Wazzup – 23rd May 2017

Chemicals day at Wazzup. – Yesterday’s $14bn merger announcement between Huntsman and Clariant show that it can be done, notwithstanding Akzo Nobel still playing ‘hard to get’ in face of PPG’s multiple advances. With the sector also at the cusp of pushing through price rises to recoup earlier increases in raw material and energy costs, expect a pick-up in the rate of organic revenue growth into the latter half of the year; a feature usually reflected in a rising GrowthRating and stock outperformance. With today’s Chemical Activity Barometer for May posting further gains, both month-on-month (+0.2%) and year-on-year (+4.1%) I revisit the sector, with full updates available in the GrowthRater Analytics section.

- Akzo Nobel (akza_as): Akzo management may escape this time, but the Genie is out!

- PPG (ppg): Running out of time on Akzo bid, albeit perhaps not such a bad thing

- ACC Chemical Activity Barometer: Positive pricing expectations and inventory

- Eastman Chemical (EMN): How relative share price responds to the relative price of growth

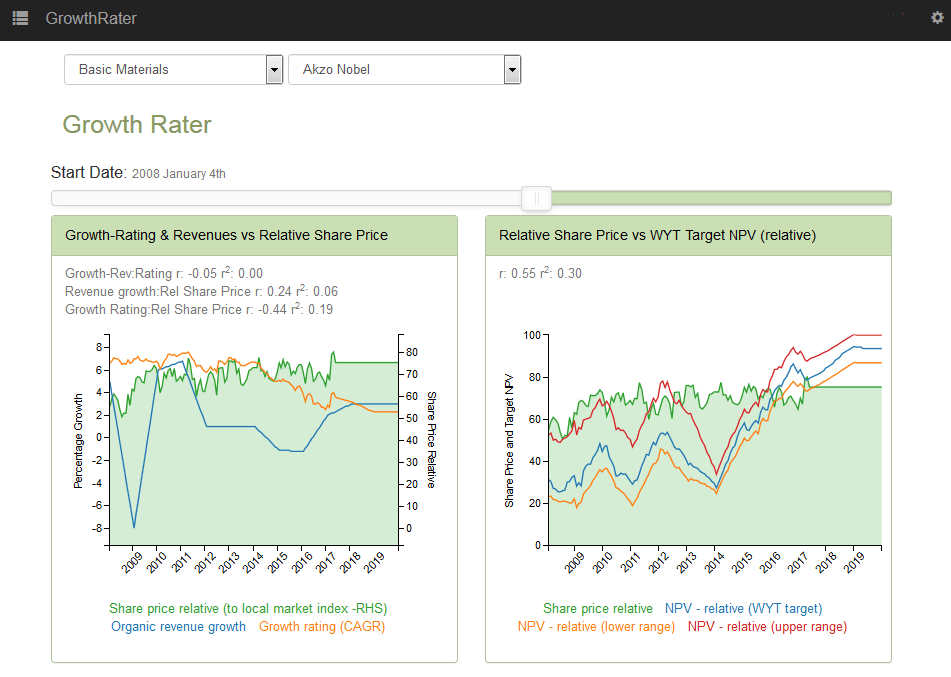

Akzo Nobel (akza_as): Akzo management may escape this time, but the Genie is out!

With Akzo shares standing at a 20% discount to PPG’s last (informal) offer, markets don’t seem too hopeful that activist shareholder Elliott will be successful in petitioning the courts and Dutch market regulator AFM, to force a vote and breach Dutch takeover defences. With the PPG offer already looking fairly full (see below), the issue therefore is whether this will be another re-run of Kraft-Heinz/Unilever or Fox/Time Warner. In both cases, the quarry escaped, but then found renewed vigour in managing costs and discarding peripheral operations, which ultimately meant the initial share price pull-back as these offers failed provided an attractive entry point. At around €75 ps, Akzo’s prospective OpFCF yield of just over 5% and implied GrowthRating of approx +4% CAGR is still short of its current organic top line growth, although not so far adrift that a few adroit corporate divestments and additional costs savings couldn’t bridge.

