Interpublic Q2 disappoints – the canary in the coal mine?

From the -100bps drop in margins as organic sales growth slowed to only +0.4% for its Q2, IPG clearly didn’t see it coming, particularly following the solid performance in Q1 and the easier prior year comparatives it was cycling against for Q2. This lack of visibility and the uncertain impact of Fed monetary tightening on marketing budgets after 8 years of plenty was enough to spook markets into slicing 13% from the share price notwithstanding attempts by management to hold full year margin guidance.

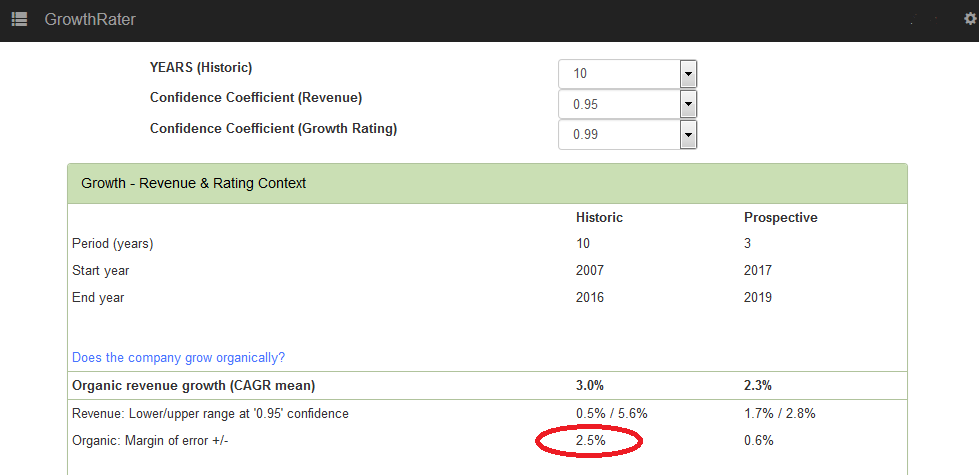

It’s not too hard to see why. The management may still seek to deliver organic revenue growth at the lower end of its +3-5% guidance range for the FY17, which also happens to be the group’s trailing 10 year average rate, but our GrowthRater volatility analysis highlights a margin of error on this of plus/minus 2.5ppts, even when excluding the 5% of outliers ( a 0.95 confidence coefficient). With the Fed and then ECB blowing hot and cold on monetary policy in Q2, it is perhaps unsurprising agency clients held back on marketing expenditure or that investors identify a heavy negative weighting to that forecast risk.

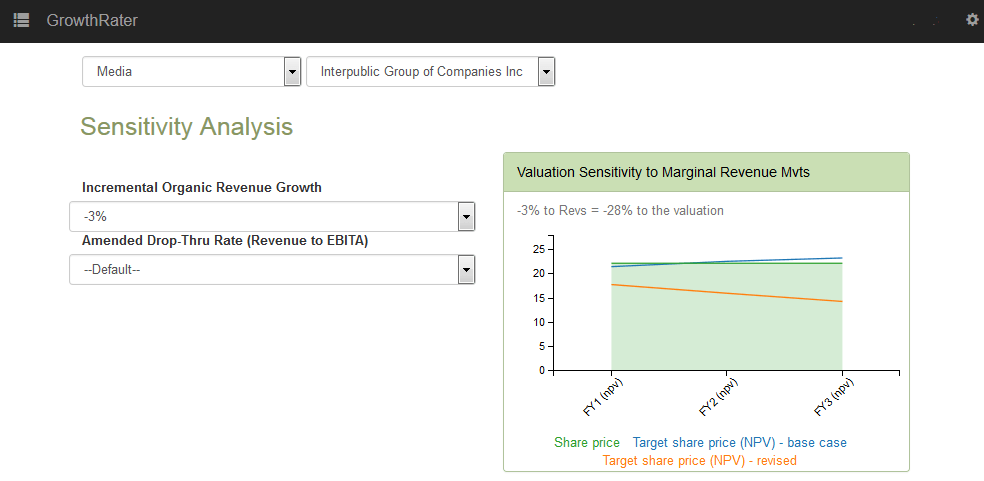

If this is it and the music is stopping ahead of further rate increases and slowing economic growth should US healthcare and tax reforms remain mired in Russia/Trump gridlock, then one might want to remodel the valuation for the lower revenue outcome. Plugging in a -3ppts reduction in projected organic revenue growth against my base case assumptions and shares could be down by the best part of 30%; and this relative to the market, which in these circumstances would also be under pressure.

The cyclical relationship between the broader economy (personal consumption and corporate profits) to Advertising expenditure is well known, albeit as with other parts of the economy, the additional distortion of coming off cheap money can only be guessed at.

We all know that cheap money makes for flawed investment decisions. It has also probably been responsible for providing an additional stimulus to marketing investment and other areas with a short-term payback, given that QE was never originally expected to have a long shelf life. So instead of committing to longer term liabilities, companies have been incentivised to outsource these (often overseas), while reallocating capital to marketing and share buybacks. Notwithstanding the grand claims of improved marketing efficiency of digital, improved marginal returns from increasing the advertising budget can also come from the other end; lowering the funding costs! Is it just coincidence that the current squeeze on budgets and agency fees by groups such as Unilever has occurred once the central bank narrative has reversed?

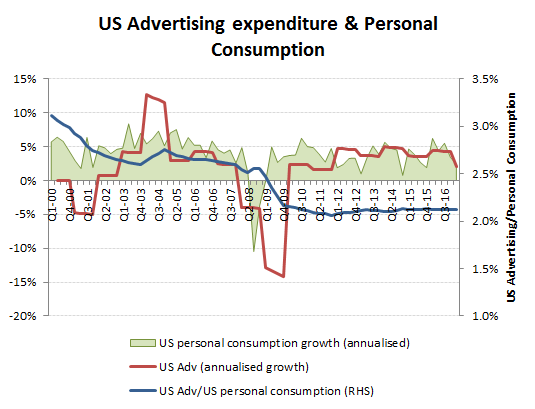

A feature that may have been overlooked in the above chart on US Advertising and Agency US organic revenue growth, is not so much that Agency fees continue to lag client media spend, but that media spend has not declined relative to GDP. The same is true when also comparing US advertising spend to US personal consumption. Unlike during the previous cycle, advertising costs have not fallen as a percentage of consumption. Given the shift in media consumption and marketing budgets to online/mobile where accountability and marketing efficiency is claimed to be better than on analogue, this might come as a surprise as it suggests marketeers are not getting any more bangs (in terms of sales) for their bucks from this transition. While this may in part reflect an element of displacement of effective marketing investment included in other cost buckets such as property, which need to be replaced as transactions move online, it still raises a concern as to the sensitivity of budgets to be cut into a less favourable interest rate environment. It also raises the thorny and unresolved subject of advertising effectiveness. Alphabet may be offsetting lower price per clicks with increased clicks, but this may just reflect the diminishing ROI per click. If advertising expenditure has been goosed up by cheap money, but has failed to deliver any overall improvement in ROI and marketers and investors remain substantially blind as to the real value proposition being sold by media, this is an area where budgets are looking increasingly vulnerable. Central bankers may have tried to eliminate the business cycle, but in this case might have just deferred it while lulling investors into a false sense of security. Definitely time to start modelling the downside revenue risk for your portfolio stocks on the GrowthRater sensitivity analysis.