ENIRO AB – Sometimes a negative valuation in the GrowthRater is justified!

ENIRO AB

Friday’s announcement warning that no agreement had been reached by the 31 March Deadline with the banks has been followed by this morning’s refinancing proposals where Convertible and Preference shareholders have basically the stark choice of agreeing to exchanging their rights for just common stock and then stumping up more cash in a rights issue or face annihilation. Shareholders have until the EGM on the 9th May to decide or otherwise “the company will not be able to meet its loan commitments. The Board intends then to the district court to apply for reorganization, which most likely would result total loss of the Company’s common shareholders, preference shareholders and convertible holders.”

http://www.enirogroup.com/en/press-releases/no-agreement-for-eniro-with-the-banks

http://www.enirogroup.com/sv/pressmeddelanden/eniro-presenterar-plan-for-rekapitalisering (still not out in English, but Google translate works quite well)

- Eniro’s been a basket case for years, so this probably won’t come as too much of a surprise, although is a reminder of Modigliani’s premise that debt should carry a risk premium

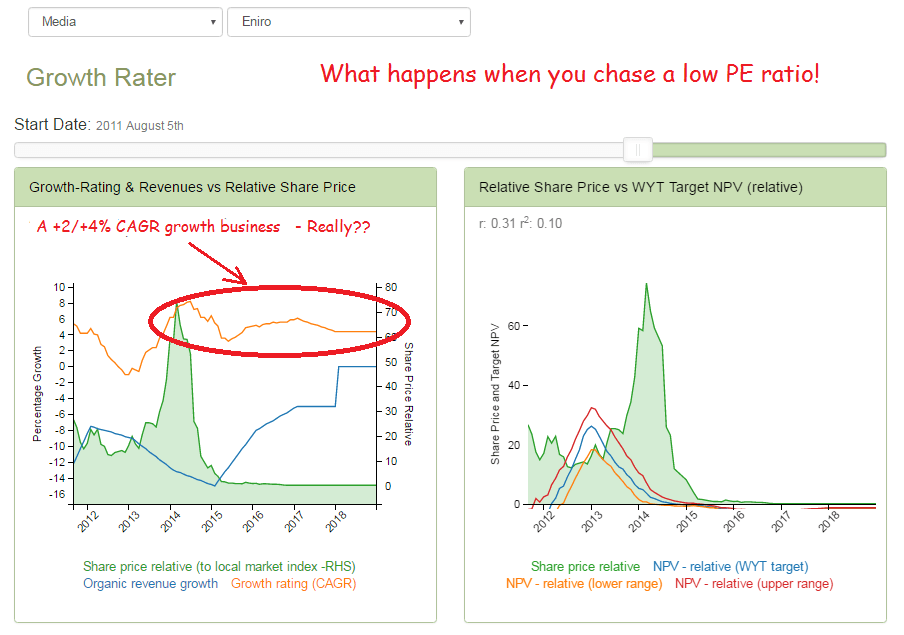

- For those enamoured with the low PE rating at Johnston Press ought to take note (see update on the webApp: https://app.growthrater.com/)

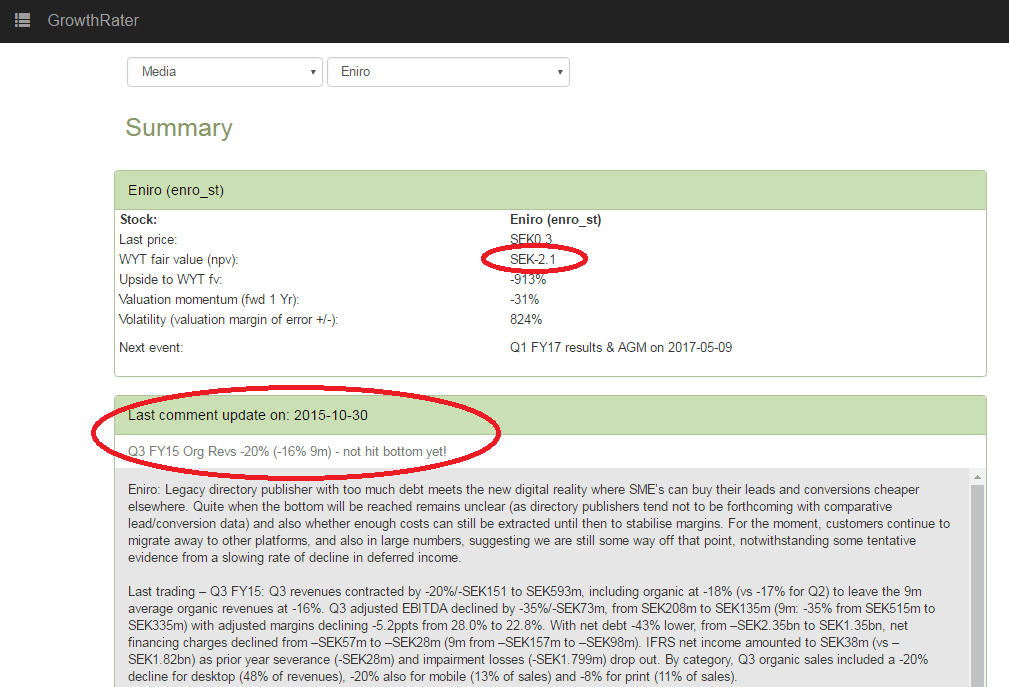

Below is a screenshot of the summary page from the WebApp: There’s not been much cause to update the comment for some time now!