November US non-farm payrolls – a positive mix for equities

Improving trend in real private sector employment

On balance, November’s non-farm payroll numbers were as good as might have been hoped for, at least for equities. Whilst the progress of the tax reforms, which offer to drop Federal corporation tax rates by 15ppts (from 35% to only 20%) are clearly more relevant to both valuations and FCF assumptions, the improved rate of annualised private sector income growth based on overall employment growth and hours worked, rather than underlying wage inflation, offers to sustain personal consumption without exacerbating the pace of monetary tightening. The key points, within the monthly payroll data include:

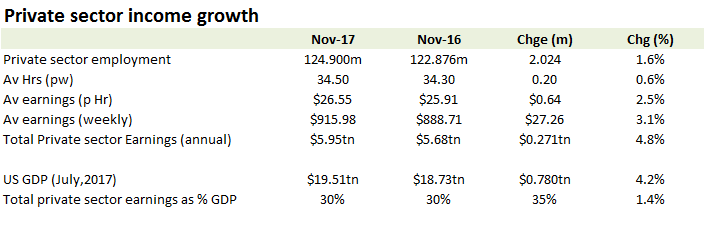

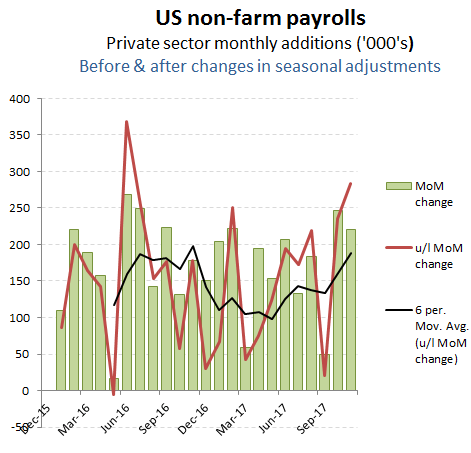

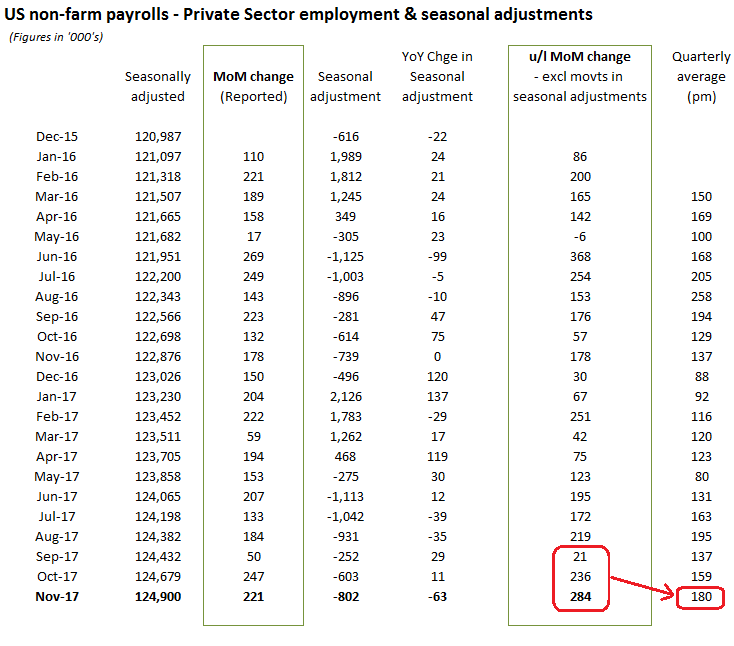

- A reported +221k MoM increase for private sector employment reflected a +284k increase excluding the -63k reduction in seasonal adjustments. On an unadjusted basis, this represents another consecutive improvement following the hurricane impacted September (of only +21k – unadj) and October’s +236k increase. This represents an trailing quarterly average monthly job growth of +180k, which is also now broadly comparable the the trailing 6 month average of +188k pm. While this is not far adrift from the average rate inherited by Trump when he was elected, it does mark an improving trend following the post inauguration dip (see chart below).

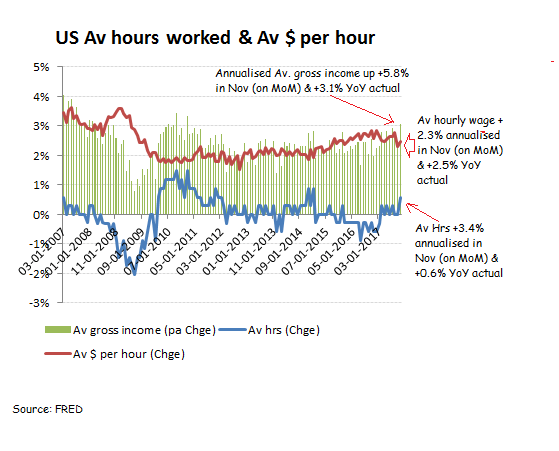

- Average gross income in November is up +5.8% on an annualised basis and +3.1% on an actual YoY basis. While annualised hourly wage growth of +2.3% is slightly down on the YoY rate of +2.5%, this was more than compensated for by a +3.4% rise in annualised hours worked, versus an actual YoY increase of just +0.6%.

- Folding the +5.8% increase in average annualised gross income through the +1.6% YoY increase in actual private sector employment suggests an annualised increase in total private sector income for November of around +7.4%; albeit a more modest +4.8% on an actual YoY basis. This represents a positive support for overall levels of private consumption ahead of Christmas, but without suggesting a dangerous rise in wage inflation to warrant a more aggressive pace of monetary tightening.