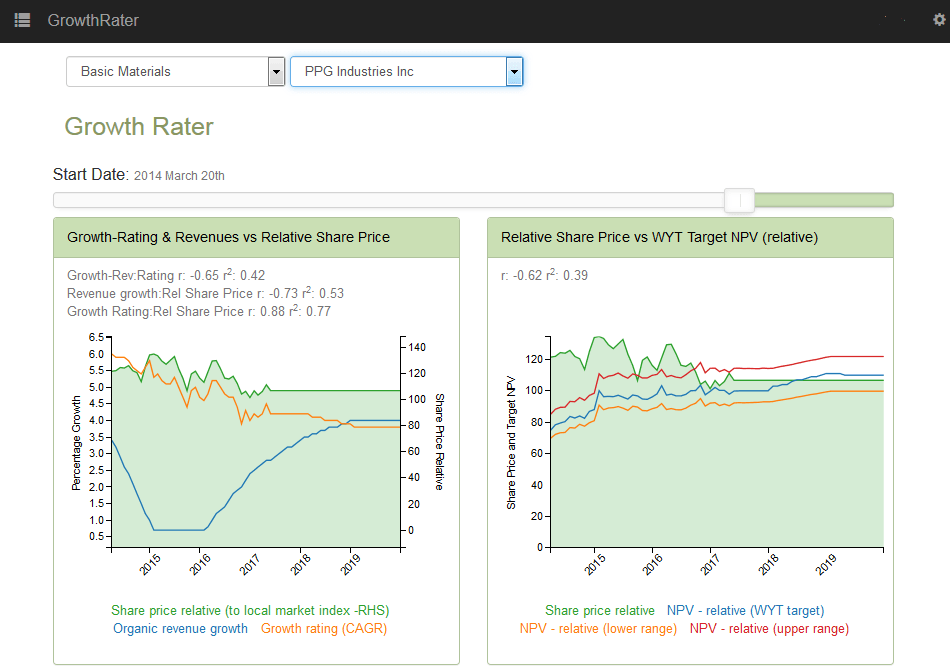

PPG (ppg): Running out of time on Akzo bid, albeit perhaps not such a bad thing

Full marks to PPG’s CEO Michael McGarry’s persistence in pursuing Akzo Nobel, having already been rejected three times. With the informal offer already up at €97.6 per Akzo (and €26.9bn), it is noticeable however that it is activist shareholders at the Akzo end that are petitioning most strongly to see this bid concluded, rather than from the PPG equity base. With Akzo possibly worth €80-90ps, assuming a generous GrowthRating of +4% CAGR and an even split of the $750m pa of planned cost synergies of maybe another €9 ps, this is perhaps unsurprising. With PPG management running out of time to make a formal offer (vs a 1st June deadline), this round looks set to go to Akzo management, which from the current Akzo share price of under €80ps, seems to be largely discounted by markets. For PPG shareholders this might prove to be a lucky escape should the slowdown in US auto markets prove to be infectious and remove one of the more dynamic growth drivers in the coatings market this cycle. In the meantime, that leaves PPG with its powder dry for other opportunities, albeit still struggling to deliver the >+4% organic sales growth to match the current implied GrowthRating.

ACC Chemical Activity Barometer: Positive pricing expectations and inventory

On an unadjusted basis the CAB climbed 0.2 percent in May. On a year-over-year basis, the unadjusted CAB is up 4.1 percent, an improvement over one year ago, but easing from first quarter comparisons. This “easing” however is large part a function of sector share price declines, which is one of the four components that make up the CAB index. While “Production-related indicators were mixed”, the remaining categories of “Input and product prices were rising and inventory and other downstream indicators remained positive.” Overall then, not a bad result, particularly if confirming end user price rises are sticking. If the relevance of this index to sector revenues were needed, then the below chart overlaying Eastman Chemical’s organic revenue growth should help resolve that question.

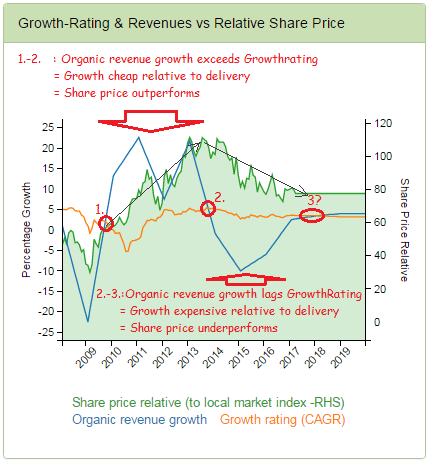

Eastman Chemical (EMN): How relative share price responds to the relative price of growth

And if you need to know what happens to the relative share price when organic revenues grow faster than the growth being priced into the equity, then take a look below at the GrowthRater analysis on Eastman over the last decade.

What is an equity, if not a participation in a cash flow stream where the yield can be determined by the prospective growth?

The message is simple – BUY growth when it is cheap relative to organic revenue growth delivery and SELL when it is expensive

Buy growth when it’s cheap relative to delivery and vice versa