A very odd recession!

Oh what a wonderful recession it is. Perhaps this is just the Sitzkreig before the real impacts are felt, but for now the stats from US employment data has yet to support the widespread news narrative of layoffs as the BLS reports US net private sector job growth approaching +400k in January. Maybe the fear quotient has been dialled down by a resilient equity market and the collapse in Natural Gas prices into a warm early winter and consumer resistance to the previously manipulated surge. Either way, this presents a dilemma for the US Federal Reserve in that an overheating labour market will place additional pressure on core inflationary expectations, notwithstanding the easing reported rates from the NatGas price fall. One misstep over Ukraine, with Russia amassing 600k troops for its next push and the mood could change rapidly. So is this a repeat of the mid 1970’s and Arthur Burn’s preemptive and damaging decision to take the Fed’s foot off the brakes, only for Volker to have to subsequently and painfully jam them back on again?

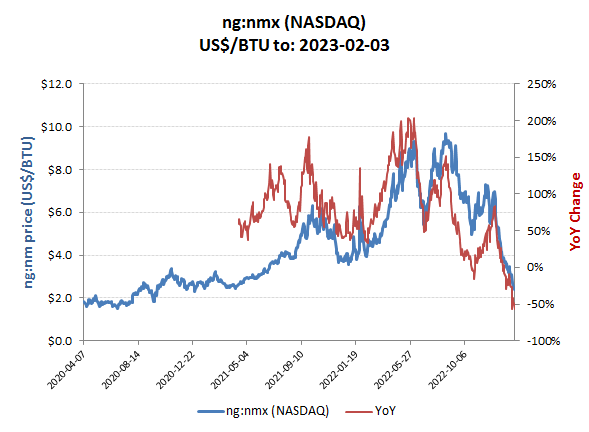

Having trebled in price over European supply concerns and the green agenda, US NatGas prices are now back down to below where they started, notwithstanding all attempts to ban alternatives. Whether this actually translates into consumer’s energy bills however, is another matter as monopolist suppliers and captured regulators will not doubt ensure consumers get price gouged on the previous price peaks, rather than the now prevailing levels. Come March/April, when the Q1 bills start being received, watch out for the next pandemic, that being bill shock!

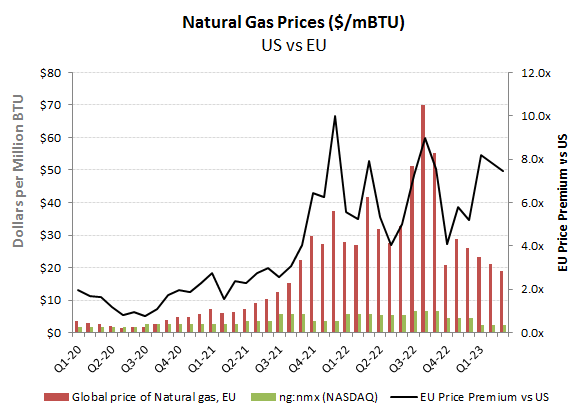

Oops, now that wasn’t supposed to happen!As an aside and perhaps not entirely relevant to this, is reflected also on what is going on in European NatGas markets. Here, as can be seen from the below chart, prices have also been falling rapidly from their peaks, by less than for the US price, notwithstanding the filtering off of some of the US supply into Europe as LNG capacity is ramped up. So for these European manufacturers, and in particularly in basic chemicals, we have an absolute gain, but more importantly not a relative one versus their US competitors.

European NatGas prices are also falling, but not as fast as in US

So back to the US employment data. As can be seen from the below chart on private sector net monthly job formation from the BLS estimates, January saw an underlying net growth of almost +400k net jobs, which has been enough to stabalise the 6 month trailing average. Those tracking the relationship between job formation and economic growth in the US over the last 3 or 4 recessions, will understand that growth of this magnitude is not consistent with your normal recession. For the US Fed meanwhile it removes the restraint on one of its two mandates, that being to secure full employment while putting additional pressure to ratchet down on its other mandate, inflation. So while these January employment numbers seem good for the economy, they may be less so for markets and financial asset prices by encouraging the Fed to continue normalising interest rates and avoid a secondary infection on inflation.

