June US payrolls: Dead zone between Fed rate decisions

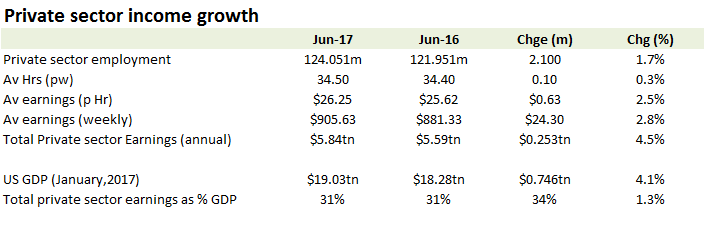

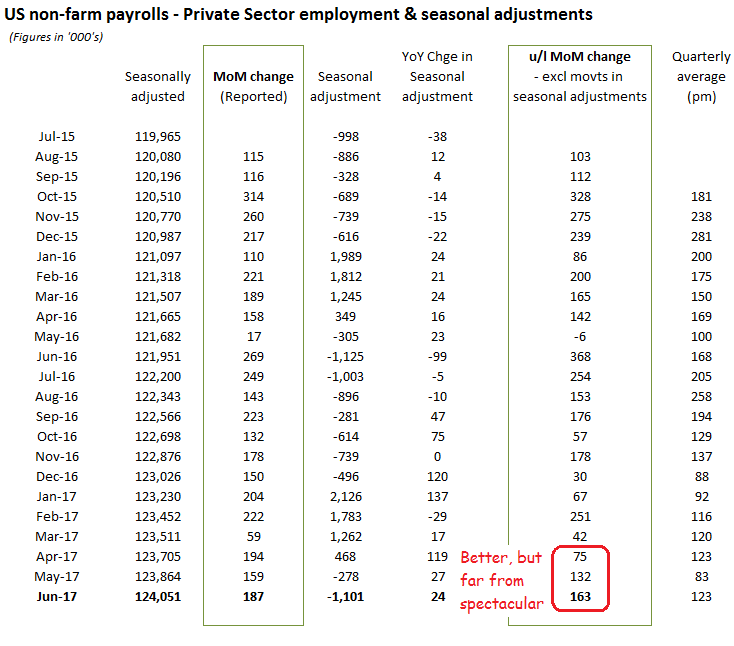

With the Fed having already edged up rates, June’s non-farm payrolls were going to have to be fairly spectacular to merit much attention as the ‘new’ Presidential grand tour moves to Europe and the G20. The reported MoM net job additions of +222k looked solid enough, although strip out government adds of +35k and Private sector net adds came in at +187k. Strip out another YoY increase in seasonal adjustments (of +24k) and the underlying private sector net job additions for June came in at +163k; better than May’s +132k, but with the trailing quarter still averaging only +123k per month. Annualised, that equates to private sector employment growth of +1.3%, which with average hourly wages rising by only +1.8% (annualised), again provides only limited camouflage to the current rate hardening currency war.

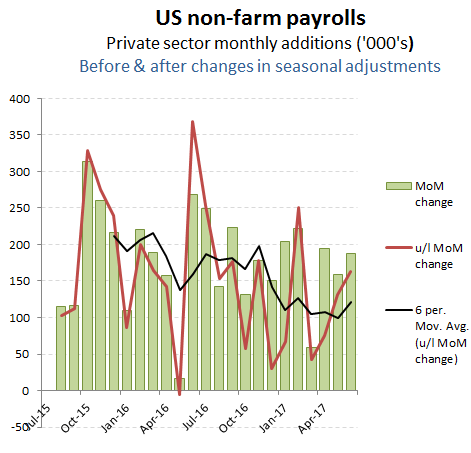

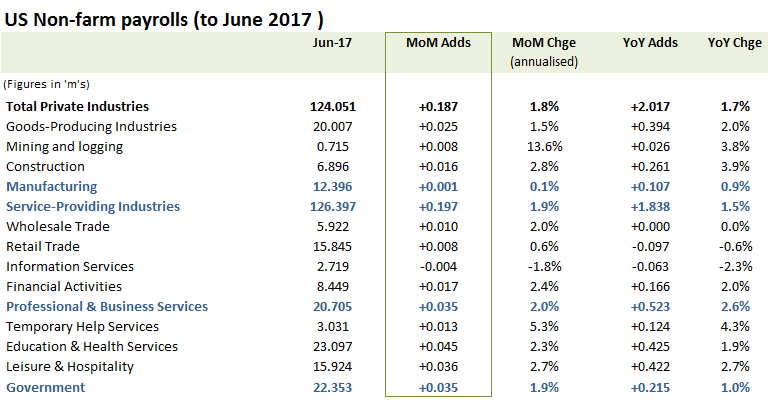

While presenting a major policy hurdle to ECB monetary stimulus for Europe, the strong US dollar/rate strategy is not great for US domestic manufacturing activity as can be seen in another sluggish monthly job additions (see below) from this sector. The rebound in fracking activity however continues to support ‘Mining & Logging’ categories while ‘Temporary Help’ and ‘Leisure & Hospitality’ segments are again leading the improvements.

Manufacturing stalls while growth centred on Temporary and Service jobs

Average hours worked edged ahead in June, which with the increase in hourly wages and employment suggest an annual increase in total private sector income growth of around +4.5%, a +20bps uplift from the annual rate posted for May, albeit effectively negated by the Fed’s intervening +25bps rate rise.