Gold returns

Was it the flip-flopping Federal reserve or Draghi’s increasingly desperate attempts to reflate the ECB debt balloon, but with Iran scare stories it has done wonders for the gold price. While forthcoming Q2 results will be pretty drab for the industry, with H1 average prices broadly flat YoY, the second half is on track for a rise of around +17% YoY, if the current price of $1,419/Oz manages to hold. All this of course could go horribly wrong for the gold bugs should peace break out and the US and China appear closer to a trade accord following the meetings at this Friday’s G20 in Japan.

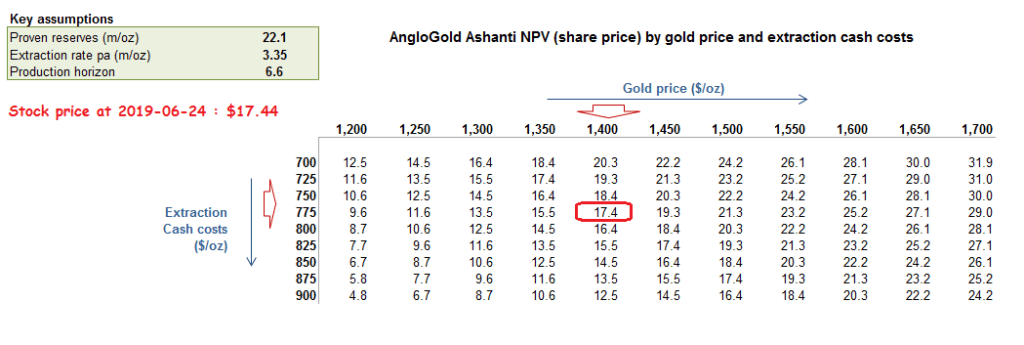

For those wishing to take a directional punt on whether to start hoarding gold or cans of beans, you might be interested in how markets have been valuing these gold producers. Discount the proven reserves at the current extraction rates, cash costs and against the current gold price and you’ll find that the share prices closely track the NPV valuations. While this isn’t going to answer that thorny question of where the gold price goes next, it ought be of passing interest for shareholders to be able to anticipate the operational leverage that the gold price may have on the share price of their favoured gold producer.

In the below table I have included a share price matrix by Gold price and cash extraction costs for AngloGold Ashanti, in part because it is NOT my favoured play on the sector given the political instability in South Africa. Clearly my sensibilities are not shared by markets who remain happy to discount the valuation it seems on a US market cost of capital. For comparable valuation analysis of other more stable gold producers, please contact us here at the GrowthRater for more details on how to subscribe.