assuming of course there is no ‘unexpected’ collapse in life expectancy to bail them out from the impending demographic timebomb around the end of this decade!

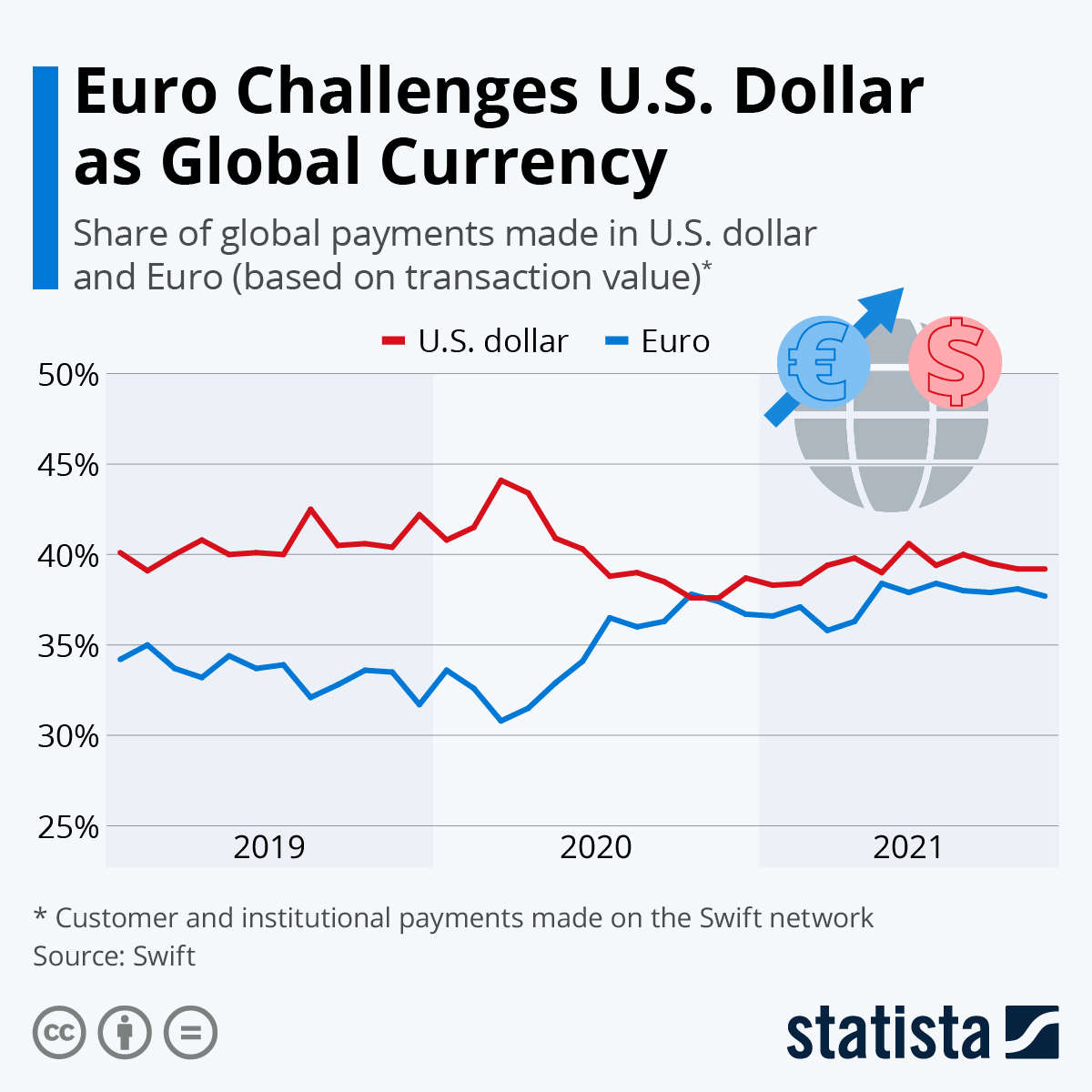

Amongst the various narratives I was reading over the weekend, I was therefore interested to see one reviving possibly the greatest vulnerability for those wishing to maintain US hegemony; that being the role of the US dollar as the World’s reserve currency. Challenge this and fewer buyers of dollars will mean higher funding costs and less scope for debt monetisation by the US Federal Reserve without risking the same thing via devaluation and inflation. For the US, that would be ‘Game Over’. The small article tucked away in Zerohedge titled “Euro Challenges USDollar As Global Currency” was therefore interestingly timed and seemed also to have the fingerprints of Goldman Sachs on it.

USD being displaced by EURO?(Goldman Sachs this week predicted that the Eurozone would grow at a faster pace than the U.S. in 2022, projecting a growth rate of 4.4 percent for European Union currency area and only 3.5 percent for U.S. GDP.)

