Airlines – back to the old ‘normal’

Manipulating monetary conditions leads to bad investment decisions as we have seen with the airline industry. 18 months ago its principal trade body IATA was waxing lyrical about the industry, as were financial pundits. Unfortunately, they underestimated the impact that low funding costs would also have on margins and profits in a capital intensive industry where excess marginal ROIC would simply get competed away.

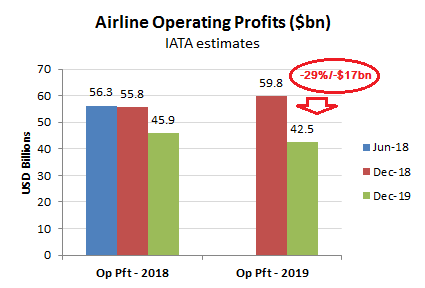

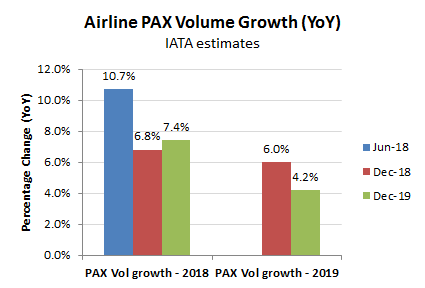

So 18 months after our warning (“Normal profits are becoming normal for airlines” – be afraid) and a follow-up blog in January (Airlines – what happens when ROIC looks too good), the IATA have now just released their latest estimates, which reveal a -29%/-$17bn cut in their 2019 industry operating profit forecast, including a -170bps drop in margin expectations. While they may point to global trade war concerns, this is not reflected in passenger volumes, where expected growth remains relatively buoyant at a predicted +4.2% for 2019. The problem however, has been that too much cheap cash has encouraged the industry to build up too much capacity, which given the high marginal profitability inherent in the commercial model has meant that yields have been sacrificed. As margins, and more importantly ROIC are compressed, there will be an inevitable polarisation in access to cheap capital, which will squeeze out the less competitive airlines and thereby stabilise returns for the remainder. The cut in capacity growth from an originally expected +5.1% for 2019 to a current estimate of +3.0% may provide some initial evidence of this process notwithstanding this probably has more to do with delays surrounding the 737 Max, rather than any underlying restoration of self-restraint by the industry.

As its dull to grind through verbiage, I have included these points in a series of charts that include IATA key forecasts for 2018 and 2019 made in June 2018, December 2018 and yesterdays December 2019 estimates.

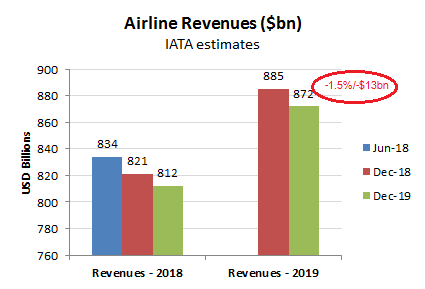

Revenues

2019 industry revenue estimates have been trimmed by -1.5%/-$13bn since last year’s IATA forecasts

Operating Profits

The compression in expected industry operating profits however has exceeded the revenue shortfall, notwithstanding oil price forecast remain at $65bbl (brent)

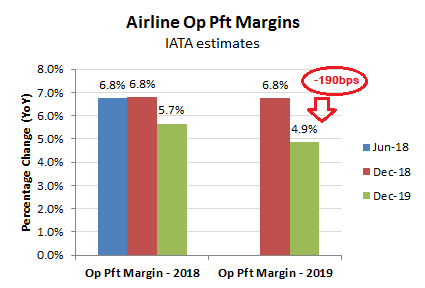

Operating Margins

In terms of expected operating margins, this represents a compression of almost 200bps from what was anticipated only a year ago.

Passenger Volumes

The growth in PAX volumes is less than originally predicted (at +4.2% vs +6.0%), but not significantly so.

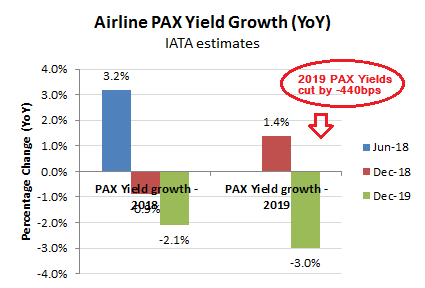

PAX Yields

The problem has been with yields (which have collapsed by approx -440bps vs last year’s forecasts) and the industry’s pricing power. The level of decline relative to volume demand however, suggests specific competitive dynamics are at work rather than the purported macro headwinds

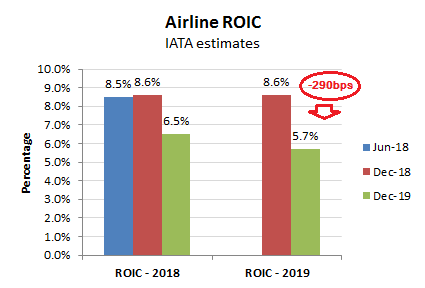

ROIC

With passenger volumes growing at over +5% pa and banks offering cheap cash, it is very tempting to lower you return thresholds to reflect short term funding costs rather than a longer term cost of capital. For capital intensive industries such as airlines (and telecoms), this is where the tail can wag the dog, with marginal returns over these artificially low funding rates bid away to secure a competitive advantage.

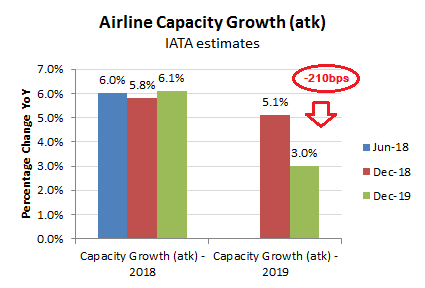

Capacity

So with industry ROIC heading back down towards 5% and passenger volumes now expected to growth at a more modest +4%, does this mean some sanity is returning to asset allocation decisions? With projected capacity growth of only +3% for 2019 trailing demand, that might be an interpretation, albeit this probably has more to do with the delays on the 737 max deliveries, with capacity growth for 2020 forecast at +4.5% exceeding the +4.1% projected passenger volume growth.