Well, that was unexpected!

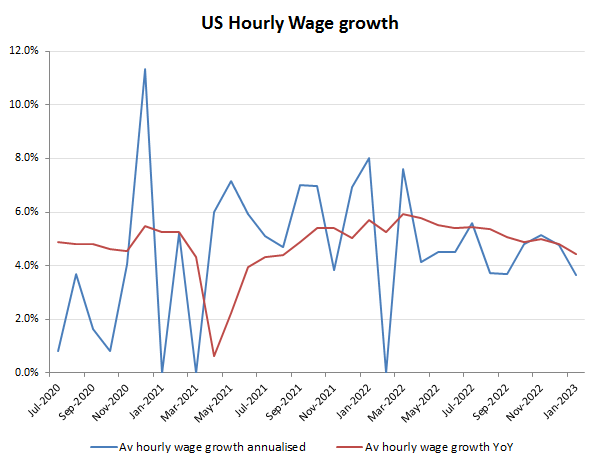

One possible relief for the Fed from the January BLS estimates, was the relatively muted increase in average wages, although how confident one can be with these as a guide for what’s coming down the pipeline is another matter.

Inflationary wage spiral? – Not in this data – (yet?)

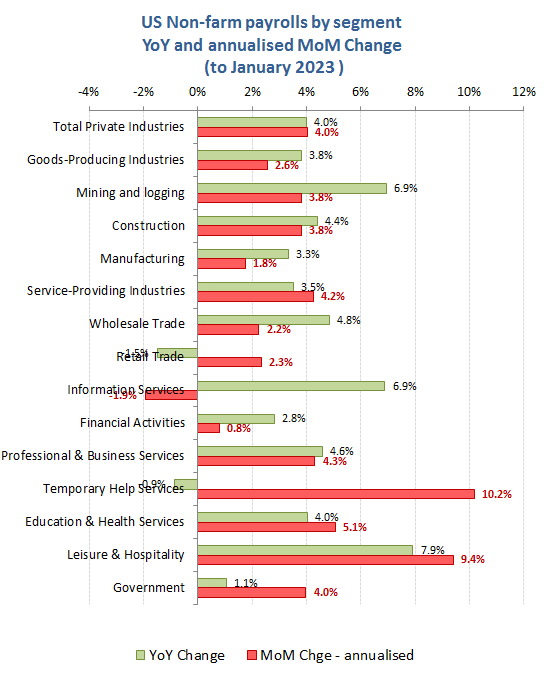

One possible explanation of the modest advance in average wages could be due to where the job growth was coming from. From the below chart, one can see traditionally low wage ‘Temporary Help’ and ‘Leisure & Hospitality’ categories growing fastest, while the premium income areas such as in Info Tech and Finance have struggled.

MoM net job adds were broadly based, but focused on the lower income categories

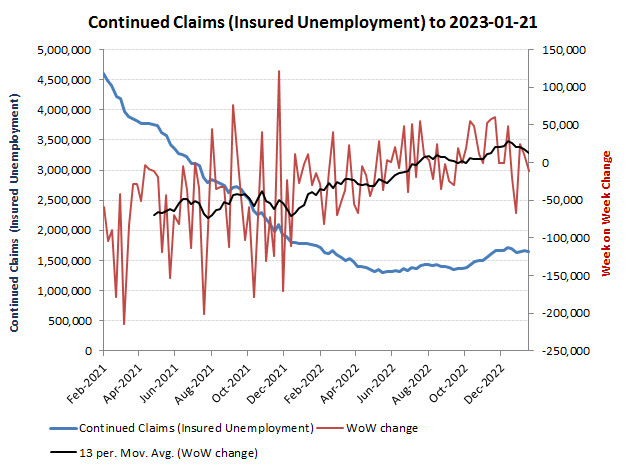

As the BLS NFP numbers are qualitative survey derived estimates and often subject to substantial subsequent revisions, I always like to cross check these with the more quantitative Weekly insured unemployment claims data. For once, these seem to reconcile with the NFP narrative, with the most recent insurance claims data supporting a picture of falling claims and therefore positive net job growth.

Weekly insured unemployment seems to support the BLS NFP estimates, for once!

Does this look like recession?