As if wanting to take up the battle cry for a return to honest financing and a stronger US dollar meanwhile, was Deutsche Bank, which has gone so far as to suggest that the Fed not only stop printing, but actually shrink its balance sheet by as much as $3 trillion (from $9tn to $6tn). One can only assume that they do not expect the fiscal plans of the current crop of crazies in the Democrat Congress ever see light of day and that the mid-term elections return both a fiscally and monetary more conservative majority back to both Houses. This however, would still entail a normalisation in US interest rates and bond yields, albeit perhaps to still manageable levels assuming a firmer dollar also eases some of the current inflationary pressures. Short term, such a threatened tightening would inevitably trigger yet another ‘hissy fit’ by markets in an attempt to test the resolve of the Fed and if it can once again be bounced into returning the punch-bowl. An earthquake under US monetary policy however, would be dwarfed by the tsunami that would ripple out to submerge other over-leveraged economies who have squandered a decade of debt monetisation to buy votes and pursue political agendas rather than resolve their deeper structural deficits. Near the top of that list remains the EU/ECB.

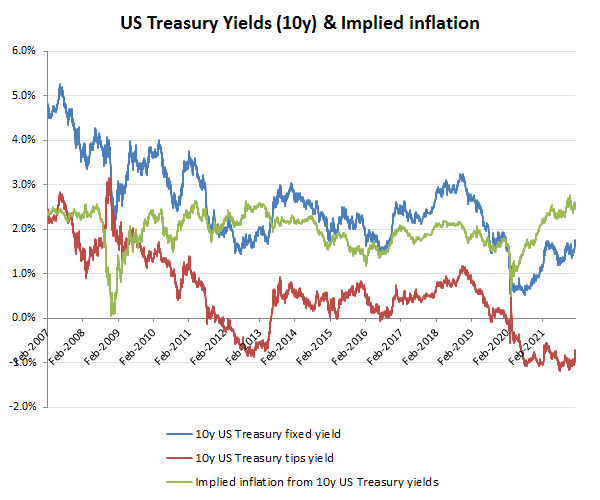

US 10Y rates edging up, but not yet normalised while Fed continues its asset purchases

EU/EURO/ECB caught between a rock and a hard place

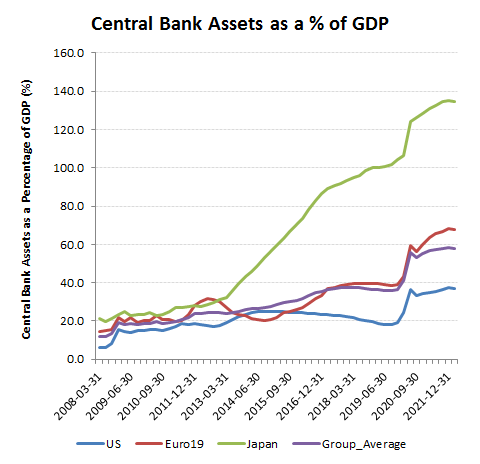

The above scenario, if finessed with some targeted encouragement for private sector investment would also have another significant consequence, that of helping to restore the reserve currency status of the US dollar relative to the Euro. Step back for a moment and consider the potential impact of even a modest normalisation of US interest rates (on a reviving US economy) on Euro rates. With the EU mired in covid social chaos and caught between unresolved structural deficits across its southern flank and a disputed authority to impose the proposed transfer union, what would the ECB do; raise rates and blow up both the EU economies and political agenda? Alternatively, it might keep backstopping local bond issuance by printing and lending cheap Euros to domestic banks, but this would risk seeing these leaking offshore and into higher yielding and faster growth US dollar instruments. In such circumstances, there would be irresistible pressure to impose exchange controls, albeit once this is perceived by markets, the damage will already be done. At present, the EU is not a transfer union and the ECB/EU does not have direct taxation powers to underwrite the issuance of more Euros. Notwithstanding this, the cost of monetising structural deficits amongst its soft underbelly has resulted in an asset build up at the ECB to almost 70% of the Euro area GDP and almost double that of the US Fed’s relative to the US economy. Fracturing political cohesion within the EU as authoritarian administrations abandon the previous ‘free movement’ principals and even the Nuremberg Code, suggest the already heightened civil unrest seen across France, Germany, Austria, Italy and the Netherlands is only going to get worse as these administrations attempt to ‘double down’ on human rights, including coercing citizens to take experimental gene therapies that are neither safe nor effective. Far from displacing the US dollar, the Euro has never been more vulnerable to imploding!

US Fed balance sheet exposure is dwarfed by the ECB’s