Rising US federal debt and maturites pose uncomfortable truths for ‘no/soft’ landing assumptions

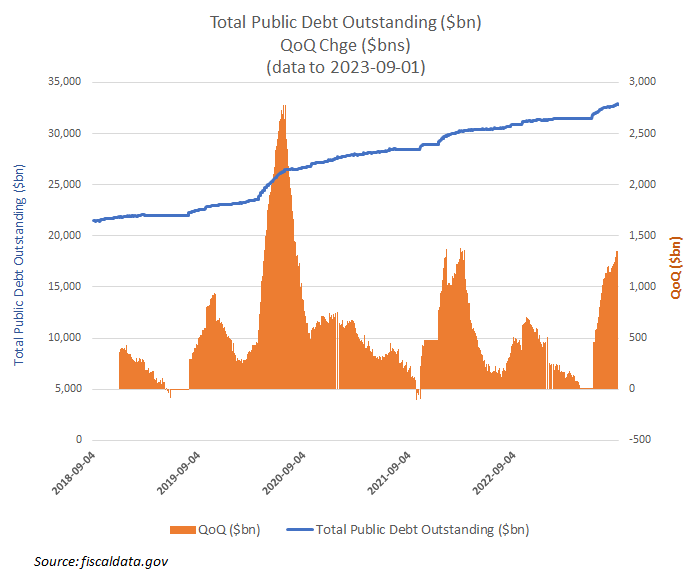

As of the 1st September, US Federal debt was estimated to be nudging $32.6 trillion, having been increasing by approx +$1.4 trillion per quarter following the abandonment of the debt ceiling and the last vestiges of Congressional constraint. Annually, that represents almost $7tn of new debt, which together with a further $7.5tn of existing debt matures and needs renewing, but at prevailing higher rates. Combined, this may require the US Treasury to find buyers for over $14tn of debt this coming year, just as energy prices and inflationary pressures are building again, suggesting an increased interest bill of at least $600bn, representing a headwind of at least -2.2ppts to GDP. Anyone still wants to bet on a no/soft landing?

Debt expanding by approx $1.4tn per quarter!

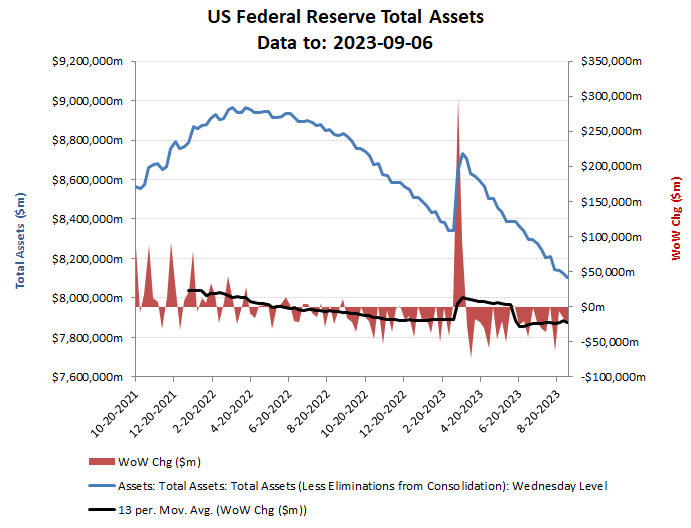

While the US Federal Govt continues to rack up the debt, the US Federal Reserve has returned to its previous tightening plan, after having fallen off the wagon briefly over the SVB/Republic bank bailouts. Over the last quarter, overall Fed assets on its balance sheet have been reduced by approx $290bn and therefore just ahead of its original plan of $95 per month.

US Fed B/S assets reduced by approx $290bn in last quarter

Employing searing analytical skills, the above debt increases of +$1,400bn in the last quarter together with this Fed B/S asset reduction of $290bn adds up to almost +$1.7tn of incremental new debt needed to be raised. Annualised, that’s a run rate of $6.5-7.0tn, which depending on which end of the maturity curve the Fed issues these new treasuries would equate to an additional interest bill of approx $350bn, equivalent to -1.3% of the $27tn of GDP

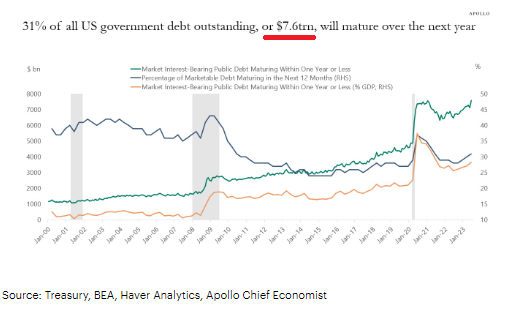

Exacerbating the above dynamics however, is the uncomfortable reality that over 30% of all Federal debt securities will be maturing over the next year, which ApolloAcademy estimates totals around $7.5tn. Given that much of this debt will have been sold on the artificially low rates from QT, rolling these over at between 5.5-4.5% yields (depending on maturities again) could easily add between 3.5-4.5ppts to the annuak funding costs, or an additional $260bn pa, or the equivalent of 1.0% of GDP.

The inevitable implication therefore is that on the current trajectory, rising funding costs on US Federal debt could increase by over $600bn over the next year. Even without the knock-on implications on demand, or funding rates, this suggests a drag to GDP/consumption of at least -220bps.

For those betting on a ‘no’, or ‘soft’ landing for the US economy, they seem to have ignored these uncomfortable realities of having to live within ones means!

$7.5tn of US Federal Debt maturing within 1 Yr