End of cycle warnings for marketing services

How many leading marketers know what return they’re getting on their marketing investment?

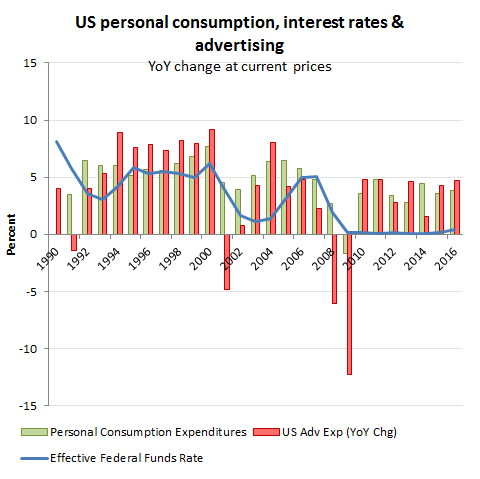

From P&G marketing honcho, Marc Pritchard’s gripes about poor transparency and accountability and a “crappy media chain”, one might surmise not many. If you can’t trust the data on who is being reached, any resulting ROI calculation derived from it is therefore unlikely to be particularly reliable and if P&G is struggling on this, what hope is there for the rest of us. From the broader macro data data meanwhile, one might arrive at an uncomfortable conclusion. If digital marketing was so effective, why is it that notwithstanding a shift in budgets into digital and a near zero interest rate environment, has US personal consumption failed to outpace the average growth in advertising expenditure over the last five years? That’s right, US advertising budgets are no more efficient in generating incremental sales and returns and marketers aren’t much the wiser as to why, albeit are a bit angrier.

http://adage.com/article/media/p-g-s-pritchard-calls-digital-grow-up-new-rules/307742/

So far, none of this seems to have hurt the big digital platform owners, where revenue growth continued to surge into the end of last year on cheap money and a click-storm of new inventory. This however doesn’t mean that there isn’t cause for serious concern for the future. Alter the macro dynamics for consumption or interest rates and very quickly, any marketing expenditure that can’t be justified on an ROI basis may get chucked overboard. Prodded by Kraft Heinz’s approach, Unilever has already announced what looks to be an almost -15% reduction in its marketing budgets over the next three years, which it thinks it can do without denting its top line growth targets. As these alpha marketers cut marketing budgets and more fmcg groups adopt zero based budgeting in response to the continued threat of Kraft Heinz, one may well ask where this leaves agency forecasts for marketing expenditure in 2017 or the consensus forecasts for agency earnings which depend on these.

If marketers are already starting to cut budgets in response to poor rates of overall returns on marketing investment and problems in measuring specific effectiveness, that makes me worried about the downside risk to forecasts. For all the leading forecasters, 2017 is expected to be ‘business as usual’, with expectations for global advertising expenditure growth ranging from Carat’s Sept 2016 forecast of +4.0% to the more recent estimates of +4.4% from GroupM and Zenith. Consensus estimates for the agency groups broadly reflect this ‘steady as she goes’ narrative, although noticeably, stock prices are wisely beginning to discount outcomes beneath these, given the invariable ability of the sector to recognise a reversal in the marketing cycle only once already pitched over the edge.

Marketing budget sensitivity to interest rates

We are in unexplored territory on this one, as the previous two interest/economic cycles had similar characteristics initially, but ended differently. A short-lived cut in interest rates reflated consumption and advertising budgets quickly after steep falls in both occasions. In the first of these (1993-2000) and perhaps reflecting the economy coming off a lower base of household indebtedness, consumption and advertising spend sustained over eight years of robust growth, notwithstanding interest rates returning to above 5% for most of the period. In the mid-noughties however, a similar attempt to normalise rates back up to these levels precipitated the now well aired sub-prime defaults. For both cycles though, the key determinant to marketing budgets was the overall macro cycle rather than interest rates in themselves, although this may not necessarily be the case this time.

The key difference of course was that the rate reductions in the previous cycles were barely noticeable before they were reversed, while since 2009, financial repression has become a commercial way of life. An artificially low rate environment however is a negative signal to markets about the health of demand which deters investments with long paybacks and liabilities (such as domestic capacity build and employment), while skewing capital allocation into areas with a quick payback which can take advantage of the increased marginal returns from crushing the cost of borrowed capital. For those wishing to understand why US advertising has raced ahead of consumption at a time when marketing budgets are being re-allocated and into supposedly more efficient digital platforms may need to look no further. Unfortunately, the reverse may also apply as rates rise.

What if

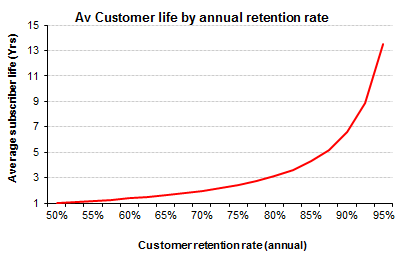

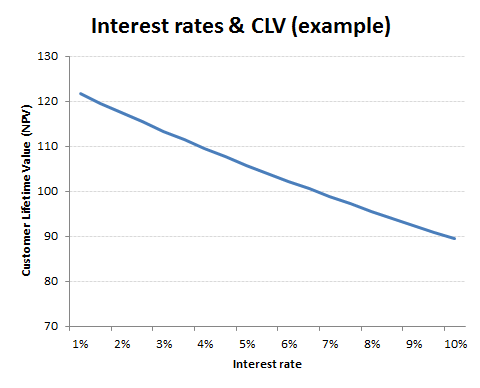

By way of an example, let’s make up a fictional campaign for a brand from the perspective of a customer. Crudely this is just the customer acquisition costs (CAC) relative to customer lifetime value (CLV), which is can be either gross or net profit generated from them while they remain as customers. As one can see from the chart below, average customer lives can be quite sensitive to retention rates and can vary considerably by product category. One might need a short payback for items such as nappies, but a new Marmite customer may provide repeat business for decades.

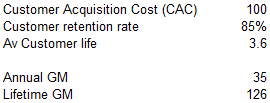

For my hypothetical example I am assuming a customer with an 85% retention rate and therefore average life of 3.6 years, with a lifetime gross profit of 126 assuming this at 35 pa. Against this, the customer acquisition cost is 100.

Customer acquisition and CLV assumptions (fictional example)

In this example, the company is making a net return of 26 for every new customer (126-100). The investment of 100 required to acquire the customer has a capital cost, which if borrowed will reflect the average interest rate and the payback period. What is important for the company in determining how much to spend on its customer acquisition will include the required marginal return and therefore also the cost of capital (interest rates).

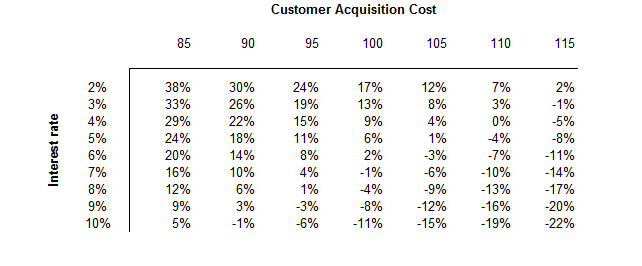

Marginal returns by customer acquisition cost and interest rate assumptions

What that means is the higher the interest rate, the less a company will be prepared to spend on acquiring that customer. While the assumptions in this example are fictional, the principal holds and offers an indication of the possible impact to marketing budgets from a normalisation in interest rates.

Marketing expenditure is sensitive to interest rates