Wazzup – 7th June

Agency AGM trading statements continue to provide mixed signals on trading into early 2017 .

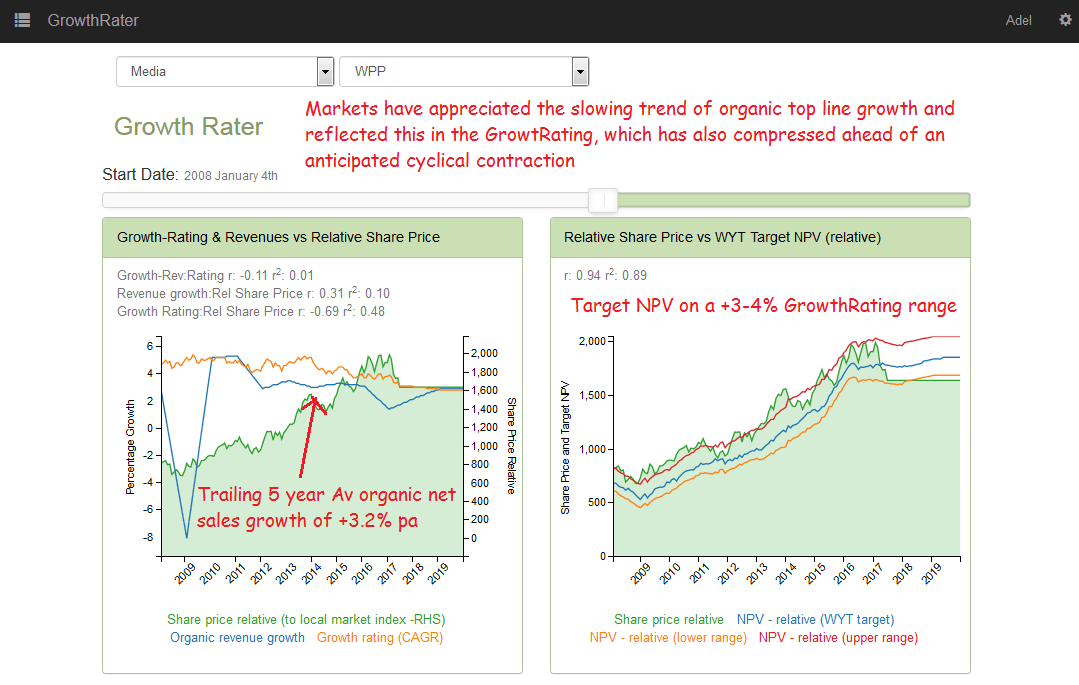

- WPP – April organic net sales growth remains below +1%, notwithstanding the late Easter and election effect .

- M&C Saatchi – “2017 has started well” .

WPP AGM trading update – little to get excited about on trading, albeit reflected by rating

AGM IMS (1-4 months): Organic net sales growth of +0.7% was broadly unchanged on Q1’s similar rate, although reflecting a stronger performance out of the UK and APAC to offset an easing in growth from Cont Europe and a further deterioration in N. America. By category, improvements across Media were offset by deteriorations across the remaining disciplines. The Group declares that revenues, net sales and profits are ahead of Q1’s revised budgets and last year. However, the lack of progress into Q2 and the reliance on the UK, which may struggle over the remainder of Q2 with the Election, forthcoming Brexit negotiations and terrorist attacks, suggests FY17 forecasting risk probably remains negative. – unlike the US, in the UK, General Elections tend to bring forwards advertising expenditure to avoid the immediate run up to the vote (a function of restrictions on Govt spend as well as marketeers trying to avoid the distracting political noise).

AGM IMS – the numbers for months 1-4:

- Revenues: +15.9% to £4,846m, incl organic of +0.7% (Q1: +0.2%), fx of +12.5% and acqs of +2.7%

- Net sales: +0.7% organic (Q1: +0.8%, implying approx +0.5% for April)

- o/w Advertising: Approx +0.1% (Q1: -0.3%, implying approx +1.2% for April)

- Consumer Insight: -1.6% (Q1: -0.8%, implying approx -3.8% for April)

- Public Relations: +3.2% (Q1: +3.9%, implying approx +1.7% for April)

- Specialist Comms: +2.0% (Q1: +2.2%, implying approx +1.6% for April)

- America: -1.6% (Q1: -1.1%, implying approx -3.1% for April)

- UK: +5.1% (Q1: +3.7%, implying approx +9.3% for April!)

- Cont Europe: +3.0% (Q1: +4.3%, implying approx +2.3% for April)

- RoW: +0.5% (Q1: -0.1%, implying approx +2.3% for April)

Markets bracing for another cyclical downturn

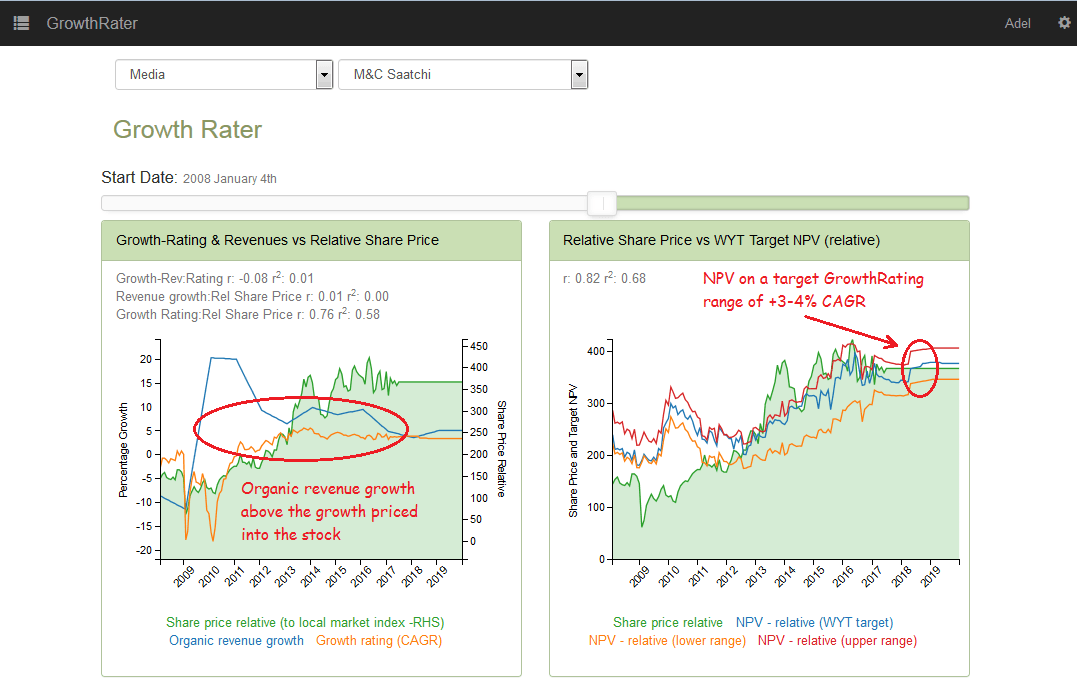

M&C Saatchi – “2017 has started well” .

Last trading update – AGM IMS:

- “2017 has started well and trading is in line with expectations.”

- “In terms of New Business, group companies have made a good start”

- A/C wins incl Pacific Life (LA), Haribo (Fr), Dreams/Visit Britain/Body Shop (UK)

- “”All of this gives the Board confidence of another successful year for the company.”

With its upbeat AGM trading statement today, it seems that not all marketing services agencies are struggling into 2017, although M&C Saatchi has been running ahead of the herd for the last few year as it extends its geographical footprint.

Trading on a prospective Op FCF yield of approx 5.5%, the stock’s discounting growth at around +3.5-4.0% CAGR. That puts the GrowthRating near the upper end of the valuation range for the sector and while this growth discount is still looking to be below what it’s delivering in terms of organic revenue growth, the above weighting and exposure to the UK dulls my enthusiasm this side of the Election and Brexit negotiations.

For M&C, my main issues relate to

How long it can continue out-grow the industry in the face of its exposure to a possible further erosion in UK Ad spend over Brexit (and maybe not helped by tomorrow’s election outcome) as well as its limited scale to invest in digital media tools

Minority put options. As many of these are fixed, the liability may be more than just an accounting nicety and reflect a real potential cost to shareholders, particularly if Ad markets turn south. At least they didn’t issue convertibles as back in the late 1980’s at S&S. My valuation takes 50% of the provision, which equates to approx -20p per share from the valuations below.

Cash conversion: They’ve been quite liberal in shifting charges below the adjusted line which has carried a real cash cost and which has been a drag on their conversion on net income to FCF (adj for mins of course). My valuation normalises the conversion to 85%, which perhaps errs on the ambitious relative to the historic performance.

For the full analysis please check out the WebApp.

So far so good

.